PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998793

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998793

Automotive Smart Key Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

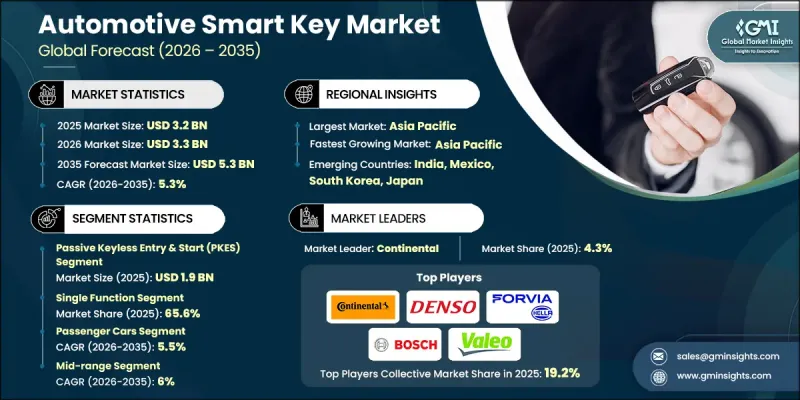

The Global Automotive Smart Key Market was valued at USD 3.2 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 5.3 billion by 2035. The automotive smart key industry is evolving rapidly as the automotive sector continues shifting from traditional mechanical key systems toward digitally connected vehicle access technologies. Declining component costs and rising consumer expectations for convenience and connectivity are accelerating the integration of smart key solutions across a wider range of vehicle segments. Modern automotive access systems are no longer limited to simple unlocking functions, as they are increasingly integrated with broader digital ecosystems that connect vehicles with smartphones, mobile applications, and cloud-based platforms. This transformation is influencing both product development strategies and the broader automotive technology landscape. As vehicles become more software-driven, digital access systems are expected to play a larger role in enabling seamless user experiences and improving overall vehicle security. Manufacturers are increasingly prioritizing the development of advanced authentication mechanisms and secure communication protocols to address evolving cybersecurity concerns. Continuous advancements in wireless communication technologies, encrypted signal transmission, and intelligent vehicle access platforms are further strengthening the growth of the automotive smart key market. In addition, the rising demand for enhanced vehicle convenience features and digital mobility services is encouraging automakers to incorporate smart key solutions across various vehicle categories.

As vehicles continue to rely more heavily on software-defined technologies, compliance standards and certification frameworks have become essential to maintaining system security and operational reliability within the automotive smart key market. These regulatory requirements help ensure that vehicle access technologies meet strict cybersecurity protocols and safety benchmarks. Strong encryption frameworks and secure authentication mechanisms are becoming essential components of smart key systems to protect sensitive user data and prevent unauthorized vehicle access. Advanced technological developments are also shaping the future of the automotive smart key industry. Emerging wireless technologies such as ultra-wideband positioning, near-field communication, and advanced encrypted communication protocols are enhancing the functionality and security of smart key solutions. These innovations allow vehicles to accurately detect the proximity and location of a key device, significantly reducing the risk of signal interception and unauthorized access. At the same time, the increasing focus on secure hardware infrastructure is encouraging semiconductor manufacturers and automotive suppliers to expand the production of advanced secure element chips designed specifically for vehicle access systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 5.3% |

The passive keyless entry and start (PKES) segment held 59% share, generating USD 1.9 billion in 2025. Passive keyless entry and start systems are widely adopted due to the convenience they provide to vehicle owners. These systems allow drivers to unlock doors and start the engine automatically when the key device is within a specific proximity, eliminating the need for manual key usage. Such features simplify everyday vehicle access and improve the overall driving experience. In addition to convenience, PKES systems incorporate multiple layers of security to protect vehicles from unauthorized access. Advanced encrypted communication protocols ensure that signals exchanged between the vehicle and the smart key remain secure. These systems also rely on proximity detection technologies supported by low-frequency and radio-frequency communication methods that allow vehicles to identify the presence of an authorized key device accurately.

The single-function segment accounted for 65.6% share in 2025 and is projected to reach USD 3.3 billion by 2035. A single-function automotive smart key is designed to perform one primary operation, typically enabling either keyless entry or engine ignition. These keys provide a straightforward and user-friendly solution that focuses on delivering basic convenience without integrating multiple advanced features. Their compact design makes them easy to carry and practical for daily use. In addition, these smart keys are engineered with low-power standby modes that help extend battery life and improve device efficiency. Consumers often prefer single-function smart keys because they offer reliable vehicle access capabilities at a relatively affordable cost. Their simplicity also makes them suitable for a wide range of vehicles, particularly entry-level and mid-range models. These keys typically support fundamental vehicle access functions such as locking and unlocking doors remotely while maintaining essential anti-theft protections.

United States Automotive Smart Key Market generated USD 740.4 million in 2025 and is projected to grow at a CAGR of 4.6% between 2026 and 2035. The United States represents a key market within the North America automotive smart key industry due to the growing adoption of connected vehicle technologies and advanced automotive electronics. Automotive manufacturers operating in the region are increasingly integrating smart access systems into their vehicle platforms as part of broader digital mobility strategies. Consumer demand for improved vehicle convenience, enhanced safety features, and integrated digital services is encouraging automakers to expand the use of smart key technologies across multiple vehicle segments. As a result, smart keys are becoming increasingly common not only in premium vehicles but also in mid-range automobile categories. Technological innovations such as ultra-wideband communication, near-field connectivity, and wireless authentication technologies are further improving the functionality and reliability of these systems.

