PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998809

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998809

Automotive Over-The-Air (OTA) Update Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

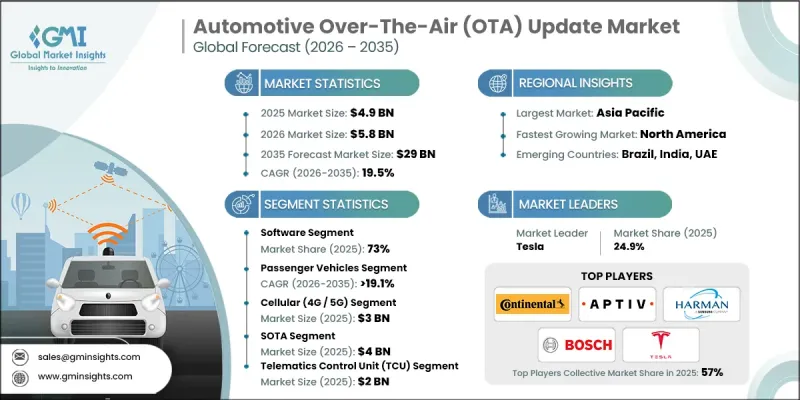

The Global Automotive Over-The-Air (OTA) Update Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 19.5% to reach USD 29 billion by 2035.

The market is experiencing rapid expansion as software-defined vehicles (SDVs), connected technologies, and electric mobility gain traction worldwide. Automakers are increasingly focusing on secure, scalable, and real-time OTA update capabilities to enhance vehicle functionality, safety, and user experience. Rising regulatory mandates related to cybersecurity, functional safety, and software compliance across North America, Europe, and Asia Pacific are pushing OEMs and technology providers to adopt advanced OTA frameworks for both passenger and commercial vehicles. The demand is further fueled by the need to minimize recall costs, accelerate feature deployment, and enhance customer satisfaction. Expanding adoption of connected EVs, commercial fleets, and telematics-driven platforms reinforces the requirement for robust firmware-over-the-air (FOTA) and software-over-the-air (SOTA) solutions, enabling continuous performance optimization and lifecycle management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $29 Billion |

| CAGR | 19.5% |

The software segment held 73% share and is expected to grow at a CAGR of 19% from 2026 to 2035. This dominance is driven by the increasing deployment of secure software and firmware management platforms, predictive diagnostics tools, and cloud-based vehicle lifecycle systems. OEMs and fleet operators rely heavily on software solutions to provide real-time updates for ECUs, infotainment systems, drive-control mechanisms, and safety-critical applications. Integration of AI, telematics, and connectivity platforms further strengthens the role of software solutions across passenger and commercial EVs, ensuring regulatory compliance, performance optimization, and cost reduction.

The passenger vehicle segment held 76% share in 2025 and is expected to grow at a CAGR of 19.1% through 2035. The widespread adoption of electric passenger vehicles and the increasing need for battery management, motor reliability, infotainment enhancements, and real-time software updates reinforce this segment's dominance. OEMs and service networks are standardizing OTA solutions for passenger EVs, ensuring warranty-compliant, data-driven updates, predictive maintenance, and performance optimization. High penetration of passenger EVs across China, Europe, and North America drives recurring OTA deployments, further solidifying market leadership in this segment.

China Automotive Over-The-Air (OTA) Update Market held a 51% share, generating USD 0.8 billion in 2025. Growth is driven by the nation's strong EV production, widespread adoption of connected and software-defined vehicles, and large-scale deployment of battery, motor, and software maintenance solutions. Collaborations between OEMs, fleet operators, and digital service providers enable efficient implementation of predictive diagnostics, software updates, and vehicle monitoring platforms, driving OTA adoption across passenger and commercial vehicles.

Major players in the Global Automotive Over-The-Air (OTA) Update Market include BYD Auto, Hyundai Motor, Tesla, BMW, HARMAN International, Qualcomm, Robert Bosch, NXP Semiconductors, Aptiv, and Continental. Companies operating in the Automotive Over-The-Air (OTA) Update Market strengthen their position by investing in scalable, secure, and AI-driven software platforms that support real-time vehicle updates. Strategic collaborations with OEMs, telematics providers, and cloud service firms enhance global reach and enable seamless integration of OTA solutions. Expanding capabilities for predictive diagnostics, battery management, and advanced driver assistance systems improves product differentiation. Firms also focus on regional expansion into high-growth EV markets, ensuring regulatory compliance and cybersecurity standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Connectivity

- 2.2.5 Technology

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Software-Defined Vehicles (SDVs)

- 3.2.1.2 Growth in Connected & Electric Vehicles

- 3.2.1.3 Need for Cost Reduction

- 3.2.1.4 Cybersecurity & Regulatory Compliance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity Risks

- 3.2.2.2 Complex ECU Integration

- 3.2.3 Market opportunities

- 3.2.3.1 5G Expansion

- 3.2.3.2 Fleet & Commercial Vehicle Digitization

- 3.2.3.3 AI-Powered Predictive Maintenance Integration

- 3.2.3.4 Feature-on-Demand & Subscription Services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: NHTSA, EPA, CARB Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS 305

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, UNECE R155/R156 Compliance

- 3.4.2.2 France: Ministry of Transport, UNECE Regulations

- 3.4.2.3 UK: Department for Transport, UNECE Compliance

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, Emission & Safety Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, Cybersecurity & OTA Standards

- 3.4.3.2 Japan: MLIT, JIS Compliance

- 3.4.3.3 South Korea: MOLIT, KS OTA Standards

- 3.4.3.4 India: MoRTH, BS6 & Cybersecurity Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport, NOM Emission Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA OTA Guidelines

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO OTA Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of Artificial Intelligence (AI)

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Update Management Platform

- 5.2.2 Security Solutions

- 5.2.3 Data Analytics & Monitoring

- 5.3 Services

- 5.3.1 Consulting & Advisory

- 5.3.2 Implementation & Integration

- 5.3.3 Testing & Validation

- 5.3.4 Managed Services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Connectivity, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Cellular (4G / 5G)

- 7.3 Wi-Fi

- 7.4 Satellite

Chapter 8 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 SOTA

- 8.2.1 Infotainment & Navigation Updates

- 8.2.2 Drive Control & Safety-Critical Updates

- 8.3 FOTA

- 8.3.1 ECU Firmware Updates

- 8.3.2 Bootloader & Low-Level System Updates

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Telematics Control Unit (TCU)

- 9.3 Electronic Control Unit (ECU)

- 9.4 Infotainment Systems

- 9.5 Safety & Security Systems

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 Aptiv

- 11.1.2 BMW

- 11.1.3 BYD Auto

- 11.1.4 Continental

- 11.1.5 HARMAN International

- 11.1.6 Hyundai Motor

- 11.1.7 NXP Semiconductors

- 11.1.8 Qualcomm

- 11.1.9 Robert Bosch

- 11.1.10 Tesla

- 11.2 Regional Player

- 11.2.1 CATL

- 11.2.2 Denso Tec

- 11.2.3 ElringKlinger

- 11.2.4 Faurecia (FORVIA)

- 11.2.5 Futaba Industrial

- 11.2.6 Gotion High-Tech

- 11.2.7 Panasonic Automotive

- 11.2.8 Tenneco

- 11.2.9 Valeo SA

- 11.2.10 ZF Friedrichshafen