PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998775

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998775

Rapid Influenza Diagnostic Tests (RIDT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

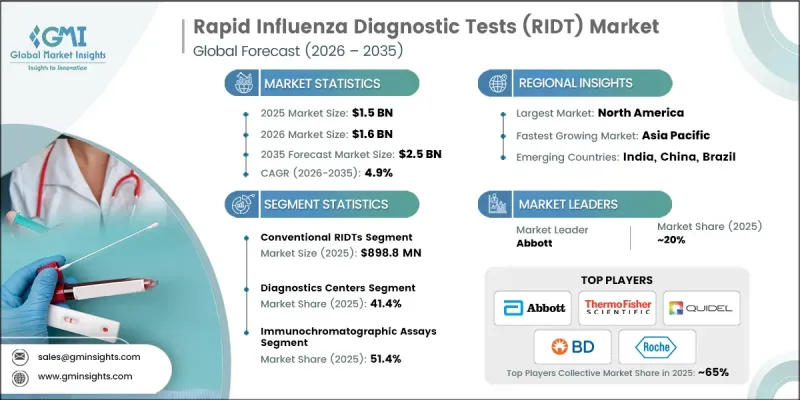

The Global Rapid Influenza Diagnostic Tests (RIDT) Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 2.5 billion by 2035.

Rapid influenza diagnostic tests help in the quick detection of influenza infections, enabling healthcare professionals to initiate treatment and preventive measures at an early stage. Growing acceptance of rapid diagnostic technologies, continuous technological progress, and increasing emphasis on timely disease identification are contributing significantly to market growth. Improvements in diagnostic technologies have strengthened the reliability of these tests by enhancing sensitivity and specificity, making them increasingly valuable in clinical practice. The transition from traditional qualitative testing toward semi-quantitative diagnostic approaches is also improving clinical assessment capabilities. Furthermore, the development of multiplex diagnostic solutions capable of identifying influenza alongside other respiratory infections has enhanced the overall usefulness of these tests in healthcare settings. Emerging digital technologies, including artificial intelligence and machine learning, are further supporting this evolution by enabling automated result interpretation and minimizing the risk of human error. At the same time, rising investments in healthcare infrastructure are improving the availability and accessibility of rapid influenza diagnostic tests for a larger patient population.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 4.9% |

Public health authorities across multiple regions are strengthening disease monitoring and diagnostic capabilities to manage the impact of influenza more effectively. Several global health initiatives emphasize the importance of accurate and early detection of influenza infections to support effective disease surveillance and response efforts. Regulatory organizations are also encouraging the adoption of rapid influenza diagnostic technologies by accelerating approval pathways and supporting the availability of advanced diagnostic solutions.

The conventional rapid influenza diagnostic tests segment generated USD 898.8 million in 2025. This segment continues to maintain a strong presence due to its ability to deliver results more quickly than many advanced molecular testing approaches. Conventional tests remain widely adopted because they are cost-effective and easily accessible for healthcare providers. Their relatively simple manufacturing process and minimal infrastructure requirements make them suitable for a broad range of healthcare environments. In addition, the affordability of these tests supports public health screening programs in regions where healthcare budgets are limited. Conventional rapid influenza diagnostic tests are also valued for their ease of use, as they can be administered without extensive technical training. Their ability to produce results within a short time frame allows healthcare professionals to make timely clinical decisions, which is particularly important during periods of increased influenza transmission.

The immunochromatographic assays segment held a 51.4% share in 2025. These diagnostic methods have gained considerable acceptance because of their strong analytical performance, including high levels of sensitivity and specificity. Their capability to detect relatively small viral concentrations supports accurate identification of infections during the early stages of illness. Early detection is particularly important for individuals who may face higher risks of complications from influenza infections. Immunochromatographic assays are also increasingly utilized in decentralized healthcare environments due to their compact design and minimal equipment requirements. Their portability and operational simplicity make them practical diagnostic tools in settings where laboratory infrastructure may be limited. Technological improvements have further enhanced the speed and reliability of these assays, which have contributed to growing preference among healthcare professionals seeking efficient and dependable influenza testing solutions.

United States Rapid Influenza Diagnostic Tests (RIDT) Market reached USD 479.3 million in 2025, positioning the country as the largest contributor within the North American region. Strong healthcare frameworks, widespread awareness of influenza prevention and diagnosis, and substantial investment in diagnostic technologies continue to support market expansion in the country. The growing availability of influenza testing services across multiple healthcare access points has improved convenience for patients seeking a timely diagnosis. Additionally, national preparedness initiatives aimed at strengthening response strategies for influenza outbreaks have encouraged broader adoption of rapid diagnostic testing technologies. The presence of established diagnostic manufacturers and the continued expansion of testing capabilities across healthcare networks are also supporting market development.

Key companies participating in the Global Rapid Influenza Diagnostic Tests (RIDT) Market include Abbott, Siemens Healthineers, Roche, Quidel Corporation, Thermo Fisher Scientific, bioMerieux, Becton, Dickinson and Company (BD), DiaSorin, Meridian, Access Bio, CHEMBIO, 3B BlackBio, and SEKISUI. Companies operating in the Rapid Influenza Diagnostic Tests (RIDT) Market are adopting a range of strategies to strengthen their competitive position and expand their market presence. A major focus remains on research and development activities aimed at improving test sensitivity, accuracy, and speed. Many manufacturers are investing in advanced diagnostic technologies such as digital testing platforms and multiplex detection systems to enhance clinical value. Strategic collaborations with healthcare providers and diagnostic laboratories are helping companies broaden product adoption and improve distribution networks. In addition, organizations are expanding manufacturing capacity and strengthening supply chains to meet increasing global demand for rapid testing solutions. Companies are also emphasizing regulatory approvals and quality certifications to support product credibility and market entry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Technology trends

- 2.2.4 Sample type trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of influenza

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising demand for early influenza diagnosis and management

- 3.2.1.4 Increasing popularity of rapid diagnostic tests

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals

- 3.2.2.2 Stringent regulatory approvals

- 3.2.3 Opportunities

- 3.2.3.1 AI-enhanced interpretation tools for better accuracy

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by primary research)

- 3.6 Future market trends (Driven by primary research)

- 3.7 Consumer behavior analysis

- 3.8 Value chain analysis

- 3.9 Pricing analysis, by products, 2025 (Driven by primary research)

- 3.10 Impact of AI & generative AI on the market (Driven by primary research)

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Gap analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Conventional RIDTs

- 5.3 Digital RIDTs

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Immunochromatographic assays

- 6.3 Lateral flow assays

- 6.4 Polymerase Chain Reaction

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Sample Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Nasal Swab

- 7.3 Throat Swab

- 7.4 Other samples

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostics centers

- 8.3 Hospitals

- 8.4 Research laboratories

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3B BlackBio

- 10.2 Abbott

- 10.3 Access Bio

- 10.4 Becton, Dickinson and Company (BD)

- 10.5 bioMerieux

- 10.6 CHEMBIO

- 10.7 DiaSorin

- 10.8 Meridian

- 10.9 Quidel Corporation

- 10.10 Roche

- 10.11 SEKISUI

- 10.12 Siemens Healthineers

- 10.13 Thermo Fisher Scientific