PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998743

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998743

Aircraft Transparencies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

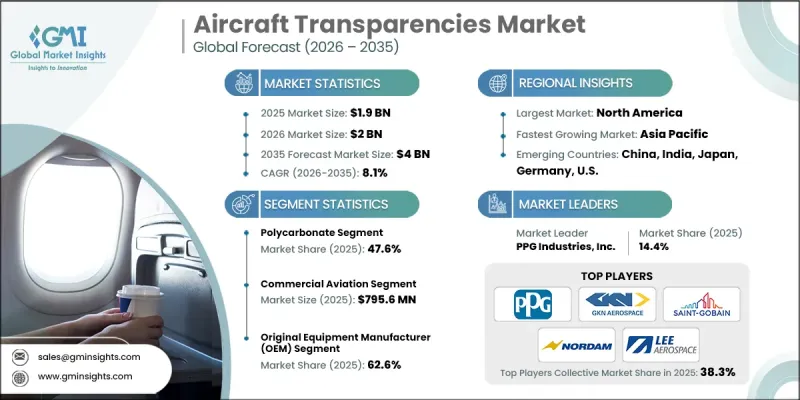

The Global Aircraft Transparencies Market was valued at USD 1.9 billion in 2025 and is estimated to grow at a CAGR of 8.1% to reach USD 4 billion by 2035.

The expansion of the market is driven by rising commercial aircraft production rates, increasing aftermarket replacement cycles, military aircraft modernization, and the adoption of advanced materials such as polycarbonate and acrylic laminates. Airlines are fulfilling delivery backlogs, prompting OEMs to ramp up production, while defense programs worldwide are upgrading aircraft capabilities. Electrically dimmable cabin windows are gaining traction in next-generation commercial aircraft, improving passenger experience and reducing reliance on mechanical shades. Technological innovations, combined with growing demand for lightweight, durable, and thermally efficient glazing, are propelling the market forward. Increasing focus on safety, FAA and EASA certification compliance, and MRO service requirements further support long-term growth in both commercial and military aviation segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.9 Billion |

| Forecast Value | $4 Billion |

| CAGR | 8.1% |

The polycarbonate segment held a 47.6% share in 2025, attributed to its superior impact resistance, lightweight structure, and compatibility with heating and anti-icing systems. Polycarbonate materials meet regulatory safety, optical, and thermal performance standards, making them ideal for cockpit windshields, cabin windows, and side panels. Their durability reduces replacement frequency for OEMs and MRO providers, ensuring widespread adoption across commercial, business, and military aircraft.

The commercial aviation segment reached USD 795.6 million in 2025, driven by fleet expansion, high delivery rates, and stringent cockpit and cabin glazing regulations. Rising production and replacement cycles of aircraft fleets further enhance demand.

North America Aircraft Transparencies Market held 38.5% share in 2025, fueled by a robust aerospace manufacturing base, extensive commercial aircraft production, and growing defense programs. Strong OEM presence, a mature MRO ecosystem, and high adoption of advanced polycarbonate, acrylic, and smart glazing technologies underpin regional growth through 2035.

Prominent players operating in the Global Aircraft Transparencies Market include Aeropair Ltd., Aviationglass & Technology B.V., Control Logistics Inc., GKN Aerospace, Lee Aerospace, Llamas Plastics Inc., Lockheed Martin, LP Aero Plastics Inc., Mecaplex Ltd., Perkins Aircraft Windows, PPG Industries, Inc., Saint-Gobain, Spartech, Tech-Tool Plastics, Inc., and The Nordam Group LLC. Key strategies adopted by companies to strengthen their market presence include investing in R&D for advanced materials and smart glazing solutions, forming strategic partnerships with aircraft OEMs and MRO providers, expanding production capacities to meet growing demand, offering custom-engineered solutions for commercial and military applications, and maintaining regulatory compliance across global markets. Firms also focus on aftersales support, lifecycle services, and retrofitting programs to enhance customer loyalty while optimizing supply chains for cost efficiency and faster delivery.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Aircraft type trends

- 2.2.3 Application trends

- 2.2.4 Point of sales trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising commercial aircraft deliveries backlog fulfillment

- 3.2.1.2 Increasing cockpit window replacement cycles

- 3.2.1.3 Growth in military aircraft modernization programs

- 3.2.1.4 Demand for lightweight polycarbonate laminates

- 3.2.1.5 Stringent bird-strike impact resistance requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High certification costs (FAA/EASA compliance)

- 3.2.2.2 Complex multi-layer lamination manufacturing process

- 3.2.3 Market opportunities

- 3.2.3.1 Electrically dimmable smart cabin windows

- 3.2.3.2 Lightweight composite frame-integrated transparencies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Glass

- 5.3 Acrylic

- 5.4 Polycarbonate

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Commercial aviation

- 6.2.1 Narrow-body

- 6.2.2 Wide-body

- 6.2.3 Regional transport

- 6.2.4 Commercial helicopter

- 6.3 Business & general aviation

- 6.3.1 Business jets

- 6.3.2 General aviation aircraft

- 6.4 Military aviation

- 6.4.1 Fighter aircraft

- 6.4.2 Transport & special mission aircraft

- 6.4.3 Military helicopter

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Windshields

- 7.3 Windows

- 7.4 Canopies

- 7.5 Chin bubbles

- 7.6 Landing lights & wingtip lenses

- 7.7 Cabin interiors

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Point of Sales, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Original equipment manufacturer (OEM)

- 8.3 Aftermarket

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 PPG Industries, Inc.

- 10.1.2 GKN Aerospace

- 10.1.3 Saint-Gobain

- 10.1.4 Lee Aerospace

- 10.1.5 Lockheed Martin

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 LP Aero Plastics Inc.

- 10.2.1.2 Mecaplex Ltd.

- 10.2.1.3 Tech-Tool Plastics, Inc.

- 10.2.1.4 Perkins Aircraft Windows

- 10.2.1.5 Spartech

- 10.2.2 Asia Pacific

- 10.2.2.1 Aeropair Ltd.

- 10.2.3 Europe

- 10.2.3.1 Aviationglass & Technology B.V.

- 10.2.3.2 The Nordam Group LLC

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Llamas Plastics Inc.

- 10.3.2 Control Logistics Inc.