PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998733

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998733

Compound Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

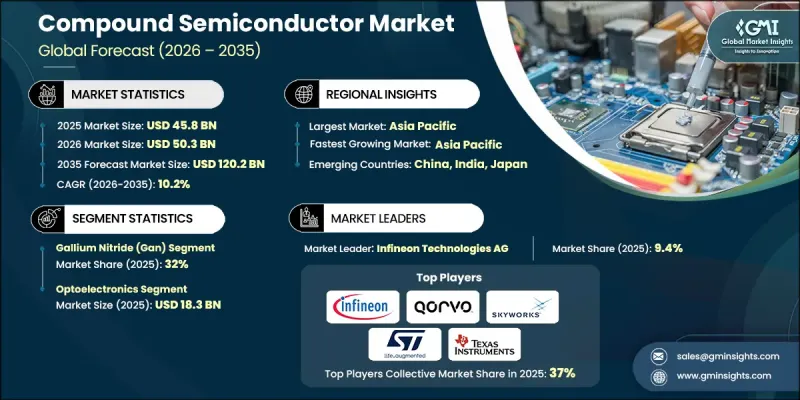

The Global Compound Semiconductor Market was valued at USD 45.8 billion in 2025 and is estimated to grow at a CAGR of 10.2% to reach USD 120.2 billion by 2035.

The market's expansion is driven by rising demand for electric vehicles, renewable energy systems, and energy-efficient high-performance components. The push for smaller, more compact electronic designs, rapid deployment of 5G networks, and the need for advanced radar systems are accelerating the adoption of compound semiconductors. In addition, the growing demand for photonics and optoelectronics products is supporting research and innovation across sectors. These materials provide superior performance in high-frequency and high-power applications, making them essential for modern infrastructure, telecommunications, automotive, and industrial energy solutions. The convergence of technological development, increased electrification, and network densification fuels continued investment and market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.8 Billion |

| Forecast Value | $120.2 Billion |

| CAGR | 10.2% |

The silicon carbide (SiC) segment is expected to grow at a CAGR of 11.1% during 2026-2035. SiC is favored for its exceptional power efficiency, thermal conductivity, and high-voltage performance, making it ideal for electric vehicles, renewable energy systems, and industrial power electronics. Its ability to operate under high temperatures and frequencies strengthens its role as a critical material in next-generation applications.

The power electronics segment is the fastest-growing application, growing at a CAGR of 12.6% from 2026 to 2035. This growth is driven by the rising need for energy-efficient power converters, inverters, and electric motor drives in electric vehicles, industrial systems, and renewable energy setups. GaN and SiC semiconductors provide high power density, superior thermal performance, and efficiency required for sustainable operation in these energy-sensitive sectors.

North America Compound Semiconductor Market held 22.1% share in 2025. The region is expanding rapidly due to strong demand from telecommunications, automotive, and renewable energy sectors. Investments in 5G infrastructure, electric vehicle adoption, and clean energy initiatives are fueling the need for high-performance semiconductors. Government programs supporting technology innovation, coupled with the presence of leading industry players, continue to drive market growth. The integration of these advanced materials across energy, mobility, and connectivity solutions positions North America as a major contributor to global compound semiconductor adoption.

Prominent players operating in the Global Compound Semiconductor Market include Wolfspeed, Inc., Infineon Technologies AG, Qorvo, Inc., Skyworks Solutions, Inc., STMicroelectronics N.V., Texas Instruments Incorporated, ams-OSRAM AG, MACOM Technology Solutions, Coherent Corp., Microchip Technology Inc., Renesas Electronics Corporation, Samsung Electronics Co., Ltd., Innoscience (Suzhou) Technology Holding Co., Ltd., Sumitomo Electric Industries, Navitas Semiconductor, Power Integrations, Inc., Nexperia B.V., and Freiberger Compound Materials GmbH. Key strategies adopted by companies in the Global Compound Semiconductor Market focus on strengthening their competitive positioning and global footprint. Firms are heavily investing in R&D to develop next-generation GaN and SiC solutions for high-efficiency power management and high-frequency applications. Strategic partnerships and collaborations with electric vehicle manufacturers, renewable energy companies, and telecom providers enable faster product adoption and tailored solutions. Companies are expanding regional manufacturing capabilities to reduce lead times, improve supply security, and meet growing global demand. They are also emphasizing sustainability by developing energy-efficient, low-loss semiconductor solutions. Targeted marketing, intellectual property protection, and advanced quality assurance protocols are employed to enhance brand reliability, establish long-term client relationships, and maintain a strong market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electric vehicles and renewable energy

- 3.2.1.2 Miniaturization and compact design requirements

- 3.2.1.3 Rapid development of 5G networks

- 3.2.1.4 Demand for high-efficiency radar solutions

- 3.2.1.5 Growing photonics and optoelectronics demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Material availability and supply chain risks

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in aerospace and defense

- 3.2.3.2 Surge in renewable energy systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Gallium nitride (GaN)

- 5.3 Gallium arsenide (GaAs)

- 5.4 Silicon carbide (SiC)

- 5.5 Indium phosphide (InP)

- 5.6 Silicon germanium (SiGe)

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Power electronics

- 6.2.1 Discrete devices

- 6.2.2 Power modules

- 6.2.3 Bare die

- 6.3 RF devices

- 6.3.1 Power amplifiers

- 6.3.2 Discrete transistors

- 6.3.3 Integrated RF components

- 6.3.4 RF integrated circuits

- 6.4 Optoelectronics

- 6.4.1 LEDs

- 6.4.2 Laser diodes

- 6.4.3 Photodetectors

- 6.4.4 Others

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Telecommunications

- 7.3 Automotive

- 7.4 Aerospace & defense

- 7.5 Industrial & power supply

- 7.6 Consumer electronics

- 7.7 Renewable energy

- 7.8 Data centers & computing

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Infineon Technologies AG

- 9.1.2 Qorvo, Inc.

- 9.1.3 Skyworks Solutions, Inc.

- 9.1.4 STMicroelectronics N.V.

- 9.1.5 Texas Instruments Incorporated

- 9.1.6 Wolfspeed, Inc.

- 9.1.7 ams-OSRAM AG

- 9.1.8 MACOM Technology Solutions

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Navitas Semiconductor

- 9.2.1.2 Power Integrations, Inc.

- 9.2.1.3 Microchip Technology Inc.

- 9.2.2 Europe

- 9.2.2.1 Renesas Electronics Corporation

- 9.2.2.2 Freiberger Compound Materials GmbH

- 9.2.2.3 Nexperia B.V.

- 9.2.3 Asia Pacific

- 9.2.3.1 AXT, Inc.

- 9.2.3.2 Samsung Electronics Co., Ltd.

- 9.2.3.3 Innoscience (Suzhou) Technology Holding Co., Ltd.

- 9.2.3.4 Sumitomo Electric Industries

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Coherent Corp.