PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998726

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998726

Automotive Piston Pin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

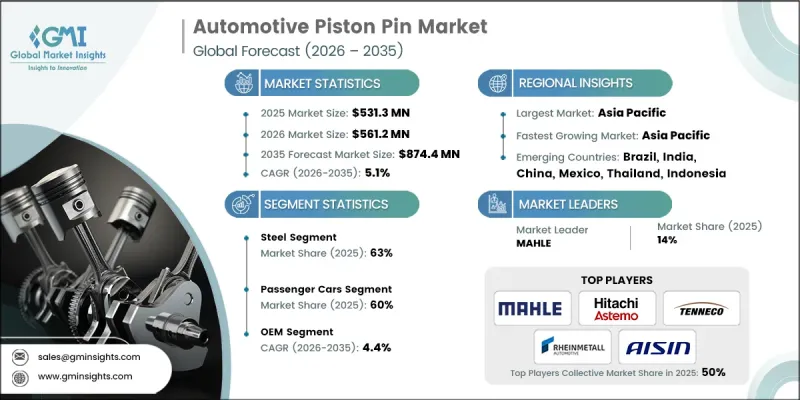

The Global Automotive Piston Pin Market was valued at USD 531.3 million in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 874.4 million by 2035.

Piston pins, also referred to as gudgeon pins, are critical engine components that link pistons to connecting rods, transferring combustion forces to the crankshaft. The market is increasingly driven by demand for higher engine durability, improved fuel efficiency, and enhanced performance in both passenger and commercial vehicles. Modern piston pin designs leverage high-performance alloy steels, diamond-like carbon (DLC) coatings, and precision machining to withstand high mechanical and thermal loads. Innovations in metallurgical processes, surface treatments, and lightweight design have transformed conventional solid pins into hollow, coated, and ultra-strong variants, reducing friction, boosting wear resistance, and supporting higher engine speeds. Rising global vehicle production, adoption of fuel-efficient engines, stringent emission standards, and growth in hybrid and turbocharged powertrains are major factors driving sustained market expansion. The commercial vehicle replacement segment also contributes to consistent demand for high-quality piston pins.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $531.3 Million |

| Forecast Value | $874.4 Million |

| CAGR | 5.1% |

The market comprises solid and hollow piston pins, coated variants, lightweight high-strength steel grades, and precision-finished pins supplied to OEMs and Tier 1 engine component manufacturers. Technological advances are shifting the market toward hollow and surface-treated designs, which minimize friction, extend engine life, and handle elevated combustion pressures. These innovations are especially relevant for downsized and turbocharged engines, where piston pins must sustain higher mechanical and thermal stresses.

The steel segment held a 63% share in 2025 and is expected to grow at a CAGR of 4.5% from 2026 to 2035. Steel retains market leadership due to its combination of strength, durability, cost efficiency, and established manufacturing processes. High-carbon steel alloys such as SAE 8620 and SAE 52100, after heat treatment, achieve tensile strengths exceeding 1,000 MPa and hardness levels of 58-62 HRC, ensuring reliability in internal combustion engines. Steel piston pins remain the preferred choice for commercial vehicles where durability and cost considerations outweigh weight reduction imperatives.

The passenger cars segment accounted for 60% share in 2025, growing at a CAGR of 4.2% through 2035. These vehicles include sedans, hatchbacks, SUVs, and crossovers under 6,000 pounds gross vehicle weight. Piston pins for passenger cars prioritize lightweight materials, friction reduction, and refinement rather than ultimate durability, reflecting typical service cycles of 150,000-200,000 miles. Aluminum alloys and advanced coatings, particularly DLC, are increasingly used, with DLC penetration exceeding 50% in premium segments, offering enhanced wear resistance and performance.

China Automotive Piston Pin Market accounted for USD 37.5 billion in 2025 and is forecasted to maintain a CAGR of 4.3% from 2026 to 2035. Its robust automotive manufacturing base, extensive supply chain control, and vertical integration of battery production and raw material sourcing reduce costs and reliance on international suppliers. Rising production of both passenger and commercial vehicles, combined with demand for high-performance internal combustion and hybrid powertrain components, fuels sustained growth in the region. China's commercial vehicle sector, particularly heavy-duty trucks supporting infrastructure development and freight logistics, ensures continuous demand for diesel engine components and piston pins. Regional manufacturers are also expanding into niche segments, increasing competition and innovation in the market.

