PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998786

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998786

Unmanned Marine Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

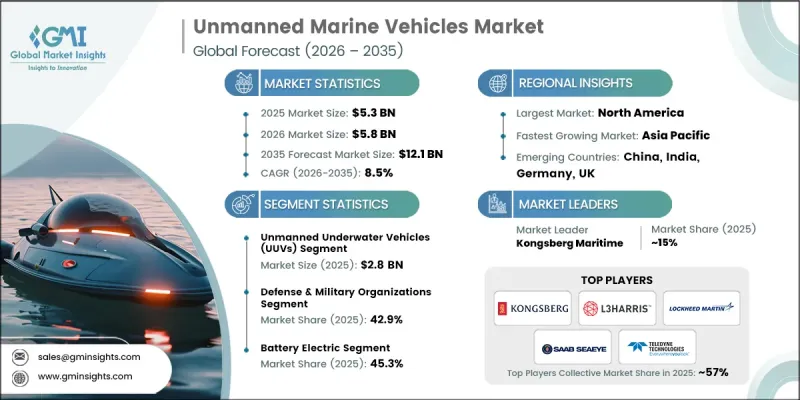

The Global Unmanned Marine Vehicles Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 12.1 billion by 2035.

Market expansion is fueled by increasing naval fleet modernization programs, growing demand for persistent maritime border surveillance, and heightened anti-submarine warfare capabilities. Rising offshore energy inspections, particularly in deepwater oil and gas operations, alongside accelerating offshore wind farm development, are further strengthening adoption. Advancements in autonomous navigation, AI-driven mission systems, and secure maritime communications are driving technological innovation in the sector. The integration of digital twins allows operators to simulate vehicle performance and mission conditions in real time, improving operational efficiency. Interoperable and open-architecture mission systems enable multi-vendor unmanned platforms to function within unified command structures. These trends, which gained traction around 2021, are expected to continue through 2030, supporting flexible fleet growth and rapid capability upgrades.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $12.1 Billion |

| CAGR | 8.5% |

The unmanned underwater vehicles (UUVs) segment reached USD 2.8 billion in 2025. UUVs are extensively deployed in naval mine countermeasure missions, anti-submarine warfare, hydrographic mapping, and offshore energy inspections. Their ability to operate at significant depths, perform long-endurance missions without surface visibility, and capture high-resolution seabed data makes them indispensable for both defense and offshore energy operations.

The fuel cell-powered segment is expected to grow at a CAGR of 14.6% through 2035. Fuel cells provide extended operational endurance for unmanned surface vehicles, reducing the need for frequent refueling during persistent surveillance or offshore servicing operations. Increasing investments in maritime decarbonization and alternative propulsion technologies are accelerating the development and early deployment of fuel cell-powered marine platforms.

North America Unmanned Marine Vehicles Market held a 33.1% share in 2025. Market growth in the region is driven by heightened focus on maritime security, protection of offshore assets, and naval modernization initiatives. Persistent ISR, mine countermeasure, and environmental surveillance missions are driving adoption among defense agencies, coast guards, and offshore energy operators. Advanced autonomous navigation, AI-based mission systems, and modular unmanned platforms are increasing operational efficiency, while collaborations with technology companies are further enhancing capabilities. North America is expected to maintain leadership in innovation and deployment of unmanned marine vehicles through 2035.

Prominent players operating in the Global Unmanned Marine Vehicles Market include BlueZone Group, AutoNaut Ltd, Deep Ocean Engineering, Inc., Elbit Systems Ltd., Exail Technologies, International Submarine Engineering Ltd., Kongsberg Maritime, L3Harris Technologies, Inc., Lockheed Martin Corporation, Maritime Robotics AS, Ocean Aero, Ocius Technology Ltd, Saab Seaeye, Saildrone, Inc., and Teledyne Technologies Incorporated. Companies in the Global Unmanned Marine Vehicles Market are pursuing multiple strategies to consolidate their market position and enhance competitiveness. They are investing heavily in R&D to develop AI-enabled autonomous systems, fuel cell propulsion platforms, and next-generation underwater and surface vehicles. Strategic partnerships with defense organizations, offshore energy operators, and technology firms enable integration of cutting-edge unmanned solutions into operational fleets. Companies are also expanding production capacity, establishing regional service hubs, and offering training programs to improve customer support. Modular design, open-architecture mission systems, and digital twin integration allow rapid upgrades and fleet interoperability, strengthening adoption in defense, research, and commercial sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Vehicle type trends

- 2.2.2 Primary energy source trends

- 2.2.3 Autonomy level trends

- 2.2.4 Vehicle size trends

- 2.2.5 End user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising naval ISR and mine countermeasure modernization programs

- 3.2.1.2 Maritime border surveillance and anti-submarine warfare needs

- 3.2.1.3 Deepwater oil & gas asset integrity inspections

- 3.2.1.4 Offshore wind farm inspection and subsea cable monitoring demand

- 3.2.1.5 Integration of AI-enabled autonomous navigation systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory uncertainty for autonomous maritime operations

- 3.2.2.2 Limited battery endurance for long-duration missions

- 3.2.3 Market opportunities

- 3.2.3.1 Swarm-enabled multi-vehicle coordinated missions

- 3.2.3.2 Hybrid propulsion and hydrogen-powered USVs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Unmanned surface vehicles (USVs)

- 5.3 Unmanned underwater vehicles (UUVs)

- 5.4 Hybrid surface-underwater vehicles

Chapter 6 Market Estimates and Forecast, By Primary Energy Source, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Battery electric

- 6.3 Combustion-based

- 6.4 Fuel cell-based

- 6.5 Renewable-driven

Chapter 7 Market Estimates and Forecast, By Autonomy Level, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Remotely operated

- 7.3 Autonomous

Chapter 8 Market Estimates and Forecast, By Vehicle Size, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Small (< 5 meters)

- 8.3 Medium (5-15 meters)

- 8.4 Large (> 15 meters)

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Defense & military organizations

- 9.3 Offshore energy operators

- 9.4 Commercial marine service providers

- 9.5 Civil government maritime authorities

- 9.6 Research & academic institutions

- 9.7 Port & harbor authorities

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Kongsberg Maritime

- 11.1.2 Lockheed Martin Corporation

- 11.1.3 Saab Seaeye

- 11.1.4 L3Harris Technologies, Inc.

- 11.1.5 Teledyne Technologies Incorporated

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Saildrone, Inc.

- 11.2.1.2 Elbit Systems Ltd.

- 11.2.1.3 Deep Ocean Engineering, Inc.

- 11.2.2 Asia Pacific

- 11.2.2.1 Exail Technologies

- 11.2.2.2 International Submarine Engineering Ltd.

- 11.2.2.3 Ocean Aero

- 11.2.3 Europe

- 11.2.3.1 Maritime Robotics AS

- 11.2.3.2 Ocius Technology Ltd

- 11.2.3.3 AutoNaut Ltd

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 BlueZone Group