PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998823

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998823

Firefighting Aircraft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

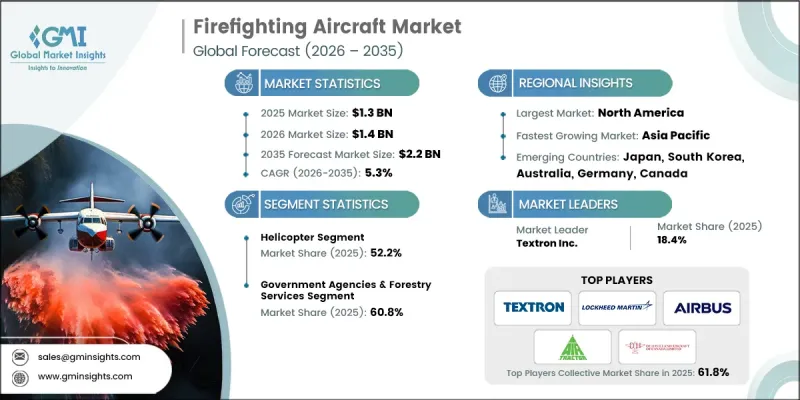

The Global Firefighting Aircraft Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 2.2 billion by 2035.

Growth in the firefighting aircraft market is supported by the increasing need for rapid-response aerial firefighting capabilities across regions that regularly experience severe wildfire activity. Governments and emergency management authorities are expanding aerial firefighting resources to strengthen disaster response strategies and reduce damage caused by large-scale fires. In addition, the modernization of aerial firefighting fleets is becoming a key priority as older aircraft gradually reach the end of their operational lifespan. Investment in advanced aircraft platforms capable of carrying larger suppressant loads and operating in complex fire environments is increasing across several countries. The integration of advanced surveillance technologies, mission coordination tools, and aerial command systems is also improving firefighting efficiency and response times. These technological improvements allow firefighting agencies to monitor fire behavior more effectively while deploying aerial resources with greater precision. Collectively, these factors are contributing to the long-term expansion of the global firefighting aircraft market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.3% |

The firefighting aircraft market continues to gain momentum as wildfire events become more frequent and severe across several regions of the world. Rising fire intensity is placing greater operational pressure on firefighting agencies, which increasingly rely on aerial suppression capabilities to contain large fires quickly. At the same time, many existing firefighting aircraft fleets are aging, prompting governments and operators to invest in replacement programs and modernized platforms. As older aircraft approach retirement, agencies are focusing on acquiring newer models that offer improved payload capacity, enhanced safety systems, and greater operational efficiency. Additionally, wildfire seasons are extending in duration, which increases aircraft utilization rates and requires greater fleet availability during peak response periods.

The helicopter segment accounted for 52.2% share in 2025. Helicopters remain widely utilized in aerial firefighting operations due to their ability to perform highly flexible missions in complex environments. These aircraft are particularly valuable in areas where terrain conditions limit the effectiveness of other aerial platforms. Their maneuverability allows them to operate in confined spaces and deliver targeted water or retardant drops with high precision. Helicopters can also access nearby water sources quickly, allowing them to refill and redeploy multiple times during a firefighting mission. Because of their operational versatility and rapid deployment capability, helicopters continue to play a central role in wildfire suppression strategies across many regions affected by recurring fire activity.

The 5,000-10,000 liters segment is anticipated to grow at a CAGR of 6.2% during 2026-2035, reflecting increasing demand for mid-capacity aerial firefighting platforms. Aircraft within this payload range offer a balanced combination of operational efficiency and mission flexibility. These platforms can deliver substantial volumes of fire suppressant while maintaining the ability to operate from a broader range of airfields. Their versatility allows them to support various firefighting operations, including regional wildfire response and coordinated aerial suppression missions. In addition, mid-sized firefighting aircraft typically involve lower acquisition and operational costs compared with larger tanker aircraft, making them attractive options for countries seeking to expand their aerial firefighting fleets without significantly increasing capital expenditure.

North America Firefighting Aircraft Market accounted for 33.8% share in 2025. The market in this region continues to expand due to increasing wildfire activity and the growing need for effective aerial firefighting capabilities. Fire management agencies across the region are investing in advanced aerial suppression resources to strengthen rapid response capacity and reduce the impact of large-scale fires. Government organizations and aviation service providers are also expanding multi-year aircraft contracts and cooperative resource-sharing arrangements to ensure sufficient firefighting capacity during peak fire seasons. At the same time, investments in advanced avionics systems, improved retardant delivery technologies, and real-time mission coordination platforms are helping operators enhance operational performance and aircraft availability across North America.

Key companies operating in the Global Firefighting Aircraft Market include Airbus SE, Lockheed Martin Corporation, Textron Inc., Saab AB, Embraer S.A., United Aircraft Corporation, De Havilland Aircraft of Canada Limited, ShinMaywa Industries, Ltd., Air Tractor, Inc., Thrush Aircraft, Coulson Aviation, Conair Group Inc., Erickson Incorporated, Kaman Corporation, and Russian Helicopters JSC. Companies active in the Global Firefighting Aircraft Market are adopting several strategic initiatives to strengthen their competitive position and expand their operational capabilities. Many organizations are focusing on developing advanced aerial firefighting platforms with improved payload capacity, enhanced safety features, and greater operational efficiency. Investment in research and development is enabling manufacturers to integrate advanced avionics, mission management systems, and improved suppressant delivery technologies into modern aircraft designs. Strategic partnerships with government agencies and firefighting operators are also helping companies secure long-term contracts and strengthen their market presence. In addition, firms are expanding maintenance, repair, and support services to ensure reliable aircraft performance during demanding firefighting missions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Aircraft trends

- 2.2.2 Water capacity trends

- 2.2.3 End-user trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising megafire frequency in North America and Australia

- 3.2.1.2 Aging global aerial firefighting fleets requiring replacement

- 3.2.1.3 Government funding increases for wildfire suppression

- 3.2.1.4 Expansion of wildland urban interface zones

- 3.2.1.5 Climate-driven longer fire seasons globally

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High acquisition and lifecycle maintenance costs

- 3.2.2.2 Limited production capacity for specialized aircraft

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation amphibious and scooper aircraft development

- 3.2.3.2 Retrofit programs for turboprop conversion platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Aircraft, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Helicopter

- 5.2.1 Type 1

- 5.2.2 Type 2

- 5.2.3 Type 3

- 5.3 Fixed wing aircraft

- 5.4 Unmanned aerial vehicles

Chapter 6 Market Estimates and Forecast, By Water Capacity, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Less than 5,000 liters

- 6.3 5,000-10,000 liters

- 6.4 More than 10,000 liters

Chapter 7 Market Estimates and Forecast, By End-user, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Government agencies & forestry services

- 7.3 Military operators

- 7.4 Private contractors

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Airbus SE

- 9.1.2 Lockheed Martin Corporation

- 9.1.3 Textron Inc.

- 9.1.4 Embraer S.A.

- 9.1.5 United Aircraft Corporation

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Air Tractor, Inc.

- 9.2.1.2 Erickson Incorporated

- 9.2.1.3 Kaman Corporation

- 9.2.1.4 Conair Group Inc.

- 9.2.1.5 Coulson Aviation

- 9.2.2 Asia Pacific

- 9.2.2.1 ShinMaywa Industries, Ltd.

- 9.2.2.2 Russian Helicopters JSC

- 9.2.3 Europe

- 9.2.3.1 Saab AB

- 9.2.3.2 De Havilland Aircraft of Canada Limited

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Thrush Aircraft