PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019030

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019030

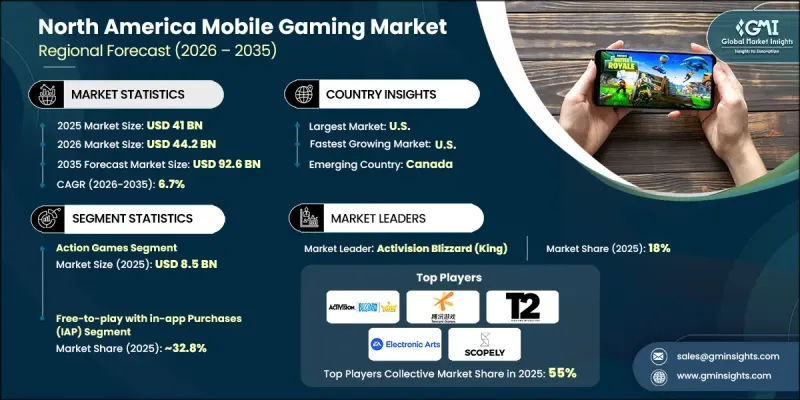

North America Mobile Gaming Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

North America Mobile Gaming Market was valued at USD 41 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 92.6 billion by 2035.

A high level of smartphone adoption, with more than 85% of adults using such devices, provides a solid foundation for market expansion by ensuring accessibility across diverse user groups. Advancements in network infrastructure are significantly enhancing gaming experiences, enabling developers to deliver high-quality, immersive gameplay on mobile platforms. These improvements are contributing to longer engagement times, higher retention levels, and increased revenue generation. In addition, the integration of advanced technologies is elevating overall gameplay experiences, making mobile gaming more interactive and dynamic. As consumer expectations continue to evolve, the market is benefiting from improved performance capabilities and richer content offerings. With strong digital infrastructure and a growing user base, mobile gaming is firmly positioned as a leading entertainment segment in North America, with promising growth prospects over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $41 Billion |

| Forecast Value | $92.6 Billion |

| CAGR | 6.7% |

Revenue models based on free access combined with optional spending have become a key factor supporting the expansion of the North America mobile gaming market. These approaches attract a large user base by minimizing initial barriers while enabling developers to generate income through digital transactions, subscriptions, and ongoing content updates. This model continues to strengthen user engagement and supports long-term revenue stability within the industry.

The action games segment generated USD 8.5 billion in 2025 owing to its strong appeal among a wide range of players. This category benefits from engaging gameplay mechanics, competitive elements, and immersive experiences that encourage repeat usage. High engagement levels are supported by continuous content updates and interactive features, which contribute to consistent monetization opportunities. The segment's popularity reflects user preference for dynamic and skill-driven gaming experiences within the region.

The smartphone segment is expected to experience the fastest growth during the forecast period and remains the dominant platform in the North America mobile gaming market. This dominance is driven by the widespread use of smartphones as a primary digital device, offering convenience and ease of access. Ongoing improvements in hardware performance, graphics capabilities, and display quality are enabling more sophisticated gaming experiences. These advancements are reducing the gap between mobile and traditional gaming platforms, further supporting segment growth.

United States Mobile Gaming Market accounted for 60% share in 2025, generating USD 25.3 billion. The country leads the regional market due to its large and active gaming population, high consumer spending, and advanced technological ecosystem. Strong user engagement across multiple gaming formats supports consistent revenue generation. A well-established digital environment and the presence of leading industry participants contribute to ongoing innovation and market development. The ability to effectively monetize through digital transactions and subscriptions further strengthens the country's dominant position.

