PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998828

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998828

Automotive Crash Test Dummies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

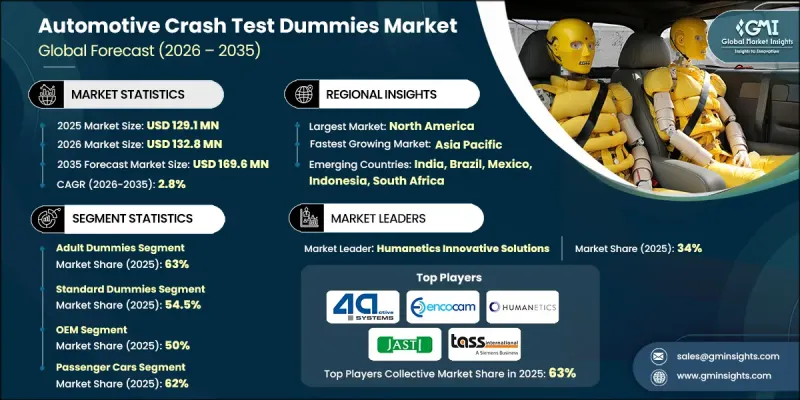

The Global Automotive Crash Test Dummies Market was valued at USD 129.1 million in 2025 and is estimated to grow at a CAGR of 2.8% to reach USD 169.6 million by 2035.

Growth in the automotive crash test dummies market is closely linked to the continued expansion of global vehicle manufacturing, which increases the need for safety validation and compliance testing across new vehicle models. As automakers introduce updated vehicle designs and integrate new safety technologies, the requirement for detailed crash simulations and safety performance assessments continues to rise. Regulatory bodies across several regions have also strengthened vehicle safety standards, encouraging manufacturers to perform extensive crash testing to ensure compliance with evolving guidelines. The increasing emphasis on occupant protection and vehicle safety innovation is reinforcing the importance of crash test dummies in automotive research and development programs. In addition, improvements in biomechanical modeling and measurement capabilities are enabling engineers to capture more accurate data related to human injury risk during crash scenarios. These developments continue to support the long-term demand for advanced crash testing tools, positioning the automotive crash test dummies market as a critical component within the broader automotive safety ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $129.1 Million |

| Forecast Value | $169.6 Million |

| CAGR | 2.8% |

The automotive industry has placed greater attention on improving protection for occupants with varying physical characteristics, which has increased demand for specialized crash test dummies designed to represent different body structures. Modern dummy systems are becoming significantly more advanced, offering improved bio-fidelity that enables engineers to collect highly precise data regarding potential injuries during simulated collisions. The integration of enhanced sensor technologies has allowed crash test dummies to record a wider range of measurements related to force, motion, and impact response during testing procedures. As crash simulations become more complex, these advanced dummies help engineers better understand vehicle safety performance and refine safety designs accordingly.

The adult crash test dummies segment held 63% share and is expected to grow at a CAGR of 1.6% between 2026 and 2035. Adult dummies are widely used in vehicle crash simulations to evaluate occupant safety across multiple collision scenarios involving the front, side, and rear of a vehicle. These dummies are designed to replicate the physical characteristics of typical adult body structures and are equipped with measurement systems that track potential injuries across several critical areas of the body. Data collected from these simulations plays an essential role in establishing global vehicle safety benchmarks and guiding the development of improved safety systems. Because adult body structures represent a significant portion of real-world vehicle occupants, these dummies remain fundamental to automotive safety testing programs worldwide.

The standard dummies segment accounted for 54.5% share in 2025 and is anticipated to grow at a CAGR of 1.7% from 2026 to 2035. Standard crash test dummies are designed as general-purpose models used primarily in regulatory compliance testing and baseline vehicle safety evaluations. These models typically feature simplified mechanical structures that replicate human body movement during collision events. Although they incorporate limited electronic instrumentation compared to advanced models, they continue to play a crucial role in many testing programs due to their accessibility and cost efficiency. Automotive manufacturers frequently utilize standard dummies for routine safety validation procedures and laboratory testing activities where extremely detailed data collection is not required.

