PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998723

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998723

Vapor Barriers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

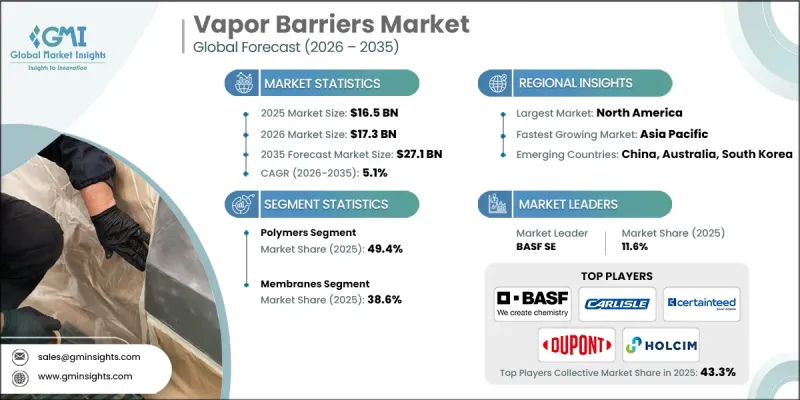

The Global Vapor Barriers Market was valued at USD 16.5 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 27.1 billion by 2035.

Growth in the vapor barriers market is driven by the increasing need for effective moisture management solutions in both residential and commercial construction. Builders and developers are increasingly prioritizing materials that help maintain indoor air quality, reduce energy consumption, and improve building durability. Vapor barriers play an important role in achieving these goals by preventing moisture infiltration that can compromise insulation performance and structural integrity. Rising awareness regarding sustainable construction methods is also contributing to the growing demand for advanced vapor barrier materials. The adoption of green building frameworks, including initiatives such as LEED certification standards, is encouraging the use of moisture-resistant and energy-efficient construction components. Technological progress within the industry is further supporting market development through the introduction of innovative material technologies designed to enhance performance and ease of installation. In addition, increasing construction activity in developing economies and the renovation of aging buildings to comply with modern energy efficiency standards are creating significant opportunities for market expansion. As sustainability awareness continues to grow and building regulations evolve, demand for environmentally responsible moisture control solutions is expected to remain strong across global construction markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.5 Billion |

| Forecast Value | $27.1 Billion |

| CAGR | 5.1% |

The polymer segment accounted for 49.4% share in 2025 and is anticipated to grow at a CAGR of 5.2% through 2035. Polymer-based materials maintain a leading position in the market due to their durability, cost efficiency, and effective moisture resistance. These materials provide strong flexibility and adaptability, allowing contractors to apply them across a wide range of construction environments. Their lightweight structure also simplifies installation processes while enabling manufacturers to produce vapor barrier solutions in multiple thicknesses that suit varying construction requirements. These advantages continue to support the widespread use of polymer-based vapor barrier materials in modern building projects.

The membrane segment held 38.6% share in 2025. Membrane-based vapor barriers are widely used because they provide highly effective waterproofing and moisture protection capabilities. Their structural properties allow them to perform reliably in both residential and industrial construction environments where moisture control is essential for maintaining building performance. In addition, the lightweight composition of membrane materials allows for faster and more efficient installation processes. As demand for energy-efficient construction solutions and environmentally responsible building practices continues to grow, membrane-based vapor barrier systems are increasingly aligned with the evolving needs of modern construction technologies.

North America Vapor Barriers Market will grow at a CAGR of 4.8% between 2026 and 2035. Demand across the region is rising as construction companies adopt advanced moisture protection systems that improve insulation performance and enhance building durability. Increasing interest in environmentally responsible construction methods and energy-efficient building designs continues to encourage the adoption of high-performance vapor barrier materials. Furthermore, updated building regulations and environmental standards are promoting the use of materials that support sustainable construction objectives, which is further contributing to market expansion across the region.

Key companies operating in the Global Vapor Barriers Market include DuPont, BASF SE, Carlisle Companies, Sika AG, Holcim, CertainTeed Corporation, Johns Manville, GAF Materials LLC, Soprema Group, Polyguard, Tremco, GCP Applied Technologies, VaproShield, and W.R. Meadows. Companies operating in the Global Vapor Barriers Market are focusing on multiple strategic initiatives to strengthen their market position and expand their global presence. Leading manufacturers are investing in research and development to introduce advanced materials that provide improved moisture resistance, durability, and energy efficiency. Many firms are also emphasizing environmentally sustainable product development by incorporating recyclable materials and low-emission manufacturing processes into their product portfolios. Strategic collaborations with construction companies and infrastructure developers are helping manufacturers integrate vapor barrier solutions into large-scale building projects. In addition, companies are expanding production capabilities and strengthening distribution networks to ensure a consistent supply across regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Installation

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing awareness of energy conservation and sustainable building

- 3.2.1.2 Government regulations on energy efficiency and moisture control in construction projects

- 3.2.1.3 Green building certifications (e.g., LEED) is encouraging the adoption of materials like vapor barriers to meet environmental standards

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Vapor barriers must be carefully selected for compatibility with various construction materials

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for sustainable and eco-friendly vapor barrier materials

- 3.2.3.2 Increasing construction activities in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material, 2022-2035 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Polymers

- 5.2.1 Polyethylene

- 5.2.2 Polypropylene

- 5.2.3 Polyvinyl chloride

- 5.2.4 Others

- 5.3 Glass

- 5.3.1 Fiberglass

- 5.3.2 Glass fiber reinforced materials

- 5.4 Metal

- 5.4.1 Aluminum foil

- 5.4.2 Metallized films

- 5.4.3 Steel & copper

- 5.5 Drywall

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Installation, 2022-2035 (USD Billion) ( Tons)

- 6.1 Key trends

- 6.2 Membranes

- 6.3 Coatings

- 6.4 Cementitious waterproofing

- 6.5 Stacking and filling

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Insulation

- 7.2.1 Cavity insulation

- 7.2.2 Continuous insulation

- 7.2.3 Spray foam insulation

- 7.2.4 Rigid board insulation

- 7.3 Waterproofing

- 7.4 Corrosion resistance

- 7.4.1 Metal structure protection

- 7.4.2 Concrete reinforcement protection

- 7.4.3 Industrial equipment protection

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Construction

- 8.2.1 Residential construction

- 8.2.2 Commercial construction

- 8.2.3 Industrial construction

- 8.3 Packaging

- 8.4 Automotive

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Carlisle Companies

- 10.3 CertainTeed Corporation

- 10.4 DuPont

- 10.5 GAF Materials LLC

- 10.6 GCP Applied Technologies

- 10.7 Holcim

- 10.8 Johns Manville

- 10.9 Polyguard

- 10.10 Sika AG

- 10.11 Soprema Group

- 10.12 Tremco

- 10.13 VaproShield

- 10.14 W.R. Meadows