PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998805

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998805

Luxury Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

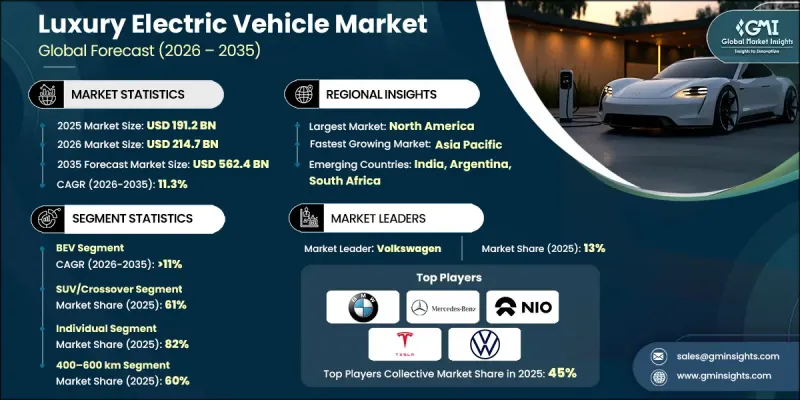

The Global Luxury Electric Vehicle Market was valued at USD 191.2 billion in 2025 and is estimated to grow at a CAGR of 11.3% to reach USD 562.4 billion by 2035.

Rapid electrification combined with premium brand positioning is accelerating demand for high-end electric mobility solutions. Affluent consumers are increasingly prioritizing sustainability while expecting uncompromised performance, refinement, and prestige. Automakers are responding with extended-range battery systems, advanced thermal management technologies, and high-output electric drivetrains that compete with or outperform traditional propulsion systems. Luxury electric vehicles are now positioned as both aspirational and environmentally responsible transportation choices for global high-net-worth buyers. Digital integration is further transforming the segment, as advanced connectivity, intelligent driver assistance technologies, and software-centric vehicle platforms enhance personalization and brand differentiation. Seamless connectivity, autonomous-ready systems, and continuous software enhancements are becoming central to the luxury ownership experience. This combination of technological sophistication, environmental responsibility, and premium craftsmanship is strengthening pricing power and brand loyalty across developed automotive markets, supporting sustained growth in the luxury electric vehicle industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $191.2 Billion |

| Forecast Value | $562.4 Billion |

| CAGR | 11.3% |

The battery electric vehicles segment accounted for 80% share in 2025 and is expected to grow at a CAGR of 11% from 2026 to 2035. Advances in high-capacity lithium-ion battery technology are reinforcing the segment's value proposition. Improvements in energy density, thermal regulation, and extended driving range exceeding 500 kilometers per charge are addressing the performance expectations of premium buyers. Enhanced acceleration capabilities and smooth, near-silent driving dynamics are further elevating the appeal of battery electric models among high-income consumers seeking refined and powerful mobility solutions.

The SUV and crossover models segment held a 61% share in 2025 and is forecast to grow at a CAGR of 11% during 2026-2035. Growing global preference for elevated driving positions, spacious interiors, and versatile design is significantly contributing to segment growth. Luxury electric SUVs deliver strong torque output, smooth acceleration, and advanced comfort features, making them attractive to affluent families and business professionals who value practicality alongside premium performance and cutting-edge mobility technologies.

United States Luxury Electric Vehicle Market held an 88% share, generating USD 59.2 billion in 2025. Strong consumer purchasing power and elevated disposable incomes are supporting rapid luxury EV adoption across the country. High-net-worth buyers are drawn to vehicles that combine advanced engineering, innovative technology, and sustainable performance. A culture of early technology adoption, supported by flexible financing and leasing structures, is enabling executives and professionals to invest in premium electric mobility without compromising convenience or lifestyle expectations.