Key companies operating in the North America Mobile Gaming Market include Tencent Games, Electronic Arts, Activision Blizzard (King), Take-Two Interactive (Zynga), NetEase Games, Supercell, Niantic, Scopely, Rovio Entertainment, Jam City, Krafton, Machine Zone (AppLovin), Com2Us Corporation, Lilith Games, and miHoYo. Companies in the North America Mobile Gaming Market are focusing on content innovation, user engagement, and monetization optimization to strengthen their competitive position. They are investing in high-quality game development and live service models to ensure continuous content updates and player retention. Strategic partnerships and acquisitions are being used to expand portfolios and enhance technological capabilities. Firms are also leveraging data analytics to better understand player behavior and personalize gaming experiences. Expanding cross-platform integration and improving in-game purchase systems are key priorities for maximizing revenue. Additionally, companies are increasing their focus on marketing strategies and community engagement to build strong player ecosystems and maintain long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Monetization model

- 2.2.4 Device type

- 2.2.5 Platform

- 2.2.6 Connectivity

- 2.2.7 Age group

- 2.2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High smartphone penetration & 5G network expansion

- 3.2.1.2 Freemium & in-app purchase model success in North America

- 3.2.1.3 Advancements in AR/VR & cloud gaming technologies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Intense competition & market saturation

- 3.2.2.2 Regulatory & privacy compliance costs

- 3.2.3 Opportunities

- 3.2.3.1 Hispanic gaming market growth

- 3.2.3.2 Cross-platform gaming & cloud gaming services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Regional pricing variations

- 3.7 Regulatory Framework

- 3.7.1 Data privacy & protection (CCPA, State-Level Privacy Laws)

- 3.7.2 Loot box & gacha regulations (State-by-State Analysis)

- 3.7.3 Age rating & content classification (ESRB Standards)

- 3.7.4 Payment & monetization regulations (Children's Online Privacy Protection Act - COPPA)

- 3.7.5 Gambling laws impact on casino & card games by state

- 3.7.6 Platform policy landscape (App Store Review Guidelines, Google Play Policies)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of game development (procedural content, NPC behavior)

- 3.10.2 GenAI use cases & adoption roadmap by segment (art assets, narrative, personalization)

- 3.10.3 Risks, limitations & regulatory considerations (copyright, content moderation)

- 3.10.4 North America leadership in AI gaming technologies

- 3.11 Consumer buying behavior analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Action games

- 5.3 Puzzle games

- 5.4 Role-playing games (RPG)

- 5.5 Strategy games

- 5.6 Simulation games

- 5.7 Sports games

- 5.8 Arcade & hyper-casual games

- 5.9 Adventure games

- 5.10 Card & casino games

- 5.11 Others (emerging & niche genres)

Chapter 6 Market Estimates and Forecast, By Monetization Model, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Premium

- 6.3 Free-to-play with in-app purchases (IAP)

- 6.4 Subscription-based models

- 6.5 Ad-supported (free) games

- 6.6 Hybrid (multiple revenue streams)

Chapter 7 Market Estimates and Forecast, By Device Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Smartphones

- 7.3 Tablets

- 7.4 Wearable devices

- 7.5 Others (feature phones & emerging devices)

Chapter 8 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 iOS

- 8.3 Android

- 8.4 Progressive web apps (PWAs)

- 8.5 Others (HarmonyOS & emerging platforms)

Chapter 9 Market Estimates and Forecast, By Connectivity, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online multiplayer games

- 9.3 Offline games

- 9.4 Hybrid connectivity games

Chapter 10 Market Estimates and Forecast, By Age Group, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Kids

- 10.3 Teenagers

- 10.4 Young adults

- 10.5 Adults

- 10.6 Seniors

Chapter 11 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 App store (iOS)

- 11.3 Google play store

- 11.4 Third-party app stores

- 11.5 Direct APK/sideloading

- 11.6 Social media platforms

- 11.7 Others (carrier pre-installs, OEM partnerships, web portals)

Chapter 12 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 U.S.

- 12.3 Canada

Chapter 13 Company Profiles

- 13.1 Activision Blizzard (King)

- 13.2 Electronic Arts

- 13.3 Take-Two Interactive (Zynga)

- 13.4 Tencent Games

- 13.5 NetEase Games

- 13.6 Niantic

- 13.7 Rovio Entertainment

- 13.8 Supercell

- 13.9 Scopely

- 13.10 Jam City

- 13.11 MachineZone (AppLovin)

- 13.12 Com2Us Corporation

- 13.13 Krafton

- 13.14 Lilith Games

- 13.15 miHoYo