Key companies operating in the Global Automotive Smart Key Market include Alps Alpine, Bosch, Continental, Denso, Forvia HELLA, Huf Hulsbeck & Furst, Lear, Tokai Rika, Valeo, and ZF Friedrichshafen. Companies participating in the Global Automotive Smart Key Market are focusing on multiple strategic initiatives to strengthen their market presence and maintain technological competitiveness. Many organizations are increasing investments in research and development to design more secure and intelligent vehicle access systems. Technology innovation is a major priority, with companies developing advanced encryption technologies, wireless authentication systems, and integrated digital key platforms that improve both security and user convenience. Strategic collaborations with automotive manufacturers are also becoming increasingly common, allowing technology providers to integrate their solutions directly into next-generation vehicle platforms. In addition, companies are working to expand their semiconductor and electronic component capabilities to support the growing demand for secure hardware solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Function

- 2.2.4 Vehicle

- 2.2.5 Vehicle Class

- 2.2.6 Vehicle Powertrain

- 2.2.7 Distribution Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Consumer Demand For Vehicle Security & Convenience Features

- 3.2.1.2 OEM integration of keyless entry systems in mid-range & economy segments

- 3.2.1.3 Proliferation of electric vehicles driving smart key adoption

- 3.2.1.4 Government mandates on vehicle safety & anti-theft technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity vulnerabilities & relay attack concerns

- 3.2.2.2 Aftermarket installation challenges & compatibility issues

- 3.2.3 Market opportunities

- 3.2.3.1 Ultra-Wideband (UWB) technology adoption for enhanced security

- 3.2.3.2 Integration with smart city & mobility-as-a-service (MaaS) ecosystems

- 3.2.3.3 Biometric authentication feature upgrades in luxury segment

- 3.2.3.4 Smartphone penetration enabling mobile-based digital key solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Federal Motor Vehicle Safety Standards (FMVSS)

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 WP.29 / UNECE

- 3.4.2.3 Cyber Resilience Act (EU)

- 3.4.3 Asia Pacific

- 3.4.3.1 India Connected Vehicle Cybersecurity Framework

- 3.4.3.2 China GB 44495 - Vehicle Cybersecurity Standard

- 3.4.3.3 Japan Automotive Cybersecurity Guidelines (JAMA / JAPIA)

- 3.4.4 Latin America

- 3.4.4.1 Brazil Rota 2030 Automotive Policy

- 3.4.4.2 National Data Protection Regulations

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Regulatory Framework on Vehicle Safety & Cybersecurity

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.1 North America

- 3.5 Investment & Funding Analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 Passive Keyless Entry (PKE) Systems

- 3.8.1.2 Over-the-Air (OTA) Firmware Updates

- 3.8.1.3 Multi-Function Smart Key Platforms

- 3.8.2 Emerging technologies

- 3.8.2.1 Smartphone-Based Digital Key Solutions

- 3.8.2.2 Ultra-Wideband (UWB)

- 3.8.2.3 Integrated Biometric Authentication

- 3.8.2.4 Wearable and Auxiliary Device Integration

- 3.8.1 Current technological trends

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Integration with Connected Vehicle & IoT Ecosystems

- 3.12.1 V2X Communication Protocol Integration

- 3.12.2 Cloud Platform & Data Analytics Integration

- 3.12.3 Smart & Digital Ecosystem Interoperability

- 3.13 Mitigation of Wireless Signal Interception Threats

- 3.13.1 Relay Attack Prevention Technologies

- 3.13.2 Encryption & Authentication Protocol Evolution

- 3.13.3 Ultra-Wideband (UWB) & Secure Ranging Solutions

- 3.14 Case studies

- 3.15 Future outlook & opportunities

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Remote Keyless Entry (RKE)

- 5.3 Passive Keyless Entry & Start (PKES)

- 5.4 Biometric Entry Systems

- 5.5 Mobile/Digital Key

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Function, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Single Function

- 6.3 Multi-Function

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Economy/entry-level

- 8.3 Mid-range

- 8.4 Premium/luxury

Chapter 9 Market Estimates & Forecast, By Vehicle Powertrain, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 EV/Hybrid

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Russia

- 11.3.8 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Singapore

- 11.4.7 Malaysia

- 11.4.8 Vietnam

- 11.4.9 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Continental

- 12.1.2 Denso

- 12.1.3 Valeo

- 12.1.4 ZF Friedrichshafen

- 12.1.5 Forvia HELLA

- 12.1.6 Tokai Rika

- 12.1.7 Huf Hulsbeck & Furst

- 12.1.8 Lear

- 12.1.9 Bosch

- 12.1.10 Alps Alpine

- 12.2 Regional players

- 12.2.1 Minda

- 12.2.2 Alpha

- 12.2.3 Honda Lock

- 12.2.4 U-Shin

- 12.2.5 Strattec Security

- 12.2.6 Marquardt

- 12.3 Emerging players

- 12.3.1 TEQ

- 12.3.2 Thales

- 12.3.3 Automotive Key Solutions

- 12.3.4 Infineon