PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998778

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998778

Stents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

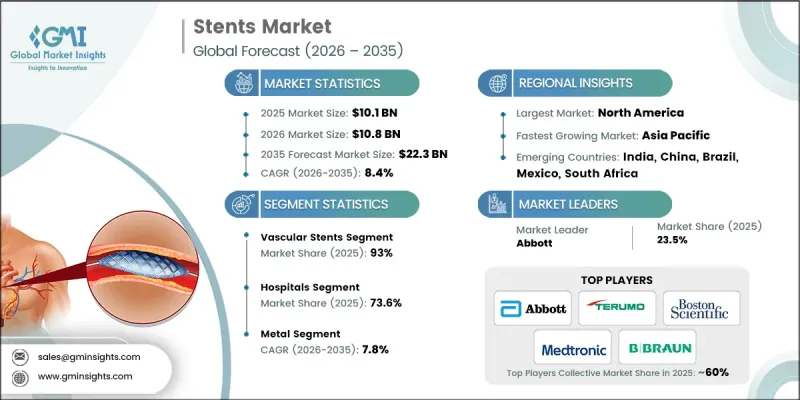

The Global Stents Market was valued at USD 10.1 billion in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 22.3 billion by 2035.

Market growth is driven by the rising prevalence of cardiovascular diseases, increasing adoption of minimally invasive procedures, technological advancements in stent design, and expanding healthcare infrastructure in emerging regions. Stents are small, tubular medical devices that maintain the patency of narrowed or blocked blood vessels, ensuring consistent blood flow and preventing vessel collapse. The growing incidence of coronary artery disease, peripheral artery disease, and aneurysms, combined with lifestyle factors such as sedentary behavior, poor diet, and smoking, fuels demand for stent procedures. Innovations, including drug-eluting stents, bioresorbable stents, and biodegradable polymer coatings, enhance patient outcomes, reduce restenosis, and improve procedural safety. The market is further propelled by patient-centric solutions, digital health integration, and the development of smart stents, which collectively expand treatment options and adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.1 Billion |

| Forecast Value | $22.3 Billion |

| CAGR | 8.4% |

The vascular stents segment held a share of 93% in 2025, driven by the widespread prevalence of coronary artery disease and preference for minimally invasive cardiovascular interventions. Endovascular stenting is favored over open surgical bypass due to shorter recovery times, lower complication risks, and reduced hospital stays. Expansion of cardiovascular care centers, availability of trained specialists, and growing awareness of early detection, particularly in Asia-Pacific, Latin America, and the Middle East, contribute to increasing adoption of vascular stents.

The hospitals segment accounted for 73.6% share in 2025, reaching USD 16 billion. Hospitals are increasingly performing percutaneous coronary interventions and endovascular procedures, as stent implantation shortens recovery periods, reduces procedural risks, and improves patient throughput. The rising number of patients with cardiovascular conditions due to aging populations and lifestyle-related risk factors is driving higher demand for stents in both cardiac and peripheral interventions.

U.S. Stents Market reached USD 3.5 billion in 2025. The increasing prevalence of coronary artery disease and peripheral artery disease, combined with aging demographics and lifestyle-related risks such as obesity, hypertension, and diabetes, drives procedural volumes. The presence of advanced hospitals, specialized cardiac centers, and catheterization labs facilitates high-volume stent implantation. Insurance coverage and reimbursement policies in the U.S. and Canada also encourage patients to undergo both elective and emergency procedures, further supporting market growth.

Prominent players in the Global Stents Market include Abbott, Medtronic, Boston Scientific, Biotronik, MicroPort Scientific, Stryker, W.L Gore & Associates, B. Braun, Biosensors International Group, Terumo, Veryan Medical, Elixir Medical, Johnson & Johnson, and SLTL Group. Companies in the Global Stents Market strengthen their presence by focusing on continuous research and development to improve stent design, durability, and safety features. They are expanding production capacities, forming strategic partnerships with hospitals and healthcare providers, and entering emerging markets to reach underserved populations. Firms emphasize minimally invasive and patient-specific solutions, integrate digital health technologies with smart stents, and launch drug-eluting and bioresorbable products to enhance clinical outcomes. Marketing initiatives, training programs for clinicians, and collaborations with key cardiovascular centers help companies build brand trust, drive adoption, and maintain a competitive edge in the global market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Material trends

- 2.2.4 Type trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases

- 3.2.1.2 Advancements in stent technology

- 3.2.1.3 Increasing number of minimally invasive procedures

- 3.2.1.4 Growing awareness about early diagnosis and treatment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of stent procedures

- 3.2.2.2 Risk of complications and restenosis

- 3.2.3 Market opportunities

- 3.2.3.1 Development of bioresorbable and next-gen stents

- 3.2.3.2 Increasing adoption of digital health and AI in diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario (Driven by primary research)

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Consumer insights (Driven by primary research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Vascular stents

- 5.2.1 Coronary stents

- 5.2.1.1 Drug eluting stent

- 5.2.1.2 Bioresorbable vascular scaffold (BVS)

- 5.2.1.3 Bare metal stent

- 5.2.2 Peripheral stents

- 5.2.2.1 Renal

- 5.2.2.2 Iliac

- 5.2.2.3 Femoral-popliteal

- 5.2.2.4 Carotid

- 5.2.3 Neurovascular stents

- 5.2.1 Coronary stents

- 5.3 Non-vascular stents

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Polymer

Chapter 7 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Balloon expandable

- 7.3 Self expandable

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 B. Braun

- 10.3 Becton, Dickinson and Company

- 10.4 Biosensors International Group

- 10.5 Biotronik

- 10.6 Boston Scientific

- 10.7 Elixir Medical

- 10.8 Medtronic

- 10.9 Meril Life Science

- 10.10 MicroPort Scientific

- 10.11 SLTL Group

- 10.12 Stryker

- 10.13 Terumo

- 10.14 Veryan Medical

- 10.15 W.L Gore & Associates