PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998738

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998738

Electric Commercial Vehicle Traction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

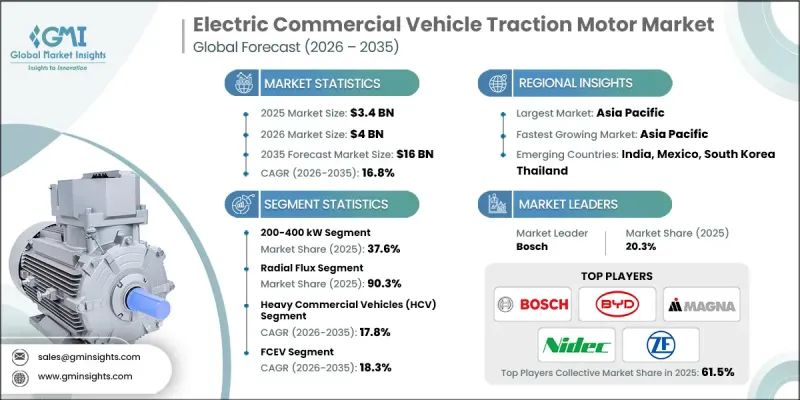

The Global Electric Commercial Vehicle Traction Motor Market was valued at USD 3.4 billion in 2025 and is estimated to grow at a CAGR of 16.8% to reach USD 16 billion by 2035.

Traction motors play a crucial role in electric commercial vehicles by converting electrical energy into mechanical power that drives trucks, vans, buses, and other heavy-duty vehicles. As electrification spreads across commercial transportation fleets, these motors are becoming one of the most important components enabling efficient vehicle performance. Businesses operating commercial vehicles are increasingly recognizing the economic advantages associated with electric propulsion systems. Electric traction motors offer improved energy efficiency and lower operational costs compared with conventional powertrain technologies. In addition, electric vehicles typically require less maintenance because they contain fewer moving components, which reduces repair expenses and vehicle downtime. These cost savings make electric commercial vehicles an attractive solution for fleet operators seeking long-term operational efficiency. As global transportation systems continue transitioning toward low-emission mobility, the demand for advanced traction motor technologies is expected to rise significantly, supporting sustained growth in the global electric commercial vehicle traction motor market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.4 Billion |

| Forecast Value | $16 Billion |

| CAGR | 16.8% |

Government initiatives and regulatory frameworks designed to reduce transportation emissions are further accelerating the adoption of electric commercial vehicles and their associated components. Authorities in many regions are implementing stricter environmental standards while introducing incentives such as tax benefits and financial subsidies to encourage businesses to transition toward electric fleets. These policy measures are creating a favorable environment for manufacturers developing high-performance traction motors. At the same time, technological innovation is improving motor efficiency, durability, and thermal performance. Modern motor designs are increasingly optimized to deliver higher power output while consuming less electrical energy. Continuous improvements in motor architecture and advanced materials are enabling vehicles to achieve greater operational range, faster acceleration, and improved reliability.

The 200-400 kW power segment held a 37.6% share, generating USD 1.3 billion in 2025. Traction motors within this power range are commonly used in medium-duty and heavy-duty electric trucks and buses that require strong propulsion capabilities to transport substantial loads across extended distances. These motors deliver sufficient power to support demanding commercial applications while maintaining efficiency and durability. Although motors in this category typically involve higher production costs than lower-power alternatives, they incorporate advanced engineering designed to handle intensive operational conditions. As commercial transportation fleets increasingly adopt electric powertrains to meet regulatory and environmental objectives, the demand for high-capacity traction motors capable of supporting large vehicles is expected to grow steadily across global markets.

The radial flux motor segment held 90.3% share and is projected to reach USD 14.2 billion by 2035. Radial flux motors have been widely utilized in electric vehicle traction systems for many years due to their proven reliability and consistent operational performance. Their relatively simple design structure makes them easier to manufacture at scale, which helps maintain cost efficiency while ensuring strong mechanical durability. These motors are particularly suitable for commercial vehicles that must transport heavy loads over long distances while maintaining stable performance levels. Fleet operators and manufacturers value radial flux motors for their ability to deliver high torque and power output while maintaining efficient energy consumption. As commercial electric vehicle production expands globally, radial flux motor technology is expected to remain a preferred solution for many heavy-duty vehicle applications.

United States Electric Commercial Vehicle Traction Motor Market generated USD 395.4 million in 2025 and is expected to grow at a CAGR of 15.6% between 2026 and 2035. Government policies aimed at reducing transportation emissions and supporting electric mobility are playing a major role in accelerating market growth across the country. Regulatory frameworks across various states are influencing vehicle manufacturing standards and encouraging the adoption of cleaner transportation technologies. These policies are creating opportunities for companies to produce traction motors specifically designed for electric commercial vehicles. As environmental regulations continue to tighten and electrification becomes a strategic priority for the transportation sector, the United States is expected to remain a key market supporting innovation and investment in electric commercial vehicle traction motor technologies.

