PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998798

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998798

Europe Elevators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

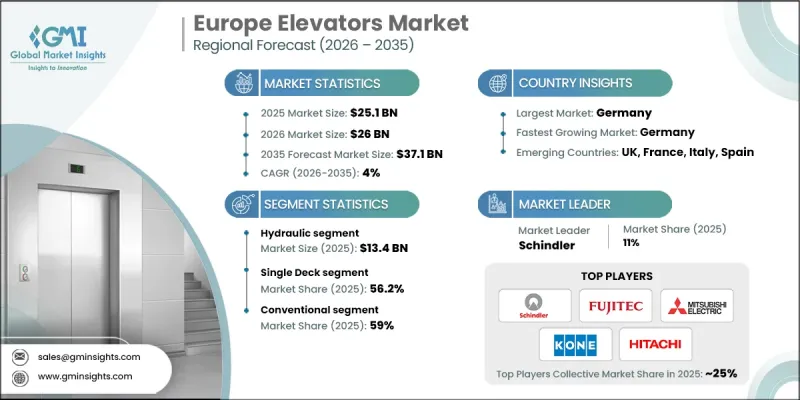

Europe Elevators Market was valued at USD 25.1 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 37.1 billion by 2035.

Market growth is influenced by the rapid integration of intelligent and energy-efficient elevator technologies in modern buildings. Digital transformation within the building infrastructure sector has encouraged the use of advanced elevator systems that incorporate connected technologies and automated operational capabilities. Smart elevators equipped with connected monitoring systems, predictive maintenance tools, and advanced operational functions are becoming increasingly common in both new developments and modernization projects. These solutions enhance building safety, operational efficiency, and passenger convenience. In addition, the growing demand for compact and flexible elevator solutions is accelerating the adoption of modern elevator designs. Building developers and property owners are focusing on technologies that improve space utilization while lowering long-term operating costs. As a result, advanced elevator systems designed for energy efficiency, improved safety, and optimized building integration are gaining widespread acceptance, supporting long-term expansion of the Europe elevators market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $25.1 Billion |

| Forecast Value | $37.1 Billion |

| CAGR | 4% |

A notable trend influencing the Europe elevators industry is the rising adoption of Machine Room Less elevator systems and other technologically advanced configurations. These elevator designs eliminate the requirement for a separate machine room, allowing better use of building space while offering greater architectural flexibility. Their streamlined structure allows easier installation within both new developments and renovation projects. In addition, these systems are recognized for their lower energy consumption and reduced maintenance requirements, which increases their attractiveness for property developers and facility managers. Advanced elevator engineering, including modern traction technologies, upgraded cabin structures, and enhanced safety mechanisms, is further strengthening the demand for innovative solutions across the European construction sector. As building owners increasingly prioritize efficient space utilization and lifecycle cost optimization, compact and technologically advanced elevator systems are becoming a preferred choice throughout the Europe elevators market.

The hydraulic elevators segment generated USD 13.4 billion in 2025 and is expected to grow at a CAGR of 3.6% between 2026 and 2035. Hydraulic elevator systems are widely utilized in buildings with limited height due to their practical design and cost efficiency. These elevators are often preferred because they offer relatively simple installation procedures and require less complex maintenance compared to other elevator technologies. Their operational structure allows installation in buildings with restricted space availability, which increases their appeal for developers and building planners working with structural limitations. Because they can function effectively without extensive infrastructure requirements, hydraulic elevators remain a practical solution for a wide range of building applications within the Europe elevators industry.

The single-deck segment held 56.2% share in 2025 and is expected to grow at a CAGR of 3.8% from 2026 to 2035. Single-deck elevators are widely adopted across various building categories due to their operational simplicity and economic advantages. These systems generally involve lower installation and maintenance costs compared with more complex elevator configurations, which makes them attractive for property owners seeking efficient vertical transportation solutions while maintaining cost control. Their compact design and straightforward operational mechanism also allow easier integration into different types of building layouts. As a result, single-deck elevators remain a widely used configuration within the Europe elevators market.

