PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998751

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998751

Middle East District Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

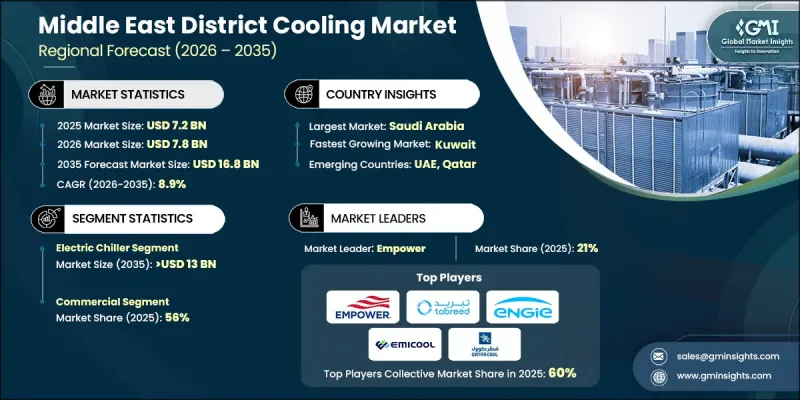

Middle East District Cooling Market was valued at USD 7.2 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 16.8 billion by 2035.

Market growth is driven by extreme climatic conditions, rapid urbanization, and strong government mandates for energy efficiency and sustainability across GCC countries. District cooling systems are increasingly preferred over conventional air-conditioning solutions due to their ability to reduce electricity consumption by 20-35%, lower carbon emissions, and provide reliable cooling for large-scale developments. Rising investments in mega infrastructure projects, smart cities, and mixed-use developments, particularly under Saudi Vision 2030 and UAE clean energy strategies, are significantly accelerating market adoption. Additionally, advancements in thermal energy storage, digital monitoring, and integration with renewable energy sources are further enhancing system efficiency and long-term cost benefits for end users.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.2 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 8.9% |

By production technique, the electric chiller segment is expected to reach USD 13 billion by 2035. Electric chillers dominate due to their scalability, high efficiency, and suitability for large commercial and urban developments with high cooling demand. Continuous upgrades such as variable speed drives, magnetic bearing compressors, and hybrid configurations with thermal energy storage are improving performance while reducing operational costs. These systems are widely deployed across dense urban centers such as Dubai, Abu Dhabi, and Riyadh, where consistent and high-capacity cooling is critical.

In terms of application, the commercial segment accounted for 56% share in 2025. Strong demand from offices, government buildings, healthcare facilities, hospitality, and large mixed-use developments continues to fuel growth. Commercial developers increasingly favor district cooling to meet green building standards such as LEED and Estidama, reduce lifecycle energy costs, and ensure compliance with regional sustainability regulations. Long-term service contracts and centralized cooling infrastructure also provide predictable operating expenses, making district cooling an attractive solution for large commercial assets.

Saudi Arabia District Cooling Market generated USD 2.5 billion in 2025 and continues to gain momentum as the country increases investments in modern cooling infrastructure across urban developments. Significant capital is being directed toward the refurbishment and modernization of commercial buildings, corporate offices, hospitality facilities, and educational institutions, which is creating strong demand for centralized and energy-efficient cooling systems. As these facilities upgrade their infrastructure to meet modern operational standards, district cooling solutions are increasingly being adopted to deliver reliable temperature control while improving overall energy efficiency.

Key players operating in the Middle East District Cooling Market include Tabreed, Emirates Central Cooling Systems Corporation (Empower), Emicool, Qatar Cool, ENGIE, ADC Energy Systems, Ramboll Group, Arabian Cooling, City Cool, Marubeni Corporation, TAKEEF, and Saudi Tabreed, among others. Companies in the Middle East district cooling market are strengthening their market position through a combination of capacity expansion, strategic partnerships, and technology integration. Leading players are forming long-term agreements with master developers and government entities to secure stable revenue streams from large-scale urban and mixed-use projects. Investments in advanced electric chillers, thermal energy storage, and AI-driven digital monitoring platforms are helping operators improve efficiency and reduce operational costs. Firms are also leveraging green financing and sustainability-linked loans to support expansion while meeting ESG targets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates and forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Production technique trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/RT)

- 3.5.1 By production technique

- 3.5.2 By application

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of district cooling

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.10 Impact of AI & Generative AI on the industry (Core Solution)

- 3.10.1 AI-Driven production optimization

- 3.10.2 Predictive maintenance & fault detection

- 3.11 Emerging opportunities & trends

- 3.11.1 Digitalization & IoT integration

- 3.11.2 Growth in untapped markets & applications

- 3.12 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 Saudi Arabia

- 4.2.2 UAE

- 4.2.3 Oman

- 4.2.4 Qatar

- 4.2.5 Kuwait

- 4.2.6 Bahrain

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Production Technique, 2022 - 2035 (USD Million & '000 RT)

- 5.1 Key trends

- 5.2 Free cooling

- 5.3 Electric chiller

- 5.4 Absorption cooling

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & '000 RT)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.3.1 Education

- 6.3.2 Office

- 6.3.3 Government

- 6.3.4 Healthcare

- 6.3.5 Others

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Country, 2022 - 2035 (USD Million & '000 RT)

- 7.1 Key trends

- 7.2 Saudi Arabia

- 7.3 UAE

- 7.4 Oman

- 7.5 Qatar

- 7.6 Kuwait

- 7.7 Bahrain

Chapter 8 Company Profiles

- 8.1 ADC Energy Systems

- 8.2 ALFA LAVAL

- 8.3 Araner

- 8.4 Dalkia Middle East

- 8.5 Danfoss

- 8.6 DC Pro Engineering

- 8.7 DISTRICT COOLING INTERNATIONAL LLC

- 8.8 Emicool

- 8.9 Emirates Central Cooling Systems Corporation PJSC

- 8.10 ENGIE

- 8.11 Johnson Controls

- 8.12 Marafeq Qatar

- 8.13 Pal Cooling Holding

- 8.14 Qatar District Cooling Company

- 8.15 Ramboll Group AS

- 8.16 Shinryo Corporation

- 8.17 Siemens

- 8.18 Stellar Energy

- 8.19 Tabreed

- 8.20 Veolia