PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019045

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019045

Europe High Performance Air Filtration for Cleanrooms, Hospitals, and High-End Industrial Processes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

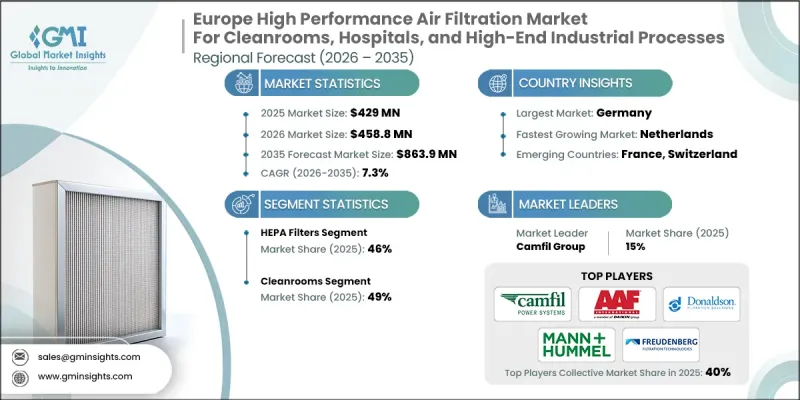

Europe High Performance Air Filtration for Cleanrooms, Hospitals, and High-End Industrial Processes Market was valued at USD 429 million in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 863.9 million by 2035.

The Europe high performance air filtration market is evolving as critical environments demand consistently clean air to ensure uninterrupted operations and maintain safety standards. Healthcare facilities rely heavily on advanced filtration systems to support sterile conditions and safeguard patient care. Similarly, controlled production environments depend on precise air filtration to maintain consistent output quality and avoid contamination risks. The increasing complexity of industrial processes is further driving the need for reliable filtration solutions that can maintain stable conditions. Continuous technological advancements are enhancing filtration efficiency and system integration, enabling facilities to achieve higher levels of performance. As industries modernize, the demand for high-performance air filtration systems across Europe continues to expand, supported by strict operational and environmental expectations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $429 Million |

| Forecast Value | $863.9 Million |

| CAGR | 7.3% |

The Europe high performance air filtration market is also influenced by evolving regulatory frameworks that are encouraging facilities to upgrade filtration systems to meet stricter compliance requirements. As operational processes become more sensitive, industries are increasingly dependent on advanced filtration technologies to maintain clean environments and protect product integrity. Ongoing improvements in airflow control and environmental monitoring are supporting consistent performance in controlled spaces. Facilities are investing in upgrades to maintain operational stability and meet changing compliance standards, reinforcing the importance of advanced filtration solutions across the region.

In 2025, the HEPA filters segment accounted for 46% share for cleanrooms, hospitals, and high-end industrial processes. These filters remain a core component of high-efficiency filtration systems due to their ability to capture extremely fine particles and maintain air purity standards. Their long-standing reliability and compliance with stringent regulatory requirements have supported their widespread adoption. At the same time, ULPA filters are witnessing increased demand as industries move toward stricter air quality standards. These advanced systems are designed to capture even smaller particles, making them suitable for environments requiring higher levels of filtration performance.

In 2025, the cleanrooms segment held a 49% share, generating USD 210.6 million. Controlled environments are becoming increasingly important across industries that require strict contamination control and consistent environmental conditions. The expansion of advanced manufacturing sectors is driving demand for highly regulated environments, where even minor variations can affect production quality and compliance. Continuous investments in cleanroom infrastructure are supporting the need for high-performance filtration systems, ensuring stable operations and adherence to strict regulatory standards.

Germany High Performance Air Filtration for Cleanrooms, Hospitals, and High-End Industrial Processes Market held 26% share, generating USD 111.5 million in 2025. The regional market landscape reflects differences in industrial development, regulatory enforcement, and infrastructure maturity. Western Europe remains a key hub due to strong compliance frameworks and widespread adoption of advanced filtration technologies. Countries such as France and United Kingdom continue to contribute significantly through well-established industrial ecosystems and consistent demand for contamination control solutions.

