PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998769

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998769

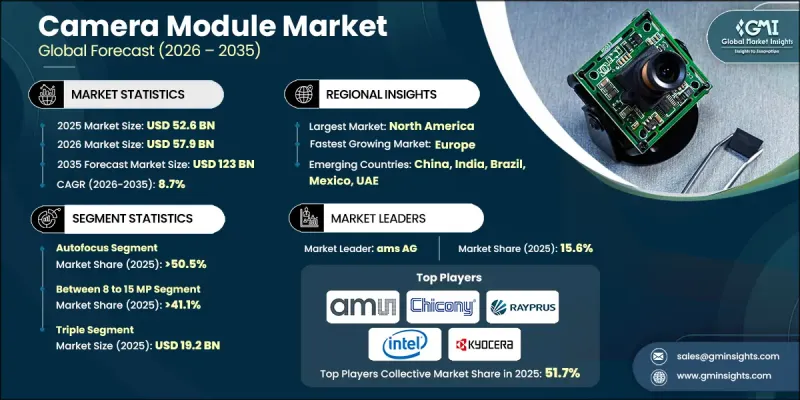

Camera Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Camera Module Market was valued at USD 52.6 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 123 billion by 2035.

The market is driven by the rapid expansion of consumer electronics, including smartphones, tablets, laptops, and wearables, where advanced imaging capabilities have become a key differentiator. Manufacturers are increasingly integrating multi-camera setups, high-resolution sensors, and sophisticated optical technologies to deliver superior imaging experiences. Growth is further fueled by the widespread adoption of advanced driver-assistance systems (ADAS) and autonomous vehicle technologies, where camera modules are critical for lane departure warnings, parking assistance, driver monitoring, and surround-view systems. Increasing safety regulations and demand for intelligent mobility solutions are prompting automakers to install multiple cameras per vehicle. Beyond consumer electronics, the rising deployment of camera modules in security, surveillance, and smart city infrastructure is supporting market expansion. Governments, enterprises, and home users are investing in networked video monitoring systems to improve public safety, asset protection, and traffic management, reinforcing the overall market momentum.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $52.6 Billion |

| Forecast Value | $123 Billion |

| CAGR | 8.7% |

The autofocus segment accounted for 50.5% share in 2025, driven by smartphones adopting AI-powered phase detection for rapid focusing, enhanced low-light performance, and accurate subject tracking. Manufacturers are emphasizing VCM-based autofocus systems, miniaturized high-resolution sensors, automated multi-camera assembly, AI low-light processing, and supply chain resilience against semiconductor shortages.

The above 15 MP segment is projected to grow at a CAGR of 9.8% through 2026-2035, propelled by demand for computational photography, 8K video, high-quality zoom in smartphones, and detailed imaging for ADAS and surveillance systems. Key focus areas include advanced sensor stacking, optical image stabilization (OIS) integration, and AI-driven computational photography optimization.

North America Camera Module Market held a 22.9% share in 2025, led by strong adoption of multi-camera smartphones, expanding ADAS/autonomous vehicle deployment, and growing IoT and security applications. Companies are leveraging R&D in high-resolution, low-light modules, AI-enhanced imaging, localizing supply chains, and forming OEM partnerships to support EVs and security solutions.

Prominent players operating in the Global Camera Module Market include ams AG, Chicony Electronics Co., Ltd., Intel, Kyocera Corporation, LG Innotek, MCNEX Co., Ltd., OFILM Group Co., Ltd., OmniVision, Onsemi, Q Technology, Rayprus Holding Ltd. (Foxconn), Samsung Electro-Mechanics, Sony, STMicroelectronics N.V., Sunny Optical Technology (Group), and Toshiba Corporation. Companies in the Global Camera Module Market strengthen their position by focusing on technological innovation, including high-resolution, low-power sensors, AI-enabled imaging, and advanced optics. Strategic collaborations with smartphone, automotive, and IoT OEMs expand market penetration. Firms invest in R&D for ADAS and autonomous vehicle sensors, computational photography, and low-light imaging. Supply chain localization reduces dependence on Asia, ensuring production stability. Product diversification across smartphones, wearables, automotive, and security segments allows companies to reach multiple markets. Additionally, patenting proprietary technologies and optimizing assembly automation enhance efficiency and secure competitive advantage, while emphasizing energy-efficient, sustainable designs to meet regulatory and consumer demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Offering type trends

- 2.2.2 Focus type trends

- 2.2.3 Pixel trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of GigE Vision networking

- 3.2.1.2 Growth of edge AI vision processing

- 3.2.1.3 Increasing demand for real-time and deterministic communication

- 3.2.1.4 Expansion of multi-camera synchronization protocols

- 3.2.1.5 Growing need for PoE power delivery

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Sensor Deployment Costs

- 3.2.2.2 Complex Network Synchronization

- 3.2.3 Market opportunities

- 3.2.3.1 GigE Vision Scalability

- 3.2.3.2 PoE Network Simplification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends,

- 5.2 Single

- 5.3 Dual

- 5.4 Triple

- 5.5 Quad

Chapter 6 Market Estimates & Forecast, By Focus Type, 2022 - 2035 (USD Million)

- 6.1 Key trends,

- 6.2 Autofocus

- 6.3 Fixed Focus

Chapter 7 Market Estimates & Forecast, By Pixel, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Upto 7 MP

- 7.3 Between 8 to 15 MP

- 7.4 Above 15 MP

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Consumer electronics

- 8.1.1 Smartphone

- 8.1.2 Tablet

- 8.1.3 Cameras

- 8.1.4 Gaming Devices

- 8.1.5 Others (Wearables, etc.)

- 8.2 Automotive

- 8.3 Industrial

- 8.4 Security & Surveillance

- 8.5 Aerospace & Defence

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Automotive Manufacturing

- 9.3 Semiconductor & Electronics

- 9.4 Pharmaceutical & Biotechnology

- 9.5 Food & Beverage

- 9.6 Oil & Gas

- 9.7 Pulp & Paper

- 9.8 Mining & Metals

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends, by region

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia-Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Sony

- 11.1.2 Samsung Electro-Mechanics

- 11.1.3 LG Innotek

- 11.2 Regional Players

- 11.2.1 ams AG

- 11.2.2 Chicony Electronics Co., Ltd.

- 11.2.3 Intel

- 11.2.4 Kyocera Corporation

- 11.3 Emerging Players

- 11.3.1 MCNEX Co., Ltd.

- 11.3.2 OFILM Group Co., Ltd.

- 11.3.3 OmniVision

- 11.3.4 Onsemi

- 11.3.5 Q Technology

- 11.3.6 Rayprus Holding Ltd. (Foxconn)

- 11.3.7 STMicroelectronics N.V.

- 11.3.8 Sunny Optical Technology (Group)

- 11.3.9 Toshiba Corporation