Major companies operating in the Global Electric Commercial Vehicle Traction Motor Market include ABB, Allison, BorgWarner, BYD, Dana, Magna, Nidec, Robert Bosch, Valeo, and ZF Friedrichshafen. Companies participating in the Global Electric Commercial Vehicle Traction Motor Market are implementing several strategies to strengthen their competitive positioning and expand their global presence. Manufacturers are investing heavily in research and development to improve motor efficiency, thermal management, and power density in order to meet the performance requirements of next-generation electric commercial vehicles. Many firms are also forming strategic partnerships with vehicle manufacturers to integrate traction motor systems into new electric truck and bus platforms. Expansion of manufacturing facilities and supply chain capabilities is another key focus area as companies aim to support growing demand for electrified transportation solutions. Additionally, businesses are developing modular motor architectures and advanced control technologies to improve product versatility, reduce production costs, and enhance long-term reliability for commercial fleet applications.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Motor

- 2.2.3 Power Output

- 2.2.4 Motor Design

- 2.2.5 Axle Architecture

- 2.2.6 Transmission

- 2.2.7 Vehicle

- 2.2.8 Powertrain

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission regulations & zero-emission mandates

- 3.2.1.2 Total cost of ownership (TCO) advantages over ICE vehicles

- 3.2.1.3 Government incentives & subsidies for electric commercial fleets

- 3.2.1.4 Rapid urbanization & last-mile delivery demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from hydrogen fuel cell powertrains in long-haul segments

- 3.2.2.2 Motor overheating & durability in extreme operating conditions

- 3.2.3 Market opportunities

- 3.2.3.1 Fleet electrification by logistics & e-commerce companies

- 3.2.3.2 Government investments in public transit electrification

- 3.2.3.3 Expansion of battery swapping & ultra-fast charging networks

- 3.2.3.4 Technological breakthroughs in motor efficiency & power density

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 Transportation Canada (TC)

- 3.4.2 Europe

- 3.4.2.1 European Commission (EC)

- 3.4.2.2 European Union Regulation (EU) No 168/2013

- 3.4.2.3 International Organization for Standardization (ISO)

- 3.4.3 Asia Pacific

- 3.4.3.1 China National Standardization Administration (SAC)

- 3.4.3.2 Japan Automobile Standards Internationalization Center (JASIC)

- 3.4.4 Latin America

- 3.4.4.1 Instituto Nacional de Metrologia (INMETRO)

- 3.4.4.2 Mexico's Secretaria de Comunicaciones y Transportes (SCT)

- 3.4.5 Middle East & Africa

- 3.4.5.1 South African Bureau of Standards (SABS)

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.1 North America

- 3.5 Investment & Funding Analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Permanent Magnet Synchronous Motors (PMSM)

- 3.8.1.2 Induction Motors (Asynchronous Motors)

- 3.8.1.3 Switched Reluctance Motors (SRM)

- 3.8.2 Emerging technologies

- 3.8.2.1 Solid-State Motors

- 3.8.2.2 High-Temperature Superconducting Motors (HTS)

- 3.8.1 Current technologies

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Trade data analysis (Driven by Paid Database)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Capacity & production landscape (driven by primary research)

- 3.12.1 Installed capacity by region & key producer

- 3.12.2 Capacity utilization rates & expansion pipelines

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Battery technology and its interplay with traction motors

- 3.14.1 Battery chemistry evolution & motor compatibility

- 3.14.2 Voltage architecture trends (400V vs 800V systems)

- 3.14.3 Battery-motor thermal management integration

- 3.14.4 State of charge (SOC) impact on motor performance

- 3.15 Lifecycle and sustainability of traction motors

- 3.15.1 Rare earth material dependency & supply chain risks

- 3.15.2 Circular economy approaches & remanufacturing

- 3.15.3 End-of-life recycling & material recovery

- 3.15.4 Carbon footprint analysis

- 3.16 Case studies

- 3.17 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Motor, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Permanent Magnet Synchronous Motor (PMSM)

- 5.3 Switched Reluctance Motor (SRM)

- 5.4 AC Induction Motor

- 5.5 DC Traction Motor

- 5.6 Electrically Excited Synchronous Motor

Chapter 6 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Less than 100 kW

- 6.3 100-200 kW

- 6.4 200-400 kW

- 6.5 Above 400 kW

Chapter 7 Market Estimates & Forecast, By Motor Design, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Radial Flux

- 7.3 Axial Flux

Chapter 8 Market Estimates & Forecast, By Axle Architecture, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Integrated Axle

- 8.3 Central Drive Unit

Chapter 9 Market Estimates & Forecast, By Transmission, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 Single-Speed Drive

- 9.3 Multi-Speed Drive

Chapter 10 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 Light commercial vehicles (LCV)

- 10.3 Medium commercial vehicles (MCV)

- 10.4 Heavy commercial vehicles (HCV)

Chapter 11 Market Estimates & Forecast, By Powertrain, 2022 - 2035 ($Mn, Thousand Units)

- 11.1 Key trends

- 11.2 BEV

- 11.3 PHEV

- 11.4 FCEV

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Belgium

- 12.3.7 Sweden

- 12.3.8 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Chile

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 BYD

- 13.1.2 ZF Friedrichshafen

- 13.1.3 Dana

- 13.1.4 Robert Bosch

- 13.1.5 Magna

- 13.1.6 Allison

- 13.1.7 ABB

- 13.1.8 BorgWarner

- 13.1.9 Valeo

- 13.1.10 Nidec

- 13.2 Regional players

- 13.2.1 TECO Electric & Machinery

- 13.2.2 Brogen

- 13.2.3 Broad-Ocean Motor

- 13.2.4 WEG

- 13.2.5 American Axle & Manufacturing

- 13.2.6 Mahle

- 13.3 Emerging players

- 13.3.1 Equipmake

- 13.3.2 YASA

- 13.3.3 Saietta

- 13.3.4 Protean Electric