PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998818

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998818

Magnetoresistive RAM (MRAM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

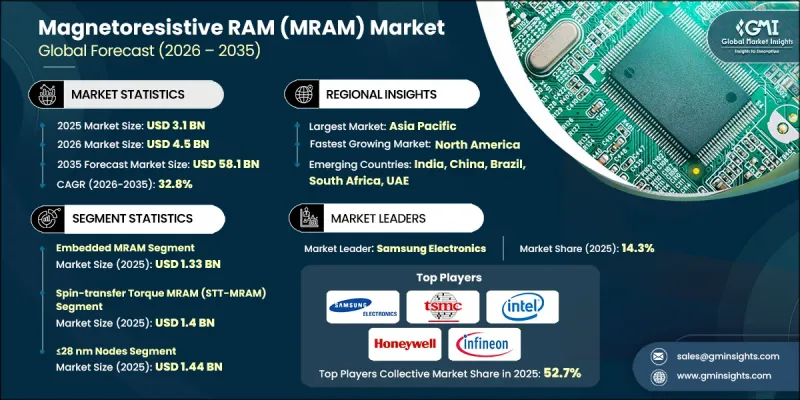

The Global Magnetoresistive RAM (MRAM) Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 32.8% to reach USD 58.1 billion by 2035.

Market growth is driven by the increasing requirement for ultra-fast memory performance, minimal latency, and non-volatile storage capabilities that significantly reduce power consumption. As digital transformation accelerates, industries are demanding advanced memory technologies that deliver both speed and energy efficiency. MRAM is gaining strong adoption due to its scalability and compatibility with advanced semiconductor process nodes, making it suitable for next-generation chip architectures. The growing integration of connected systems, smart electronics, and data-intensive applications is further strengthening demand for embedded memory solutions. MRAM's ability to retain data without power while maintaining high endurance positions it as a reliable alternative to traditional memory technologies. Expanding implementation across automotive electronics and IoT ecosystems is reinforcing long-term revenue opportunities. As semiconductor manufacturers continue innovating toward compact, efficient, and high-performance systems, the magnetoresistive RAM market is set for exponential expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $58.1 Billion |

| CAGR | 32.8% |

The combination of durability, non-volatility, and energy efficiency is accelerating MRAM adoption across automotive and IoT environments. Connected systems require memory that ensures data integrity while operating under demanding conditions. MRAM provides instant-on functionality and robust performance, making it highly suitable for intelligent vehicle platforms and distributed device networks that require real-time processing and dependable long-term storage. In IoT endpoints, non-volatile memory plays a vital role in preserving data and reducing energy usage during power interruptions. The rapid expansion of smart devices that rely on embedded architectures is significantly boosting demand for embedded MRAM. Integrated non-volatile memory enables system-on-chips and microcontrollers to manage storage internally, reducing hardware complexity and improving energy optimization.

The embedded MRAM segment reached USD 1.33 billion in 2025. This segment supports seamless integration into SoCs and microcontrollers, minimizing board footprint while improving system stability and efficiency. Its low-latency performance and non-volatile characteristics enable rapid boot cycles, real-time data processing, and secure firmware storage across high-density computing environments. Manufacturers are prioritizing embedded MRAM solutions tailored for automotive, industrial, and consumer semiconductor platforms, with emphasis on low power consumption, high endurance, and reliable instant-on capabilities for mission-critical applications.

The spin-transfer torque MRAM (STT-MRAM) segment generated USD 1.4 billion in 2025. STT-MRAM delivers high-speed read and write performance while maintaining reduced energy consumption, making it a strong fit for embedded systems, automotive electronics, and industrial-grade semiconductor devices. Industry participants are focusing on refining fabrication processes for STT-MRAM to optimize integration within embedded SoCs and automotive-grade chips. Leveraging its performance advantages allows manufacturers to expand their footprint in connected systems and high-reliability electronic applications.

North America Magnetoresistive RAM (MRAM) Market held 28.5% share in 2025, positioning the region as a key growth hub. A well-established semiconductor ecosystem, substantial research investments, and early integration of MRAM into advanced computing and storage systems support regional dominance. Semiconductor foundries and chip designers across the region are incorporating MRAM into next-generation processors to meet rising requirements for efficiency, durability, and performance in AI-driven and edge computing platforms. Government-backed semiconductor initiatives are strengthening domestic manufacturing capacity and encouraging innovation in memory technologies, enhancing overall supply chain resilience.

Leading companies operating in the Global Magnetoresistive RAM (MRAM) Market include Samsung Electronics, Everspin Technologies, Intel, Avalanche Technology, SK Hynix, TSMC, Honeywell International, Fujitsu, Infineon Technologies, Crocus Technology, Toshiba, NVE Corporation, Numem, and Spin Memory. Companies in the magnetoresistive RAM market are strengthening their competitive position through continuous innovation, fabrication optimization, and strategic collaborations. Major players are investing heavily in research and development to enhance the scalability, endurance, and integration of MRAM within advanced semiconductor nodes. Partnerships with automotive and industrial chip manufacturers are expanding commercial deployment opportunities. Capacity expansion and process refinement are improving production efficiency and yield rates. Firms are also targeting embedded memory applications to capture demand from IoT and AI-driven systems. Geographic expansion into high-growth semiconductor regions is further supporting revenue diversification.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Device type trends

- 2.2.2 Offering trends

- 2.2.3 Technology node trends

- 2.2.4 Memory density trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for high-speed performance and low latency

- 3.2.1.2 Non-volatility reducing power consumption

- 3.2.1.3 Increasing adoption in automotive and IoT applications

- 3.2.1.4 Rising demand for embedded memory solutions

- 3.2.1.5 Scalability and compatibility with advanced process nodes

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High manufacturing costs compared to traditional memory

- 3.2.2.2 Technological complexity and integration challenges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Device Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Spin-Transfer Torque MRAM (STT-MRAM)

- 5.3 Voltage-Controlled MRAM (VC-MRAM)

- 5.4 Toggle MRAM

- 5.5 Spin-Orbit Torque MRAM (SOT-MRAM)

Chapter 6 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Embedded MRAM

- 6.3 Stand-Alone MRAM

- 6.4 IP Cores & Design Services

Chapter 7 Market Estimates and Forecast, By Technology Node, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 ≤ 28 nm

- 7.3 28-40 nm

- 7.4 40-65 nm

- 7.5 > 65 nm

Chapter 8 Market Estimates and Forecast, By Memory Density, 2022 - 2035 (USD Million)

- 8.1 Key Trends

- 8.2 < 256 Kbit

- 8.3 256 Kbit-1 Mbit

- 8.4 1-16 Mbit

- 8.5 > 16 Mbit

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key Trends

- 9.2 Automotive Electronics

- 9.3 IoT & Edge Computing Devices

- 9.4 Consumer Electronics

- 9.5 Enterprise Storage & Data Centers

- 9.6 Industrial Automation & Robotics

- 9.7 Aerospace & Defense

- 9.8 Healthcare Devices

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Samsung Electronics

- 11.1.2 TSMC

- 11.1.3 Intel

- 11.1.4 SK Hynix

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Everspin Technologies

- 11.2.1.2 Honeywell International

- 11.2.1.3 NVE Corporation

- 11.2.2 Europe

- 11.2.2.1 Infineon Technologies

- 11.2.2.2 Crocus Technology

- 11.2.3 Asia Pacific

- 11.2.3.1 Toshiba

- 11.2.3.2 Fujitsu

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 Avalanche Technology

- 11.3.2 Spin Memory

- 11.3.3 Numem