United States Automotive Crash Test Dummies Market reached USD 38.7 million in 2025, supported by strict vehicle safety regulations and ongoing advancements in automotive testing standards. Federal safety guidelines require manufacturers to conduct comprehensive crash evaluations as part of vehicle certification processes, which continues to drive demand for standardized crash test equipment. Automotive manufacturers and independent testing organizations in the United States regularly perform detailed crash simulations to ensure that vehicles meet established safety benchmarks. As safety evaluation programs evolve and testing protocols become more sophisticated, research laboratories are gradually upgrading their facilities to accommodate newer crash test dummy technologies.

Key companies operating in the Global Automotive Crash Test Dummies Market include Humanetics Innovative Solutions, Kistler, Cellbond (Encocam), MGA Research, Dynamic Research, CTS, 4activeSystems, JASTI, and TASS (Siemens). Companies active in the Global Automotive Crash Test Dummies Market are focusing on multiple strategic initiatives to strengthen their competitive position and expand their technological capabilities. Significant investments are being directed toward research and development to improve dummy biofidelity and enhance the accuracy of injury measurement systems. Manufacturers are also incorporating advanced sensor technologies and data acquisition systems to provide more detailed insights into crash dynamics. Strategic collaborations with automotive manufacturers, safety laboratories, and regulatory institutions are helping companies develop testing solutions aligned with evolving safety standards. Expanding product portfolios to include next-generation dummy platforms designed for complex crash simulations is another key strategy.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Dummy

- 2.2.3 Technology

- 2.2.4 Vehicle

- 2.2.5 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent vehicle safety regulations

- 3.2.1.2 Rising vehicle production globally

- 3.2.1.3 Increasing focus on child & pedestrian safety

- 3.2.1.4 Growing adoption of advanced dummies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced crash test dummies

- 3.2.2.2 Long replacement & calibration cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging market safety regulation expansion

- 3.2.3.2 Development of female and elderly representative dummies

- 3.2.3.3 Growth in electric & autonomous vehicle testing

- 3.2.3.4 Advancements in smart data acquisition systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Insurance Institute for Highway Safety (IIHS)

- 3.4.2 Europe

- 3.4.2.1 Euro NCAP (European New Car Assessment Programme)

- 3.4.2.2 UNECE Regulations (R94, R95, R129)

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Automobile Research Institute (JARI) / JIS Standards

- 3.4.3.2 China Automotive Technology & Research Center (CATARC) / Chinese NCAP (C-NCAP)

- 3.4.4 Latin America

- 3.4.4.1 Latin NCAP

- 3.4.4.2 ABNT NBR / National Automotive Safety Guidelines

- 3.4.5 Middle East & Africa

- 3.4.5.1 ESMA Vehicle Safety Standards (UAE)

- 3.4.5.2 SABS Automotive Safety Standards (South Africa)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by primary research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by primary research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by primary research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Trade data analysis (Driven by paid database)

- 3.14.1 Import/export volume & value trends

- 3.14.2 Key trade corridors & tariff impact

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Dummy, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Adult dummies

- 5.2.1 Male adult dummies

- 5.2.2 Female adult dummies

- 5.3 Child dummies

- 5.3.1 0-year-old child dummies

- 5.3.2 6-year-old child dummies

- 5.3.3 3-year-old child dummies

- 5.4 Infant dummies

- 5.4.1 8-month infant dummies

- 5.4.2 2-month infant dummies

- 5.4.3 newborn dummies

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Standard dummies

- 6.3 Advanced / sensor-equipped dummies

- 6.4 Hybrid dummies

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Passenger car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Original Equipment Manufacturers (OEMs)

- 8.3 Automotive suppliers & testing labs

- 8.4 Government / regulatory bodies

- 8.5 Independent safety organizations / research institutions

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 4activeSystems

- 10.1.2 Autoliv

- 10.1.3 Cellbond

- 10.1.4 CTS

- 10.1.5 HORIBA MIRA

- 10.1.6 Humanetics Innovative Solutions

- 10.1.7 JASTI

- 10.1.8 Kistler

- 10.1.9 MGA Research

- 10.1.10 TASS International

- 10.2 Regional players

- 10.2.1 Calspan

- 10.2.2 Crashtest-Service.com

- 10.2.3 DEKRA

- 10.2.4 Denton

- 10.2.5 Diversified Technical Systems (DTS)

- 10.2.6 Dynamic Research

- 10.2.7 Transportation Research Center (TRC)

- 10.3 Emerging players

- 10.3.1 AB Dynamics

- 10.3.2 FUTEK Advanced Sensor Technology

- 10.3.3 Hunan Safe Automobile Technology