PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998857

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998857

Electric Golf Cart Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

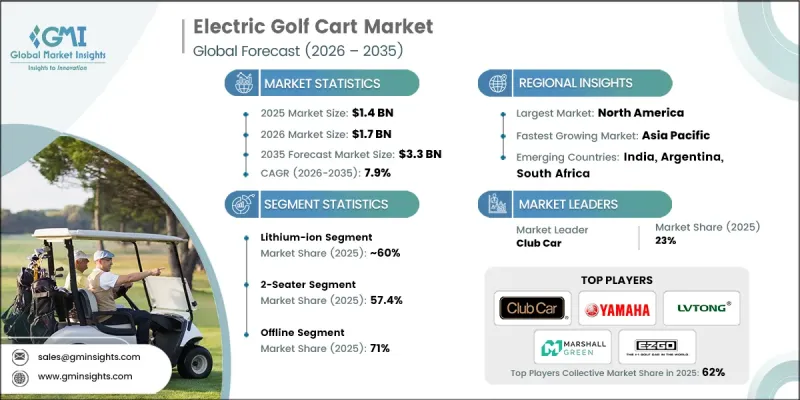

The Global Electric Golf Cart Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 3.3 billion by 2035.

The growing versatility of electric golf carts is encouraging their deployment across a wide range of environments that require efficient short-distance transportation. These vehicles provide an effective mobility solution for controlled spaces where compact design, quiet operation, and energy efficiency are important. Their low operating expenses, zero tailpipe emissions, and ease of maneuverability make them particularly suitable for environments where conventional vehicles are impractical. As organizations and institutions increasingly prioritize sustainable transportation options, electric golf carts are becoming an attractive alternative for internal mobility. Businesses, residential developments, and commercial facilities are recognizing the benefits of adopting these vehicles to improve operational efficiency while reducing environmental impact. The rising emphasis on clean mobility technologies and the need for efficient short-range transportation systems are therefore supporting the long-term expansion of the global electric golf cart market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 7.9% |

Market participants in the electric golf cart industry are actively pursuing a range of strategic initiatives to maintain competitiveness and expand their product offerings. Companies are focusing on inorganic growth strategies, including new product introductions, strategic collaborations, and acquisitions, to strengthen their market positions. Technological advancements are also reshaping the industry, particularly the gradual transition from conventional lead-acid batteries toward lithium-ion battery systems. Lithium-based batteries provide several operational advantages, including higher charging efficiency, longer service life, reduced vehicle weight, and minimal maintenance requirements. These improvements significantly enhance the operational performance and overall lifecycle economics of electric golf carts. Reduced downtime and lower maintenance costs are particularly valuable for fleet operators, which is encouraging the adoption of advanced models across commercial and institutional applications. Additionally, growing sustainability commitments and carbon-reduction initiatives are motivating organizations in the hospitality, recreational, and commercial sectors to integrate electric mobility solutions such as golf carts into their transportation infrastructure.

The 2-seater segment accounted for 57.4% share and is expected to grow at a CAGR of 8% from 2026 to 2035. Rising demand for compact personal transportation within residential developments is contributing significantly to the popularity of two-passenger models. These vehicles are particularly suitable for short-distance travel due to their compact size, ease of operation, and minimal parking requirements. They are frequently used for daily neighborhood mobility, recreational drives, and short errands, offering a convenient and efficient transportation option for residents. In addition, traditional golf facilities continue to generate consistent replacement demand for two-seater carts because this configuration remains the standard for most golf course fleets. The combination of practicality, affordability, and ease of use continues to support the widespread adoption of two-seater electric golf carts across both recreational and residential applications.

The offline distribution channel held a 71% share in 2025. Physical retail and dealership networks continue to play a vital role in facilitating customer purchases. Buyers often prefer visiting showrooms where they can directly evaluate vehicle build quality, seating comfort, battery configuration, and customization options before making purchasing decisions. Established dealer networks also help strengthen customer confidence by providing professional guidance, product demonstrations, and reliable after-sales service support. For commercial buyers and institutional customers, offline purchasing channels offer additional benefits such as direct negotiations, customized fleet configurations, and bundled service agreements. Large fleet purchasers often rely on dealership relationships to secure maintenance contracts, financing arrangements, and tailored mobility solutions that align with operational requirements, reinforcing the continued importance of traditional distribution channels in the electric golf cart market.

United States Electric Golf Cart Market accounted for 87% share, generating USD 851.7 million in 2025. The country benefits from a deeply established golf culture supported by many operational golf facilities across various regions. Continuous participation in recreational and competitive golf activities maintains a strong demand for fleet vehicles within these facilities. Regular fleet replacement cycles and the ongoing transition toward lithium-powered vehicles provide stability in procurement across the sector. In addition to recreational use, residential communities designed with internal mobility systems are also contributing significantly to the adoption of electric golf carts. Many planned communities permit the use of low-speed vehicles within their internal transportation networks, encouraging households to purchase personal carts for everyday mobility within neighborhood environments.