Key companies operating in the Global Luxury Electric Vehicle Market include Tesla, Mercedes-Benz, BMW, Lucid, Rivian, Volkswagen, NIO, Jaguar, Lotus, and Li Auto. Companies in the Luxury Electric Vehicle Market are strengthening their competitive position through continuous innovation, brand differentiation, and strategic partnerships. Leading automakers are investing heavily in battery research, autonomous driving capabilities, and software-defined vehicle platforms to enhance performance and user experience. Strategic collaborations with technology firms are accelerating advancements in connectivity and digital ecosystems. Manufacturers are expanding production capacity and establishing dedicated EV platforms to improve scalability and cost efficiency. Premium branding initiatives emphasize sustainability, craftsmanship, and cutting-edge design to reinforce exclusivity. Companies are also broadening global distribution networks and investing in charging infrastructure partnerships to support customer convenience.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Vehicle

- 2.2.4 Ownership

- 2.2.5 Driving range

- 2.2.6 Price

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for premium sustainable mobility

- 3.2.1.2 Technological advancements in battery and ADAS

- 3.2.1.3 Expansion of fast-charging infrastructure

- 3.2.1.4 Brand electrification strategies

- 3.2.1.5 Increasing government incentives and emission regulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront vehicle cost

- 3.2.2.2 Battery raw material supply constraints

- 3.2.2.3 Charging infrastructure disparity

- 3.2.2.4 Technology obsolescence risks

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Asia Pacific luxury segment

- 3.2.3.2 Integration of solid-state batteries

- 3.2.3.3 Autonomous and connected mobility ecosystems

- 3.2.3.4 Subscription and digital sales models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 Occupational Safety and Health Administration (OSHA)

- 3.4.1.4 U.S. Department of Transportation (DOT)

- 3.4.1.5 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 EU Machinery Regulation

- 3.4.2.2 CE Marking Compliance

- 3.4.2.3 REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals)

- 3.4.2.4 EU Tire Labelling Regulation

- 3.4.2.5 National Type Approval & Road Homologation Requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 China Compulsory Certification (CCC)

- 3.4.3.2 Indian Central Motor Vehicle Rules (CMVR) - Off-Highway Tire Norms

- 3.4.3.3 Japanese Industrial Standards (JIS) for Tires

- 3.4.3.4 ASEAN Harmonized Technical Regulations

- 3.4.3.5 Australian Design Rules (ADR)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Institute of Metrology (INMETRO) Regulations

- 3.4.4.2 Brazilian National Traffic Council (CONTRAN)

- 3.4.4.3 Mexican NOM Tire Safety Standards

- 3.4.4.4 Regional Import & Certification Requirements

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO) Tire Regulations

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.3 South African National Regulator for Compulsory Specifications (NRCS)

- 3.4.5.4 National Road Traffic Act (NRTA) Compliance

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price analysis (Driven by Primary Research)

- 3.10.1 Historical Price Trend Analysis

- 3.10.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.11 Trade data analysis (Driven by Paid Database)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Cost breakdown analysis

- 3.13 Patent analysis (Driven by Primary Research)

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Impact of AI & generative AI on the market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Capacity & production landscape (Driven by Primary Research)

- 3.16.1 Installed capacity by region & key producer

- 3.16.2 Capacity utilization rates & expansion pipelines

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 BEV

- 5.3 PHEV

- 5.4 FCEV

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 SUV/Crossover

- 6.3 Sedan

- 6.4 Coupe

- 6.5 Convertible

- 6.6 Sports Car

Chapter 7 Market Estimates & Forecast, By Ownership, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Individual

- 7.3 Corporate & fleet

- 7.4 Subscription/Leasing

Chapter 8 Market Estimates & Forecast, By Driving Range, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Below 400 km

- 8.3 400-600 km

- 8.4 Above 600 km

Chapter 9 Market Estimates & Forecast, By Price, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 USD 80,000 - USD 149,999

- 9.3 USD 150,000 - USD 299,999

- 9.4 USD 300,000 - USD 499,999

- 9.5 Above 500,000

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Denmark

- 10.3.8 Finland

- 10.3.9 Norway

- 10.3.10 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Audi

- 11.1.2 BMW

- 11.1.3 Cadillac

- 11.1.4 Jaguar

- 11.1.5 Lexus

- 11.1.6 Lucid

- 11.1.7 Mercedes EQ

- 11.1.8 Porsche

- 11.1.9 Rivian

- 11.1.10 Tesla

- 11.2 Regional Players

- 11.2.1 Genesis

- 11.2.2 Karma

- 11.2.3 Lotus

- 11.2.4 Maserati

- 11.2.5 Volvo

- 11.3 Emerging Players

- 11.3.1 Denza

- 11.3.2 Hongqi

- 11.3.3 Voyah

- 11.3.4 XPeng

- 11.3.5 Zeekr