Major players operating in the Global Automotive Piston Pin Market include Hitachi Astemo, Burgess-Norton, Kolbenschmidt Pistons, Aisin Seiki, Shriram Pistons & Rings, Art Metal, MAHLE, Elgin Industries, Bohai Piston, and Tenneco. Companies in the Global Automotive Piston Pin Market focus on strategies such as research and development of lightweight, hollow, and coated pins, integration of advanced alloy steels, and development of DLC and other surface treatments to enhance performance. Expanding production capacity and establishing localized manufacturing hubs in high-growth regions, particularly Asia-Pacific, helps reduce costs and improve supply chain reliability. Strategic collaborations with OEMs and Tier 1 engine manufacturers allow firms to integrate their components into new vehicle models early in the design process. Mergers, acquisitions, and partnerships also help companies expand technological capabilities and product portfolios, while aftermarket and replacement-focused strategies ensure recurring revenue streams. Additionally, marketing initiatives highlighting enhanced fuel efficiency, reduced wear, and engine longevity help strengthen brand recognition and market penetration.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Coating

- 2.2.4 Vehicle

- 2.2.5 Fuel

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing global automotive production and vehicle parc expansion

- 3.2.1.2 Increasing demand for fuel-efficient and lightweight engine components

- 3.2.1.3 Rising aftermarket demand driven by vehicle aging and maintenance cycles

- 3.2.1.4 Technological advancements in coating technologies (DLC, PVD)

- 3.2.1.5 Stringent emission regulations driving engine efficiency improvements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High raw material costs and price volatility of specialty alloys

- 3.2.2.2 Shift toward electric vehicles reducing ICE component demand

- 3.2.2.3 Complex manufacturing requirements and quality control challenges

- 3.2.2.4 Design constraints and pin distortion issues in high-performance applications

- 3.2.3 Market opportunities

- 3.2.3.1 Development of advanced composite and exotic alloy materials

- 3.2.3.2 Expansion in emerging markets with growing vehicle production

- 3.2.3.3 Increasing adoption of hybrid powertrains extending ICE component demand

- 3.2.3.4 Growing performance and racing segment requiring premium products

- 3.2.3.5 Digitalization and smart manufacturing reducing production costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- EPA GHG phase 3 & CAFE standards

- 3.4.1.2 Canada - Emissions-based regulatory framework

- 3.4.2 Europe

- 3.4.2.1 Germany- Euro 7 Emission Standards

- 3.4.2.2 UK- Post-brexit vehicle type approval

- 3.4.2.3 France- Decarbonization roadmap

- 3.4.2.4 Italy- Low-Emission zone compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China- China VI-b & Emerging China VII standards

- 3.4.3.2 India- BS-VI Stage II & bharat stage VII transition

- 3.4.3.3 Japan- Fuel efficiency standards (2030 Targets)

- 3.4.3.4 Australia- Fuel quality & ADR 79/05 standards

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM-194-SE-2021 & USMCA rules of origin

- 3.4.4.2 Argentina- Law 24.449 & environmental amendments

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Pricing analysis

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9.3 Total cost of ownership (TCO) analysis

- 3.10 Trade data analysis (Driven by Paid Database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Use cases & success stories

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Steel

- 5.3 Aluminum alloy

- 5.4 Titanium alloy

Chapter 6 Market Estimates & Forecast, By Coating, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Diamond-Like Carbon (DLC)

- 6.3 Physical Vapor Deposition (PVD)

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (MCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Gasoline engines

- 8.3 Diesel engines

- 8.4 Alternative fuel engines

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aisin Seiki

- 11.1.2 Art Metal

- 11.1.3 Burgess-Norton

- 11.1.4 Elgin Industries

- 11.1.5 Hitachi Astemo

- 11.1.6 MAHLE

- 11.1.7 Tenneco

- 11.2 Regional Players

- 11.2.1 Arias Pistons

- 11.2.2 Bohai Piston

- 11.2.3 Chuxiong Piston Pin

- 11.2.4 CP-Carrillo

- 11.2.5 JE Pistons

- 11.2.6 Kolbenschmidt Pistons (Comitans Capital)

- 11.2.7 Ming Shun Industrial

- 11.2.8 Ross Racing Pistons

- 11.2.9 Shriram Pistons & Rings

- 11.3 Emerging Players

- 11.3.1 Art-Serina Piston

- 11.3.2 Garima Global

- 11.3.3 Hai Yen Industrial

- 11.3.4 Power Industries