PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998856

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998856

Healthcare Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

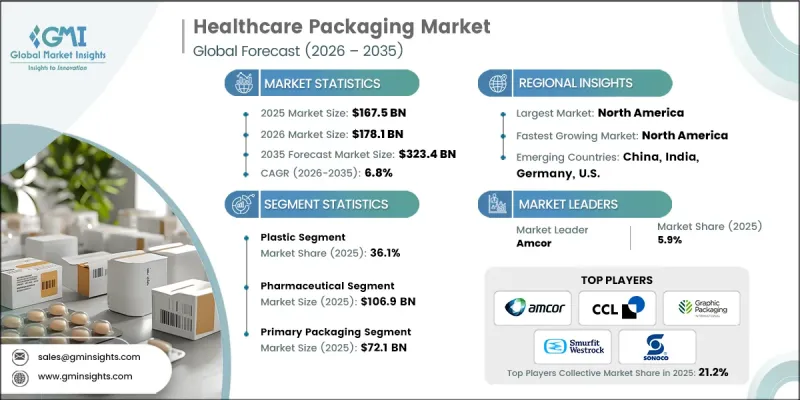

The Global Healthcare Packaging Market was valued at USD 167.5 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 323.4 billion by 2035.

The expansion of the global pharmaceutical and biotechnology sectors is driving the demand for advanced healthcare packaging that ensures product safety, sterility, and tamper evidence. The growing adoption of biologics, specialty drugs, and personalized medicine has created a need for innovative materials and designs that enhance product integrity, extend shelf life, and support complex drug delivery systems. Tighter regulatory requirements and heightened emphasis on patient safety are accelerating the adoption of compliant packaging solutions. Serialization, anti-counterfeiting measures, and tamper-evident designs are becoming standard across the industry. Rising demand for vaccines, temperature-sensitive medications, and biologics is also increasing the need for cold chain and insulated packaging solutions, compelling manufacturers to develop materials that meet strict thermal stability requirements while ensuring supply chain security and traceability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $167.5 Billion |

| Forecast Value | $323.4 Billion |

| CAGR | 6.8% |

The plastic segment held a 36.1% share in 2025, driven by its lightweight, cost-effective, and versatile properties. Plastic packaging offers durability, break resistance, and adaptability for tamper-proof, child-resistant, and pre-filled designs. Its compatibility with a wide range of pharmaceutical and biologic products makes it the preferred choice for hospitals, pharmacies, and home healthcare applications. Manufacturers continue to innovate plastic packaging to maintain compliance, reduce environmental impact, and meet the evolving demands of healthcare providers.

The pharmaceutical application segment reached USD 106.9 billion in 2025, due to the global increase in pharmaceutical consumption, high-volume prescriptions, and growing biologics production. Rising regulatory compliance requirements have prompted pharmaceutical companies to invest in safe, secure, and child-resistant packaging solutions. Hospitals, pharmacies, and home healthcare markets are driving continued demand for packaging that meets both safety and operational efficiency needs while protecting product quality.

North America Healthcare Packaging Market accounted for 38.5% share in 2025. The region's growth is fueled by increasing demand for sterile, child-resistant, and tamper-proof packaging, coupled with the expansion of biologics, biosimilars, and home healthcare services. Stringent regulations and the adoption of advanced labeling, serialization, and sustainable packaging solutions are further supporting market growth. Manufacturers in the region are focusing on developing innovative and compliant packaging systems that meet strict safety standards and regulatory requirements while also addressing environmental concerns.

Key players operating in the Global Healthcare Packaging Market include Amcor, Aptar CSP Technologies, August Faller GmbH & Co. KG, CCL Industries, Cold Chain Technologies LLC, Constantia Flexibles, Cryopak Industries Inc, Gerresheimer, Graphic Packaging, Korber AG, Mayr-Melnhof Karton, Nelipak, Peli BioThermal LLC, Schott Pharma, Schreiner Group, Smurfit WestRock, Sofrigam SA, and Sonoco Products Company. Key strategies employed by companies in the healthcare packaging market include investing in research and development to create innovative materials and packaging designs that meet regulatory compliance and enhance product protection. Firms are focusing on developing eco-friendly and sustainable solutions to align with global environmental initiatives. Strategic partnerships with pharmaceutical companies, cold chain providers, and logistics firms are being leveraged to expand distribution networks and improve supply chain efficiency. Companies are also adopting serialization, tamper-evident technologies, and anti-counterfeiting measures to strengthen brand trust and ensure compliance with international regulations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Innovation in recyclable and sustainable medical packaging

- 3.2.1.2 Expanding home healthcare and self-administration trends

- 3.2.1.3 Rising awareness about patient safety and compliance packaging

- 3.2.1.4 Growth in biologics and biosimilars requiring advanced packaging solutions

- 3.2.1.5 Rising prevalence of chronic diseases boosting demand for specialized packaging solutions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Challenges in developing packaging for emerging biologic therapies

- 3.2.2.2 Regional disparities in healthcare packaging regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Biologics and Biosimilars

- 3.2.3.2 Growth in Home Healthcare and Self-Administration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Discrete Healthcare Packaging devices

- 5.2.1 Plastic

- 5.2.2 Polyethylene Terephthalate (PET)

- 5.2.3 Polyethylene (PE)

- 5.2.4 Polypropylene (PP)

- 5.2.5 Polyvinyl Chloride (PVC)

- 5.3 Glass

- 5.4 Paper & Paperboard

- 5.5 Metals

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Primary Packaging

- 6.2.1 Bottles & Jars

- 6.2.2 Vials & Ampoules

- 6.2.3 Blister Packs

- 6.2.4 Pre-filled Syringes

- 6.2.5 Pouches

- 6.2.6 Tubes

- 6.2.7 Others

- 6.3 Secondary Packaging

- 6.3.1 Cartons & Boxes

- 6.3.2 Labels & Inserts

- 6.3.3 Trays & Sleeves

- 6.3.4 Overwraps & Shrink Wraps

- 6.3.5 Others

- 6.4 Tertiary Packaging

- 6.4.1 Shipping containers

- 6.4.2 Pallets

- 6.4.3 Protective packaging

- 6.4.4 Bulk container

- 6.4.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Pharmaceuticals

- 7.2.1 Oral Drug

- 7.2.2 Injectable

- 7.2.3 Topical & Dermal Drug

- 7.2.4 Pulmonary Drug

- 7.2.5 Nasal Drugs

- 7.2.6 Others

- 7.3 Medical Device

- 7.3.1 Disposable Consumables

- 7.3.2 Therapeutic Equipment

- 7.3.3 Monitoring & Diagnostic Equipment

- 7.3.4 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Netherlands

- 8.3.8 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia-Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Amcor

- 9.1.2 Aptar CSP Technologies

- 9.1.3 CCL Industries

- 9.1.4 Constantia Flexibles

- 9.1.5 Gerresheimer

- 9.1.6 Graphic Packaging

- 9.1.7 Mayr-Melnhof Karton

- 9.1.8 Schott Pharma

- 9.1.9 Sonoco Products Company

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Cold Chain Technologies, LLC

- 9.2.1.2 Nelipak

- 9.2.1.3 Peli BioThermal LLC

- 9.2.1.4 Smurfit WestRock

- 9.2.2 Europe

- 9.2.2.1 Sofrigam SA

- 9.2.2.2 Korber AG

- 9.2.2.3 August Faller GmbH & Co. KG

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Schreiner Group

- 9.3.2 Cryopak Industries Inc.