PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998748

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998748

Automotive Sunroof Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

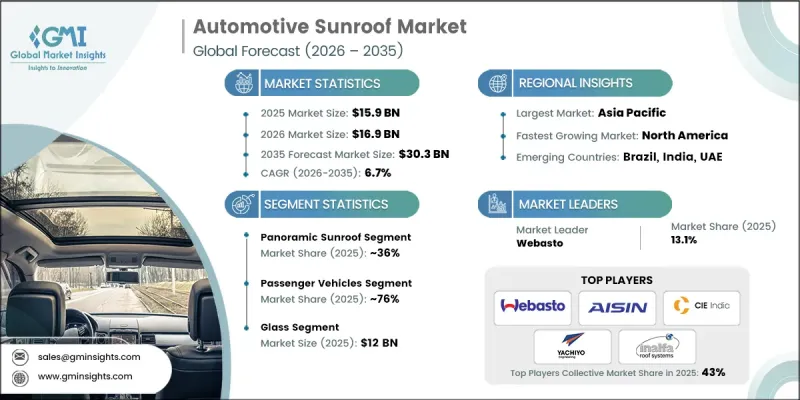

The Global Automotive Sunroof Market was valued at USD 15.9 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 30.3 billion by 2035.

The market is witnessing robust growth, fueled by rising vehicle premiumization, increasing consumer focus on interior aesthetics, and the rapid expansion of SUVs, crossovers, and electric vehicles worldwide. Automakers, Tier-1 suppliers, and fleet operators are under pressure to differentiate vehicles, enhance passenger comfort, and meet stringent safety and regulatory standards, driving the adoption of advanced sunroof technologies. Innovations in electrically operated tilt & slide mechanisms, panoramic multi-panel roofs, solar-integrated panels, smart electrochromic glazing, and connected roof systems are transforming conventional sunroof design. OEMs are increasingly investing in modular roof platforms, high-performance glazing, and cost-efficient electric actuation systems, enabling adoption across economy, mid-range, and premium vehicles. The evolving ecosystem emphasizes passenger comfort, energy efficiency, aesthetics, and overall value creation in passenger cars, SUVs, and EVs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.9 Billion |

| Forecast Value | $30.3 Billion |

| CAGR | 6.7% |

The panoramic sunroof segment held 36% share in 2025 and is expected to grow at a CAGR of 5.4% through 2035. Its premium appeal, ability to create a sense of spaciousness, and compatibility with SUVs, crossovers, and electric vehicles make it highly favored by manufacturers. Panoramic roofs enhance cabin comfort, visual appeal, and perceived value, driving adoption across mid-range and luxury vehicle segments, including passenger cars and light commercial vehicles.

The passenger vehicles segment held 76% share in 2025 and is expected to grow at a CAGR of 6.2% from 2026 to 2035. Widespread adoption of sedans, SUVs, and electric passenger cars, along with growing consumer preference for premium interiors, supports this segment. OEMs are standardizing sunroof integration to ensure high-quality assembly, reliable operation, and compliance with safety and UV-protection regulations. Extensive deployment across Europe, North America, and Asia-Pacific reinforces this segment's market leadership.

China Automotive Sunroof Market held 51% share, generating USD 2.5 billion in 2025. Rapid EV adoption, expanding SUV and passenger car production, and a strong presence of OEMs and specialized sunroof manufacturers support this growth. Advanced manufacturing capabilities, large-scale assembly, and established service networks drive high demand for panoramic, tilt & slide, and multi-panel systems across passenger and light commercial vehicles.

Key players in the Global Automotive Sunroof Market include Inalfa Roof Systems, Aisin Seiki, Magna International, CIE Automotive, Inteva Products, Robert Bosch, Webasto, Hyundai Motor, Tesla, and Yachiyo Industry. Companies in the Automotive Sunroof Market are employing several strategies to strengthen their market position. They are investing in R&D to develop advanced roof technologies such as panoramic, electrochromic, and solar-integrated systems. Collaborations with OEMs and Tier-1 suppliers ensure seamless integration of innovative sunroof features across multiple vehicle platforms. Strategic geographic expansion and partnerships in emerging markets help capture growing SUV and EV demand. Firms are optimizing production processes for cost efficiency, modularity, and scalability, enabling broader adoption across economy, mid-range, and premium vehicles. Emphasis on quality, compliance with safety regulations, and energy-efficient designs enhances brand credibility, boosts customer trust, and reinforces long-term competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Material

- 2.2.5 Operation mechanism

- 2.2.6 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising SUV and EV Sales

- 3.2.1.2 Premiumization & passenger experience

- 3.2.1.3 Technological advancements

- 3.2.1.4 Regulatory & safety compliance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production & maintenance costs

- 3.2.2.2 Limited aftermarket adoption

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with EV & Connected Vehicles

- 3.2.3.2 Emerging markets growth

- 3.2.3.3 Multi-OEM and modular platforms

- 3.2.3.4 Integration with smart and sustainable features

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, CARB, NHTSA Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS 305

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, Euro 6/7 Regulations

- 3.4.2.2 France: Ministry of Transport, Euro 6/7

- 3.4.2.3 UK: Department for Transport, Euro 6/7

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, Emission Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Regulations

- 3.4.3.3 South Korea: MOLIT, KS Emission Standards

- 3.4.3.4 India: MoRTH, BS6 Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO Emission Standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus)

- 3.8.3 OEM vs Aftermarket Price Differentiation

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent landscape (Driven by Primary Research)

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Sustainability and Environmental Aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Capacity & production landscape (Driven by Primary Research)

- 3.14.1 Installed capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipelines

- 3.15 Use case scenarios

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Panoramic Sunroof

- 5.3 Built-in/Inbuilt Sunroof

- 5.4 Tilt & Slide Sunroof

- 5.5 Spoiler/Top-mounted Sunroof

- 5.6 Pop-up Sunroof

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Glass

- 7.3 Fabric

Chapter 8 Market Estimates & Forecast, By Operation Mechanism, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Automatic/Electric

- 8.3 Manual

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 Aisin Seiki

- 11.1.2 CIE Automotive

- 11.1.3 Hyundai Motor

- 11.1.4 Inalfa Roof Systems

- 11.1.5 Inteva Products

- 11.1.6 Magna International

- 11.1.7 Robert Bosch

- 11.1.8 Tesla

- 11.1.9 Webasto

- 11.1.10 Yachiyo Industry

- 11.2 Regional Player

- 11.2.1 Edscha

- 11.2.2 Faurecia

- 11.2.3 Ficosa International

- 11.2.4 Furukawa Electric

- 11.2.5 Johnson Controls Interiors

- 11.2.6 Magneti Marelli

- 11.2.7 Samvardhana Motherson

- 11.2.8 Suntech Sunroof Systems

- 11.2.9 Tokai Rika

- 11.2.10 Valeo