Major companies operating in the Global Electric Golf Cart Market include Club Car, Dongguan Excar, Eagle Electric, E-Z-GO, LANGQING, Langqing Electric, Lvtong, Marshell Green, and Yamaha. Companies competing in the Global Electric Golf Cart Market are adopting several strategies to strengthen their competitive positioning and expand their global presence. Manufacturers are focusing on continuous product innovation by integrating advanced battery technologies, improved vehicle efficiency, and enhanced durability features. Many companies are also expanding production capacity and strengthening supply chains to meet rising global demand for electric mobility solutions. Strategic partnerships with commercial operators, recreational facilities, and mobility service providers are helping companies expand their distribution reach. In addition, firms are investing in customization options, smart vehicle features, and improved after-sales service networks to enhance customer satisfaction and build long-term brand loyalty while securing a stronger foothold in the rapidly evolving electric golf cart market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery

- 2.2.3 Application

- 2.2.4 Sales channel

- 2.2.5 Seating capacity

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption in commercial and residential sectors

- 3.2.1.2 Shift toward lithium-ion batteries

- 3.2.1.3 Rising demand for low-emission mobility solutions

- 3.2.1.4 Smart connectivity & digital dashboards

- 3.2.1.5 Expansion of tourism & hospitality sector

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront cost of lithium-ion models

- 3.2.2.2 Battery replacement & disposal concerns

- 3.2.2.3 Limited speed & road regulations

- 3.2.2.4 Seasonal demand fluctuations

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in smart city & campus mobility

- 3.2.3.2 Customization & utility variants

- 3.2.3.3 Battery technology advancements

- 3.2.3.4 Fleet leasing & rental models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA) - FMVSS 500

- 3.4.1.3 Occupational Safety and Health Administration (OSHA)

- 3.4.1.4 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.1.5 State-Level Road Use Regulations

- 3.4.2 Europe

- 3.4.2.1 EU Machinery Directive

- 3.4.2.2 CE Marking Compliance

- 3.4.2.3 Low Voltage Directive (LVD)

- 3.4.2.4 Electromagnetic Compatibility (EMC) Directive

- 3.4.2.5 National Road Homologation Requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 Chinese EV & LSV Regulatory Framework

- 3.4.3.2 Indian Central Motor Vehicle Rules (CMVR)

- 3.4.3.3 Japanese Road Transport Vehicle Act

- 3.4.3.4 ASEAN EV Policy Harmonization Efforts

- 3.4.3.5 Australian Design Rules (ADR)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) Regulations

- 3.4.4.2 Mexican NOM Standards

- 3.4.4.3 Regional Urban Mobility & EV Incentive Programs

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Vehicle Compliance & Type Approval Regulations

- 3.4.5.2 South African National Road Traffic Act (NRTA)

- 3.4.5.3 Tourism & Free-Zone Operational Standards

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price analysis (Driven by Primary Research)

- 3.10.1 Historical Price Trend Analysis

- 3.10.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.11 Trade data analysis (Driven by Primary Research)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Cost breakdown analysis

- 3.13 Patent analysis (Driven by Primary Research)

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Impact of AI & generative AI on the market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Capacity & production landscape (Driven by Primary Research)

- 3.16.1 Installed capacity by region & key producer

- 3.16.2 Capacity utilization rates & expansion pipelines

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Battery, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Lead-acid

- 5.3 Lithium-ion

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Golf Course

- 6.3 Hotels and Resorts

- 6.4 Airports

- 6.5 Housing Projects

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By Seating Capacity, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 2-Seater

- 8.3 4-Seater

- 8.4 6-Seater

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Southeast Asia

- 9.4.6 ANZ

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Club Car

- 10.1.2 Columbia

- 10.1.3 Cushman

- 10.1.4 E-Z-GO

- 10.1.5 Garia

- 10.1.6 Polaris

- 10.1.7 Yamaha

- 10.2 Regional Players

- 10.2.1 Advanced EV

- 10.2.2 Bintelli

- 10.2.3 Evolution EV

- 10.2.4 Melex

- 10.2.5 Pilotcar

- 10.2.6 Star EV

- 10.2.7 Tomberlin

- 10.3 Emerging Players

- 10.3.1 Eco Planeta

- 10.3.2 Guangdong Lvtong

- 10.3.3 HDK

- 10.3.4 Jinghang Sightseeing

- 10.3.5 Langqing

- 10.3.6 Marshell

- 10.3.7 Suzhou Eagle