Germany Elevators Market generated USD 5.3 billion in 2025 and is expected to grow at a CAGR of 3.5% from 2026 to 2035. Urban development initiatives within the country are emphasizing the construction of modern, energy-efficient buildings and the modernization of existing infrastructure to meet evolving environmental and technological standards. This development strategy aligns with broader sustainability objectives and the growing integration of intelligent building technologies. Consequently, there is increasing demand for advanced elevator systems designed to improve building performance and passenger convenience. Modern elevator technologies that improve traffic flow efficiency and optimize operational performance are being integrated into both residential and commercial properties. These developments continue to support the growth of the elevator market in Germany.

Key companies participating in the Europe Elevators Market include Aritco, Canny Elevator, Electra Elevators, EMAK, ESCON Elevators, Fujitec, Hitachi, Hyundai Elevator, KONE, Mitsubishi Electric, Schindler, Schumacher Elevator, Sigma Elevator, TK Elevator, and Toshiba. Companies operating in the Europe Elevators Market are adopting a variety of strategic initiatives to strengthen their competitive position and expand their market footprint. Leading manufacturers are investing heavily in research and development to introduce advanced elevator systems with improved energy efficiency, enhanced safety features, and digital connectivity capabilities. Many companies are focusing on smart elevator technologies that incorporate remote monitoring, predictive maintenance, and automated traffic management to improve operational efficiency. Strategic partnerships with construction companies and real estate developers are also helping elevator manufacturers secure long-term installation contracts. In addition, businesses are expanding their service networks to support modernization and maintenance of existing elevator systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product

- 2.2.3 Deck type

- 2.2.4 Building height

- 2.2.5 Speed

- 2.2.6 Destination control

- 2.2.7 Business

- 2.2.8 Application

- 2.2.9 End use

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid urbanization & high-rise construction

- 3.2.1.2 Growing adoption of smart & energy-efficient technologies

- 3.2.1.3 Preference for machine room less (MRL) and advanced elevator designs

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial installation & modernization costs

- 3.2.2.2 Skilled labor shortage for modernization & maintenance

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for smart, connected & IoT enabled elevators

- 3.2.3.2 Sustainability & green building initiatives creating demand for eco-efficient elevators

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By country

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade data analysis

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of AI & generative ai on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 Genai use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Hydraulic

- 5.3 Traction

- 5.4 Machine room-less traction

Chapter 6 Market Estimates & Forecast, By Deck Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Single deck

- 6.3 Double deck

Chapter 7 Market Estimates & Forecast, By Building Height, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low-rise

- 7.3 Mid-rise

- 7.4 High-rise

Chapter 8 Market Estimates & Forecast, By Speed, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Less than 1m/s

- 8.3 Between 1 m/s to 3 m/s

- 8.4 Between 4 m/s to 6 m/s

- 8.5 Between 7 m/s to 10 m/s

- 8.6 Above 10 m/s

Chapter 9 Market Estimates & Forecast, By Destination Control, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Smart

- 9.3 Conventional

Chapter 10 Market Estimates & Forecast, By Business, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 New equipment

- 10.3 Maintenance

- 10.4 Modernization

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Passenger

- 11.3 Freight

Chapter 12 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Residential

- 12.2.1 Home lifts

- 12.2.2 Others

- 12.3 Industrial

- 12.4 Commercial

- 12.4.1 Office

- 12.4.2 Hotels

- 12.4.3 Healthcare

- 12.4.4 Others (Shopping malls)

Chapter 13 Market Estimates & Forecast, By Country, 2022 - 2035, (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 Germany

- 13.3 UK

- 13.4 France

- 13.5 Italy

- 13.6 Spain

- 13.7 Russia

Chapter 14 Company Profiles

- 14.1 Aritco

- 14.2 Canny Elevator

- 14.3 Electra Elevators

- 14.4 EMAK

- 14.5 ESCON Elevators

- 14.6 Fujitec

- 14.7 Hitachi

- 14.8 Hyundai Elevator

- 14.9 KONE

- 14.10 Mitsubishi Electric

- 14.11 Schindler

- 14.12 Schumacher Elevator

- 14.13 Sigma Elevator

- 14.14 TK Elevator

- 14.15 Toshiba