PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998727

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998727

Smart Pills Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

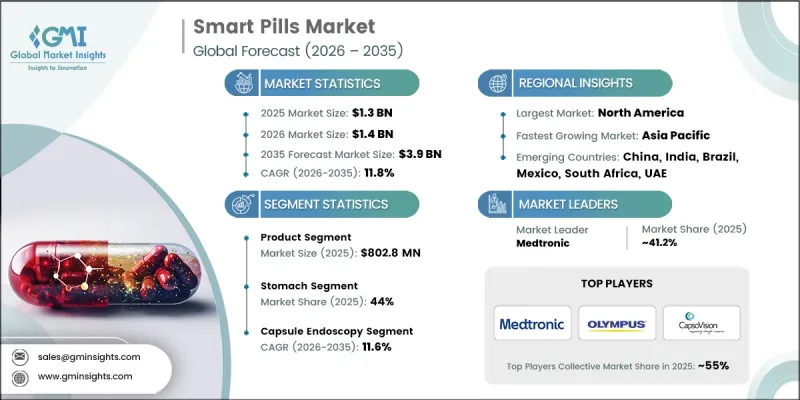

The Global Smart Pills Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 11.8% to reach USD 3.9 billion by 2035.

Growth in the smart pills market is driven by the increasing prevalence of gastrointestinal disorders and the growing demand for advanced diagnostic technologies that reduce the need for invasive procedures. Healthcare systems are increasingly adopting digital and sensor-based medical solutions that improve patient monitoring and diagnostic precision. Technological progress in data analytics, artificial intelligence, and digital health platforms has significantly enhanced the functionality of ingestible medical devices. Artificial intelligence plays an important role in processing large volumes of patient data, allowing healthcare professionals to identify health conditions more efficiently and implement accurate treatment strategies. At the same time, the integration of Internet of Things technologies is enabling remote monitoring capabilities, allowing physicians to observe patient health metrics without requiring frequent hospital visits. These innovations are improving clinical decision-making and enhancing the overall efficiency of diagnostic procedures. As digital healthcare technologies continue to evolve, smart pills are becoming an increasingly important tool for non-invasive diagnosis, patient monitoring, and disease management within modern healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $3.9 Billion |

| CAGR | 11.8% |

Smart pills are ingestible capsules that contain electronic or mechanical components designed to travel through the gastrointestinal tract for diagnostic, monitoring, or therapeutic purposes. Once swallowed, these capsules move naturally through the digestive system while collecting valuable physiological data. One of the major factors contributing to the adoption of this technology is the growing preference for minimally invasive medical procedures. Compared with traditional diagnostic techniques, smart pill technology offers improved patient comfort, lower risk of complications, and faster recovery. Continuous advancements in microelectronics, wireless connectivity, and sensor engineering have also strengthened the performance of these devices, enabling real-time physiological monitoring and expanding their potential clinical applications.

The product segment generated USD 802.8 million in 2025. Smart capsules are equipped with miniature sensors, microprocessors, and wireless communication technologies that transmit real time data related to gastrointestinal health, treatment adherence, and disease progression. These devices offer a convenient and non-invasive method for monitoring internal physiological conditions while also supporting precise drug delivery mechanisms. Their ease of use and advanced functionality have contributed to their increasing preference over conventional diagnostic approaches. In addition, the growing use of biocompatible materials and advanced patient monitoring technologies has further accelerated the adoption of smart capsules. Integration with wearable monitoring devices and digital health platforms is also expanding their role in modern healthcare.

The stomach segment accounted for 44% share in 2025. This segment holds a significant position due to the increasing application of smart pills in the monitoring and evaluation of stomach related conditions. Smart pill technologies designed for stomach assessment enable real time internal visualization and analysis of digestive health. These devices support accurate detection and monitoring of gastric disorders while minimizing patient discomfort compared with traditional diagnostic procedures. Growing demand for precise and early detection of stomach related diseases has further increased the adoption of this technology. In addition, improvements in sensor accuracy, imaging capabilities, and wireless communication systems have significantly enhanced the effectiveness of smart pill devices used for stomach diagnostics.

North America Smart Pills Market was valued at USD 503.5 million in 2025 and is expected to grow at a CAGR of 11.5% during 2026-2035. The region's strong growth is supported by its advanced healthcare infrastructure, widespread adoption of innovative medical technologies, and strong presence of digital healthcare solutions. Increasing prevalence of gastrointestinal conditions and chronic diseases continues to generate strong demand for advanced diagnostic and monitoring tools. In addition, the growing elderly population within the region is contributing to increased utilization of healthcare technologies that support early disease detection and continuous monitoring. The presence of established pharmaceutical and medical device manufacturers has also accelerated technological innovation within the industry. Continued investments in research, healthcare innovation programs, and supportive government initiatives further contribute to the steady expansion of the smart pills market across North America.

Major companies operating in the Global Smart Pills Market include Medtronic, Olympus Corporation, Otsuka Holdings, CapsoVision, ANX Robotica, Bodycap, Intromedic, Check-Cap, etectRx, and RF Co. Companies operating in the Smart Pills Market are implementing several strategic initiatives to strengthen their market presence and expand technological capabilities. Leading organizations are heavily investing in research and development to enhance sensor technologies, wireless communication systems, and data analytics platforms that improve the performance of ingestible medical devices. Many companies are also focusing on integrating artificial intelligence and connected health technologies to enable advanced diagnostic insights and remote patient monitoring. Strategic collaborations with healthcare providers, research institutions, and digital health companies are helping accelerate product development and clinical adoption. In addition, firms are expanding their global distribution networks and pursuing regulatory approvals in new markets to broaden their geographic reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.1.1 Business trends

- 2.1.2 Regional trends

- 2.1.3 Component trends

- 2.1.4 Target area trends

- 2.1.5 Application trends

- 2.1.6 End use trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of gastrointestinal disorders

- 3.2.1.2 Continuous improvements in smart pill technology

- 3.2.1.3 Growing demand for non-invasive diagnostic tools

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory requirements

- 3.2.2.2 High cost of devices

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with digital health ecosystems

- 3.2.3.2 Emerging market penetration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by primary research)

- 3.7 Investment and funding landscape

- 3.8 Impact of AI and generative AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Product

- 5.2.1 Capsule

- 5.2.2 Other products

- 5.3 Patient monitoring software

Chapter 6 Market Estimates and Forecast, By Target Area, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Stomach

- 6.3 Small intestine

- 6.4 Large intestine

- 6.5 Esophagus

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Capsule endoscopy

- 7.3 Targeted drug delivery

- 7.4 Vital sign monitoring

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ANX Robotica

- 10.2 Bodycap

- 10.3 CapsoVision

- 10.4 Check-Cap

- 10.5 etectRx

- 10.6 Intromedic

- 10.7 Medtronic

- 10.8 Otsuka Holdings

- 10.9 Olympus Corporation

- 10.10 RF Co.