PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998847

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998847

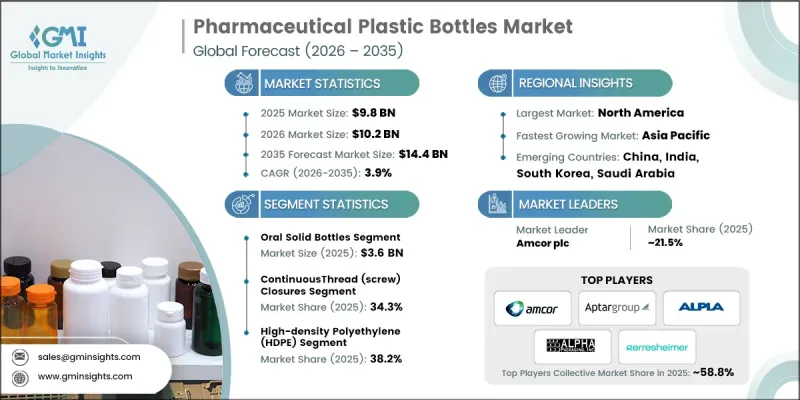

Pharmaceutical Plastic Bottles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Pharmaceutical Plastic Bottles Market was valued at USD 9.8 billion in 2025 and is estimated to grow at a CAGR of 3.9% to reach USD 14.4 billion in 2035.

The market is expanding due to rising global production of generic drugs, continuous growth of oral solid dosage forms, and increasing consumption of over-the-counter (OTC) medicines. The ongoing transition from glass to lightweight high-density polyethylene (HDPE) packaging, coupled with rising outsourcing to contract manufacturing organizations (CMOs), is also driving demand. Regulatory mandates for child-resistant and tamper-evident packaging, along with sustainability initiatives promoting recyclable and PCR-based bottles, are further stimulating growth. North America and Asia-Pacific are experiencing heightened OTC demand driven by self-medication trends, pharmacy network expansion, and growth in the nutraceutical segment. The use of plastic bottles provides key advantages, including safety, tamper evidence, and lightweight design, which continues to support high turnover and consistent demand in retail and pharmacy channels worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.8 Billion |

| Forecast Value | $14.4 Billion |

| CAGR | 3.9% |

The oral solid bottles segment reached USD 3.6 billion in 2025. These bottles remain critical as tablets and capsules account for the highest prescription volumes globally, particularly for chronic conditions. They offer moisture protection, bulk packaging efficiency, and compatibility with child-resistant closures, making them essential for large-scale pharmaceutical production and distribution networks.

The high-density polyethylene (HDPE) segment accounted for 38.2% share in 2025. HDPE is preferred for its excellent moisture barrier properties, chemical resistance, durability, and lightweight nature, making it highly suitable for packaging tablets, capsules, and powders. Its cost-effective transport and compliance with pharmaceutical stability requirements make it the material of choice in regulated markets across North America, Europe, and Asia.

North America Pharmaceutical Plastic Bottles Market held 39.7% share in 2025. Growth in this region is supported by rising prescription drug consumption, stricter drug safety regulations, and the shift to lightweight, shatter-resistant packaging. Regulatory oversight from the FDA and Health Canada requires adherence to child-resistant and tamper-evident standards, which drives demand for HDPE and polypropylene pharmaceutical bottles.

Prominent players in the Global Pharmaceutical Plastic Bottles Market include ALPLA Group, Amcor plc, Alpha Packaging, Inc., AptarGroup, Inc., COMAR LLC, Drug Plastics & Glass Company, Inc., C.L. Smith Company, Frapak Packaging B.V., Gerresheimer AG, Gil Plastic Products Ltd, Mykron Plus India Pvt. Ltd., O.Berk Company LLC, Origin Pharma Packaging Ltd, Plastipak Holdings, Inc., Pretium Packaging, LLC, Pro-Pac Packaging Ltd, Silgan Holdings Inc., United States Plastic Corporation, Weener Plastics Group BV, and Zhejiang B.I. Industrial Co., Ltd. Companies in the Global Pharmaceutical Plastic Bottles Market are employing multiple strategies to strengthen their foothold and expand their global presence. These include investing in R&D to develop child-resistant, tamper-evident, and PCR-based packaging solutions that align with sustainability trends. Firms are forming strategic alliances with CMOs and pharmaceutical companies to secure long-term contracts and increase production capacity. Expansion of regional manufacturing facilities ensures faster delivery and cost optimization. Companies are also implementing advanced quality control systems and regulatory compliance protocols to meet international standards, enhancing brand reliability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Bottle type trends

