PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019041

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019041

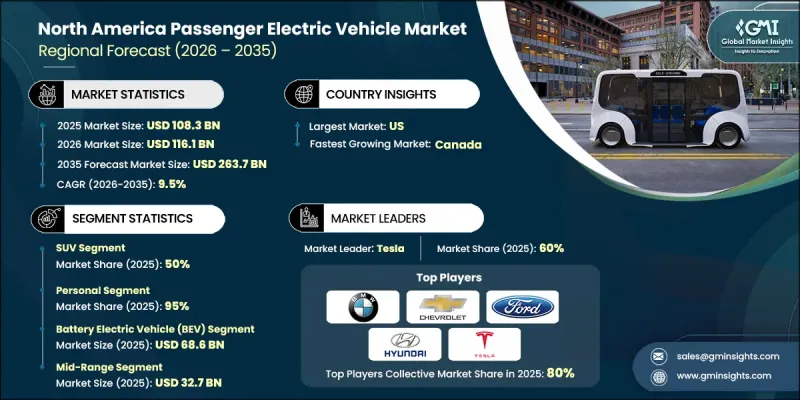

North America Passenger Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

North America Passenger Electric Vehicle Market was valued at USD 108.3 billion in 2025 and is estimated to grow at a CAGR of 9.5% to reach USD 263.7 billion by 2035.

The U.S. electric vehicle (EV) market includes battery electric vehicles, plug-in hybrid vehicles, and the supporting ecosystem, such as charging infrastructure, battery manufacturing, and software systems. Demand continues to expand as charging accessibility improves and technology advances enhance vehicle performance and convenience. Electric vehicles produce significantly lower emissions compared to conventional transportation, as they avoid releasing harmful greenhouse gases such as nitrogen oxides. They also offer quieter operation and simplified usability, which strengthens consumer appeal. Although the U.S. automotive sector experienced a sharp decline of approximately 23-24% in passenger vehicle sales during the COVID-19 pandemic due to economic disruption and mobility restrictions, EV adoption remained comparatively resilient. Long-term growth is being supported by rising consumer awareness, policy support, and continuous expansion of charging networks, which collectively improve the practicality and accessibility of EV ownership across North America.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $108.3 Billion |

| Forecast Value | $263.7 Billion |

| CAGR | 9.5% |

The SUV segment held a 50% share in 2025 and is forecast to grow at a CAGR of 10.7% from 2026 to 2035. Consumers increasingly prefer larger and more versatile electric vehicles, which is driving strong growth in this category. Automakers are expanding their electric SUV offerings and electrifying traditional vehicle segments to align with changing consumer expectations and evolving mobility trends.

The personal segment held a 95% share in 2025 and is expected to grow at a CAGR of 9.2% through 2035. Growth in personal EV adoption is supported by rising consumer interest, increasing product availability, and government-backed financial incentives that improve affordability. These factors are making electric vehicles a more practical choice for everyday use.

U.S. Passenger Electric Vehicle Market reached USD 98.7 billion in 2025. Market growth is fueled by strong consumer demand, supportive regulatory frameworks, and proactive strategies from original equipment manufacturers. Companies are focusing on scalable EV platforms to improve efficiency and accelerate model development, while also adjusting their competitive positioning to capture a larger share of the evolving market landscape.

Key participants in the North America Passenger Electric Vehicle Market include BMW, BYD Company, Ford Motor Company, Geely Automobile, General Motors Company, Hyundai Motor Company, Kia, Stellantis, Tesla, and Volkswagen. Companies operating in the North America Passenger Electric Vehicle Market are strengthening their market position through a combination of innovation, expansion, and strategic alignment. They are investing heavily in research and development to enhance battery efficiency, driving range, and vehicle performance. Firms are also scaling production capabilities and developing flexible EV platforms that support multiple models, enabling cost optimization and faster time-to-market. Strategic partnerships and collaborations are being used to accelerate technology development and expand infrastructure networks. In addition, companies are focusing on enhancing charging accessibility, improving software integration, and delivering connected vehicle experiences. Market players are also aligning their portfolios with consumer demand by increasing the availability of diverse EV models while leveraging government incentives and regulatory support to boost adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Drive

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.2.6 Price

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Battery Manufacturer

- 3.1.1.2 Component Supplier

- 3.1.1.3 OEM (Original Equipment Manufacturer)

- 3.1.1.4 Distributor / Deale

- 3.1.1.5 Battery Manufacturer

- 3.1.1.6 End user

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Strict emission regulations enforcement

- 3.2.1.2 Growing consumer preference for sustainable mobility

- 3.2.1.3 Expansion of EV model availability

- 3.2.1.4 Urban air quality improvement initiatives

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High vehicle costs and battery supply constraints