Key companies operating in the Europe High Performance Air Filtration for Cleanrooms, Hospitals, and High-End Industrial Processes Market for cleanrooms, hospitals, and high-end industrial processes include Alulux GmbH, Alumil, Aluprof SA, ASSA ABLOY, Bubendorff, Griesser AG, heroal, Hormann Group, Internorm International GmbH, Novoferm GmbH, Roma KG, Schenker Storen AG, Schuco International KG, Teckentrup, and WAREMA Renkhoff SE. Companies in the Europe High Performance Air Filtration for Cleanrooms, Hospitals, and High-End Industrial Processes Market are strengthening their competitive position through innovation, regulatory alignment, and strategic expansion. They are investing in advanced filtration technologies to improve efficiency, enhance particle capture capabilities, and support evolving industry standards. Collaborations with industrial operators and healthcare providers are helping to accelerate the adoption and integration of high-performance systems. Market participants are also focusing on expanding their regional presence through partnerships and distribution networks. Continuous upgrades in product design, along with the integration of monitoring and control systems, are enabling companies to deliver value-added solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Installation Type

- 2.2.4 Application

- 2.2.5 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Strict air quality and contamination control standards

- 3.2.1.2 Rising need for controlled environments in critical industries

- 3.2.1.3 Growing adoption of cleanrooms requiring continuous upgrades

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Rapid technological advancements leading to system obsolescence

- 3.2.2.2 High operational and maintenance demands

- 3.2.3 Opportunities

- 3.2.3.1 Development of smarter, predictive filtration systems

- 3.2.3.2 Increasing shift toward sustainable, energy-efficient filtration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Trade data analysis

- 3.5.1 Import/export volume & value trends

- 3.5.2 Key trade corridors & tariff impact

- 3.6 Impact of ai & generative ai on the market

- 3.6.1 AI-driven disruption of existing business models

- 3.6.2 Gen AI use cases & adoption roadmap by segment

- 3.6.3 Risks, limitations & regulatory considerations

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By product type

- 3.8.2 By region

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirements

- 3.9.2 Regional regulatory frameworks

- 3.9.3 Certification standards

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035(USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 HEPA filters

- 5.2.1 HEPA H13

- 5.2.2 HEPA H14

- 5.3 ULPA Filters

- 5.3.1 ULPA U15

- 5.3.2 ULPA U16

- 5.3.3 ULPA U17

- 5.4 ePM1/F-class filters

- 5.4.1 ePM1

- 5.4.2 ePM1

- 5.4.3 F7/F8/F9

Chapter 6 Market Estimates and Forecast, By Slat Material, 2022 - 2035(USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Upstream AHU/CTA installation

- 6.2.1 Stationary AHU systems

- 6.2.2 Mobile/portable AHU units

- 6.3 Direct point-of-use installation

- 6.3.1 Stationary point-of-use equipment

- 6.3.2 Mobile point-of-use equipment

- 6.4 Other installation types

- 6.4.1 Stationary recirculation systems

- 6.4.2 Portable air purifiers

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022 - 2035(USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Cleanrooms

- 7.2.1 Pharmaceutical cleanrooms

- 7.2.2 Semiconductor cleanrooms

- 7.2.3 Biotechnology cleanrooms

- 7.3 Healthcare & Hospitals

- 7.3.1 Operating theaters

- 7.3.2 Isolation rooms

- 7.3.3 General hospital HVAC

- 7.4 High-End Industrial Processes

- 7.4.1 Precision manufacturing

- 7.4.2 Advanced materials processing

- 7.4.3 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035(USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Country, 2022 - 2035(USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Germany

- 9.3 United Kingdom

- 9.4 France

- 9.5 Italy

- 9.6 Spain

- 9.7 Netherlands

- 9.8 Switzerland

Chapter 10 Company Profiles

- 10.1 CAMFIL GROUP

- 10.2 AAF International (Daikin)

- 10.3 MANN+HUMMEL

- 10.4 Donaldson Company

- 10.5 Freudenberg Filtration

- 10.6 Parker Hannifin

- 10.7 Filtration Group Corp

- 10.8 BWF Group

- 10.9 ENVI-FILTER

- 10.10 3M

- 10.11 Mikropor

- 10.12 Mortelecque

- 10.13 Euromate B.V.

- 10.14 SDC (Scientific Dust Collectors)

- 10.15 Indair B.V.