- 2.2.2 Material type trends

- 2.2.3 Bottle capacity trends

- 2.2.4 Closure type trends

- 2.2.5 End-user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global generic drug production volumes

- 3.2.1.2 Growth in oral solid dosage consumption

- 3.2.1.3 Increasing OTC medicine demand globally

- 3.2.1.4 Shift from glass to lightweight HDPE bottles

- 3.2.1.5 Expansion of contract manufacturing organizations (CMOs)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile resin prices (HDPE, PET, PP)

- 3.2.2.2 Stringent extractables and leachables compliance

- 3.2.3 Market opportunities

- 3.2.3.1 Bio-based polymer adoption in pharma packaging

- 3.2.3.2 Smart packaging with anti-counterfeit features

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Bottle Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Oral solid bottles

- 5.3 Oral liquid bottles

- 5.4 Ophthalmic bottles

- 5.5 Parenteral/injectable vials

- 5.6 Nasal spray bottles

- 5.7 Topical/dermal bottles

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 High-density polyethylene (HDPE)

- 6.3 Low-density polyethylene (LDPE)

- 6.4 Polypropylene (PP)

- 6.5 Polyethylene terephthalate (PET)

- 6.6 Polyethylene terephthalate glycol (PETG)

- 6.7 Cyclic olefin polymer (COP) & cyclic olefin copolymer (COC)

Chapter 7 Market Estimates and Forecast, By Bottle Capacity, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Micro bottles (5ml - 20ml)

- 7.3 Small bottles (30ml - 100ml)

- 7.4 Medium bottles (120ml - 300ml)

- 7.5 Large bottles (500ml - 1000ml)

- 7.6 Extra-large bottles (>1000ml)

Chapter 8 Market Estimates and Forecast, By Closure Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Continuous thread (screw) closures

- 8.3 Snap-on closures

- 8.4 Dispensing closures

- 8.5 Specialty closures

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Pharmaceutical manufacturers (in-house production)

- 9.3 Contract manufacturing organizations (CMO/CDMO)

- 9.4 Nutraceutical & dietary supplement manufacturers

- 9.5 Healthcare institutions

- 9.6 Compounding pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Gerresheimer AG

- 11.1.2 Amcor plc

- 11.1.3 AptarGroup, Inc.

- 11.1.4 ALPLA Group

- 11.1.5 Silgan Holdings Inc.

- 11.1.6 Plastipak Holdings, Inc.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Alpha Packaging, Inc.

- 11.2.1.2 COMAR LLC

- 11.2.1.3 Drug Plastics & Glass Company, Inc.

- 11.2.1.4 Pretium Packaging, LLC

- 11.2.1.5 C.L. Smith Company

- 11.2.1.6 O.Berk Company LLC

- 11.2.1.7 United States Plastic Corporation

- 11.2.2 Asia Pacific

- 11.2.2.1 Mykron Plus India Pvt. Ltd.

- 11.2.2.2 Zhejiang B.I. Industrial Co., Ltd.

- 11.2.2.3 Pro-Pac Packaging Ltd

- 11.2.3 Europe

- 11.2.3.1 Frapak Packaging B.V.

- 11.2.3.2 Origin Pharma Packaging Ltd

- 11.2.3.3 Weener Plastics Group BV

- 11.2.3.4 Gil Plastic Products Ltd

- 11.2.1 North America