PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998761

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998761

Incretin-based Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

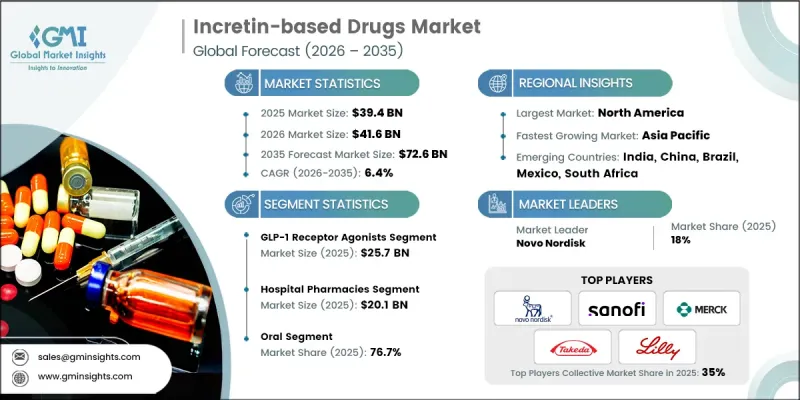

The Global Incretin-based Drugs Market was valued at USD 39.4 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 72.6 billion by 2035.

Growth in the incretin-based drugs industry is closely associated with the accelerating incidence of type 2 diabetes mellitus worldwide, which continues to increase demand for effective long-term treatment options. Medical professionals are progressively shifting toward non-insulin therapeutic approaches that offer improved glycemic control while supporting broader cardiometabolic health. Therapies in this category, including GLP-1 receptor agonists and DPP-4 inhibitors, help regulate blood glucose by stimulating insulin secretion and suppressing glucagon production. In addition, these treatments contribute to weight management and improved cardiovascular health, which has strengthened their clinical acceptance. Continuous improvements in drug delivery technologies, combined with rising awareness about advanced diabetes care, are further encouraging adoption across developed and emerging healthcare systems. As healthcare providers focus on improving treatment outcomes and long-term disease management, incretin-based therapies are increasingly being incorporated into diabetes treatment protocols. This evolving therapeutic landscape is expected to sustain strong demand for incretin-based medications over the coming decade.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.4 Billion |

| Forecast Value | $72.6 Billion |

| CAGR | 6.4% |

The incretin-based drugs market is also benefiting from growing clinical recognition of the cardiometabolic advantages associated with these therapies, particularly within the GLP-1 receptor agonists category. Beyond glucose regulation, these treatments are increasingly valued for their ability to support broader cardiovascular health in individuals living with type 2 diabetes. Medical studies have shown that therapies in this class can help lower the risk of major cardiovascular complications among high-risk patients, which has elevated their position in diabetes care strategies. Additional benefits such as reductions in blood pressure, improvements in lipid metabolism, and anti-inflammatory effects have further strengthened their role in comprehensive cardiometabolic management. Weight management has also become a significant factor influencing treatment decisions, as excess body weight remains a common concern among individuals with diabetes.

The GLP-1 receptor agonists segment generated USD 25.7 billion in 2025. This segment continues to experience strong adoption due to its consistent clinical performance and expanding relevance in metabolic disease management. Treatments within this category are widely recognized for delivering effective glucose control while supporting additional therapeutic outcomes related to cardiovascular health and body weight management. Pharmaceutical companies have strengthened the market presence of GLP-1 receptor agonists through continued product development and expanded global distribution strategies. As these therapies demonstrate reliable outcomes in managing chronic metabolic conditions, healthcare providers are increasingly integrating them into routine treatment plans. Their growing acceptance in both diabetes care and weight-related metabolic management continues to reinforce the segment's leadership within the incretin-based drugs industry.

Based on route of administration, the oral segment held a 76.7% share in 2025. Oral incretin therapies provide a convenient alternative to injectable formulations, which play an important role in improving patient adherence to long-term treatment. Advancements in oral drug formulation technologies have contributed to improved therapeutic performance, safety profiles, and patient compliance. These medications are also easier to transport, store, and distribute across healthcare facilities, making them suitable for diverse medical environments. Unlike injectable treatments, oral therapies do not require specialized training for self-administration, which helps reduce the burden on healthcare professionals while simplifying treatment routines for patients. In addition, many individuals prefer oral medications because they are more convenient and less invasive.

North America Incretin-based Drugs Market accounted for 45.7% share in 2025. The region continues to demonstrate significant growth potential, primarily due to the increasing number of individuals diagnosed with type 2 diabetes mellitus. The expanding patient population is driving demand for advanced therapeutic solutions capable of delivering sustained blood glucose management while addressing related metabolic challenges. Healthcare providers across the region are increasingly prescribing incretin-based therapies as part of comprehensive diabetes management strategies. These treatments offer effective long-term glycemic control and provide additional benefits such as weight management, which are highly relevant for patients dealing with chronic metabolic conditions. As the healthcare system focuses on improving long-term disease outcomes, incretin-based drugs are gaining broader acceptance among clinicians throughout North America.

Key participants operating in the Global Incretin-based Drugs Market include AstraZeneca, Boehringer Ingelheim, Eli Lilly and Company, Merck, Novo Nordisk, Pfizer, Sanofi, Takeda Pharmaceutical Company, and Teva Pharmaceuticals. Companies active in the Incretin-based Drugs Market are implementing several strategic initiatives to reinforce their competitive position and expand global reach. Major pharmaceutical firms are prioritizing research and development investments to advance innovative formulations and improve therapeutic performance. Strategic partnerships and collaborative agreements with research institutions and biotechnology firms are also becoming common, allowing companies to accelerate drug development and expand product pipelines. Market participants are strengthening their presence in emerging healthcare markets through distribution expansion and localized commercialization strategies. In addition, organizations are focusing on regulatory approvals and clinical trials to support new product introductions and broaden therapeutic indications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.10 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Drug type trends

- 2.2.2 Route of Administration trends

- 2.2.3 Indication trends

- 2.2.4 Distribution channel trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Rising prevalence of type 2 diabetes mellitus

- 3.2.3 Shift toward non-insulin therapies

- 3.2.4 Advancements in drug delivery technologies

- 3.2.5 Cardiovascular and weight management benefits

- 3.2.6 Industry pitfalls and challenges

- 3.2.7 High treatment costs

- 3.2.8 Adverse effects and contraindications

- 3.2.9 Market opportunities

- 3.2.9.1 Growing patient awareness and cultural shifts in obesity management

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 GLP-1 receptor agonists

- 5.3 DPP-4 inhibitors

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Injectable

Chapter 7 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Type 2 diabetes mellitus

- 7.3 Obesity and weight management

- 7.4 Other metabolic disorders

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Boehringer Ingelheim

- 10.3 Eli Lilly and Company

- 10.4 GlaxoSmithKline

- 10.5 Merck

- 10.6 Novo Nordisk

- 10.7 Pfizer

- 10.8 Sanofi

- 10.9 Takeda Pharmaceutical Company

- 10.10 Teva Pharmaceuticals