- 3.2.2.2 Consumer range anxiety

- 3.2.3 Market opportunities

- 3.2.3.1 High-power fast charging deployment

- 3.2.3.2 Battery cost reductions and technological advances

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 US

- 3.5.1.1 U.S. Federal Motor Vehicle Safety Standards

- 3.5.2 Canada

- 3.5.2.1 Canadian Electric Vehicle Safety Regulations

- 3.5.1 US

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.1.1 Predictive Maintenance & Operations Optimization

- 3.13.1.2 Automated design optimization

- 3.13.1.3 Supply chain AI for demand forecasting

- 3.13.1.4 GenAI use cases & adoption roadmap by segment

- 3.13.1.4.1 Tread pattern design generation

- 3.13.1.4.2 Customer service chatbots & technical support

- 3.13.1.4.3 Marketing content creation

- 3.13.1.4.4 Risks, limitations & regulatory considerations

- 3.13.1.4.4.1 Data privacy in IoT-enabled smart product

- 3.13.1.4.4.2 AI algorithm transparency requirements

- 3.13.1.4.4.3 Liability in AI-driven product failures

- 3.13.1 AI-driven disruption of existing business models

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 US

- 4.2.2 Canada

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Hatchback

- 5.3 Sedan

- 5.4 SUV

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Drive , 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Front-wheel drive

- 6.3 Rear-wheel drive

- 6.4 All-wheel drive

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Battery Electric Vehicle (BEV)

- 7.3 Fuel Cell Electric Vehicle (FCEV)

- 7.4 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Price, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Entry

- 9.3 Mid-Range

- 9.4 Luxury

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 10.1 Key trends

- 10.2 US

- 10.2.1 Northeast

- 10.2.1.1 Maine

- 10.2.1.2 New Hampshire

- 10.2.1.3 Vermont

- 10.2.1.4 Massachusetts

- 10.2.1.5 Rhode Island

- 10.2.1.6 Connecticut

- 10.2.1.7 New York

- 10.2.1.8 New Jersey

- 10.2.1.9 Pennsylvania

- 10.2.1.10 Delaware

- 10.2.1.11 Maryland

- 10.2.2 Southeast

- 10.2.2.1 Virginia

- 10.2.2.2 West Virginia

- 10.2.2.3 North Carolina

- 10.2.2.4 South Carolina

- 10.2.2.5 Georgia

- 10.2.2.6 Florida

- 10.2.2.7 Alabama

- 10.2.2.8 Mississippi

- 10.2.2.9 Tennessee

- 10.2.2.10 Kentucky

- 10.2.2.11 Arkansas

- 10.2.2.12 Louisiana

- 10.2.3 Midwest

- 10.2.3.1 Ohio

- 10.2.3.2 Indiana

- 10.2.3.3 Illinois

- 10.2.3.4 Michigan

- 10.2.3.5 Wisconsin

- 10.2.3.6 Minnesota

- 10.2.3.7 Iowa

- 10.2.3.8 Missouri

- 10.2.3.9 North Dakota

- 10.2.3.10 South Dakota

- 10.2.3.11 Nebraska

- 10.2.3.12 Kansas

- 10.2.4 West

- 10.2.4.1 Montana

- 10.2.4.2 Idaho

- 10.2.4.3 Wyoming

- 10.2.4.4 Colorado

- 10.2.4.5 New Mexico

- 10.2.4.6 Arizona

- 10.2.4.7 Utah

- 10.2.4.8 Nevada

- 10.2.4.9 Washington

- 10.2.4.10 Oregon

- 10.2.4.11 California

- 10.2.4.12 Alaska

- 10.2.4.13 Hawaii

- 10.2.4.14 Oklahoma

- 10.2.4.15 Texas

- 10.2.1 Northeast

- 10.3 Canada

- 10.3.1 British Columbia

- 10.3.2 Alberta

- 10.3.3 Saskatchewan

- 10.3.4 Manitoba

- 10.3.5 Ontario

- 10.3.6 Quebec

- 10.3.7 New Brunswick

- 10.3.8 Nova Scotia

- 10.3.9 Yukon

- 10.3.10 Nunavut

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 BMW

- 11.1.2 BYD Company

- 11.1.3 Ford Motor Company

- 11.1.4 Geely Automobile

- 11.1.5 General Motors Company

- 11.1.6 Hyundai Motor Company

- 11.1.7 Kia

- 11.1.8 Stellantis

- 11.1.9 Tesla

- 11.1.10 Volkswagen

- 11.2 Regional players

- 11.2.1 Changan Automobile

- 11.2.2 Chery Automobile

- 11.2.3 NIO

- 11.2.4 Renault

- 11.2.5 SAIC Motor

- 11.2.6 Tata Motors

- 11.3 Emerging players

- 11.3.1 Lucid Motors

- 11.3.2 Polestar Automotive

- 11.3.3 Rivian Automotive

- 11.3.4 VinFast Auto