PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019054

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019054

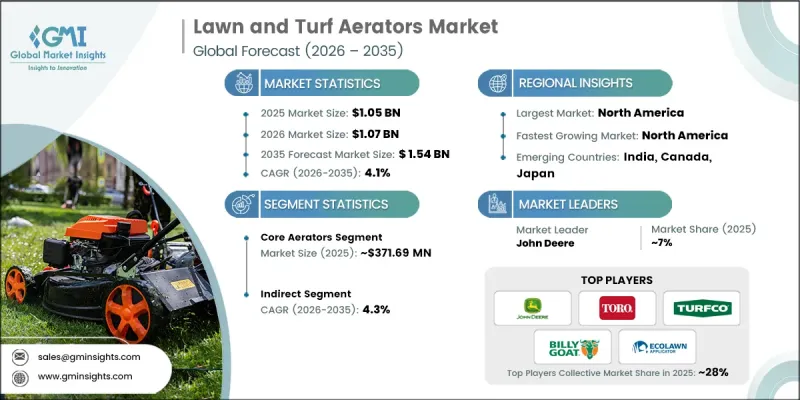

Lawn and Turf Aerators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Lawn and Turf Aerators Market was valued at USD 1.05 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 1.54 billion by 2035.

The market is rapidly growing due to the increasing interest in home lawn care and landscaping projects. Homeowners and gardening enthusiasts are investing in equipment that enhances soil aeration, strengthens root systems, and maintains lush, healthy turf. Aerators help reduce soil compaction, improve nutrient absorption, and support sustainable grass growth. Professional landscapers and recreational facility managers are adopting both mechanical and manual aeration solutions to maintain the quality of lawns and turf. Additionally, the growth of golf courses, sports fields, and recreational facilities is fueling demand, as these venues require well-maintained, resilient turf to provide optimal performance and safety for users. The combination of residential landscaping, professional turf management, and recreational maintenance is driving sustained growth for the global lawn and turf aerators market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.05 Billion |

| Forecast Value | $1.54 Billion |

| CAGR | 4.1% |

The core aerators segment accounted for USD 371.69 million in 2025 and is expected to grow at a CAGR of 4.5% through 2035. Core aerators lead the market due to their efficiency in improving soil health and promoting robust grass growth. By extracting soil plugs, they enhance water, air, and nutrient penetration, reduce compaction, and strengthen turf density. These aerators are widely utilized in golf courses, sports fields, commercial landscapes, and high-maintenance residential lawns. The increasing focus on sustainable lawn care, professional turf management, and recreational facility upkeep supports the widespread adoption of core aerators. Their proven reliability, performance consistency, and effectiveness ensure they remain a dominant solution in the global lawn and turf aerators industry.

The indirect distribution segment held a 53.2% share in 2025 and is projected to grow at a CAGR of 4.3% through 2035. This dominance is driven by the reliance on distributors, dealers, and regional partners to reach end users efficiently. Manufacturers use these channels to provide local sales, technical guidance, and after-sales support, particularly for professional-grade and commercial aeration equipment. Indirect channels facilitate quicker market penetration, installation assistance, and access to replacement parts for golf courses, municipal maintenance teams, and landscaping companies. The expertise, service, and timely support offered by distributors and dealers reinforce the prevalence of indirect distribution across the market.

U.S. Lawn and Turf Aerators Market reached USD 218.1 million in 2025 and is expected to grow at a CAGR of 4.5% through 2035. Growth is fueled by rising investments in residential landscaping, commercial turf maintenance, and sports facilities. Homeowners utilize aerators to maintain healthy lawns, enhance soil aeration, and support grass growth, particularly in areas with compacted soils or seasonal stress. Golf courses, athletic fields, and public parks rely on heavy-duty aerators to maintain large turf areas efficiently. Manufacturers focus on manual and motorized models with features such as adjustable tines, portability, and user-friendly operation to meet varying customer requirements.

Key players operating in the Global Lawn and Turf Aerators Market include Toro, Jacobsen, John Deere, Wiedenmann, Schiller Grounds Care, Turfco, Billy Goat, Salford, Classen, Millcreek, 1st Products, Blec Global, Groundsman, Ecolawn, and Ryan. Companies in the lawn and turf aerators market are strengthening their presence by expanding distribution networks and forming partnerships with dealers and landscaping service providers. They are investing in R&D to develop ergonomic, durable, and high-performance aerators, including manual and motorized models, to cater to both residential and commercial users. Manufacturers are emphasizing sustainability by offering reusable and eco-friendly components while integrating advanced features such as adjustable tines, portability, and ease of use. Strategic marketing campaigns, localized sales support, and after-sales service programs help build brand loyalty, particularly among professional turf managers, municipal teams, and golf course operators. Expansion into emerging markets and collaboration with recreational facility operators also support long-term market foothold and growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Power Source

- 2.2.4 Application

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing interest in residential lawn care and landscaping activities

- 3.2.1.2 Expansion of golf courses, sports fields, and recreational facilities

- 3.2.1.3 Growth of landscaping and grounds maintenance service providers

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High cost of professional-grade aeration equipment

- 3.2.2.2 Seasonal demand patterns linked to turf maintenance cycles

- 3.2.3 Opportunities

- 3.2.3.1 Increasing adoption of battery-powered and electric lawn care equipment

- 3.2.3.2 Growth of contract-based lawn care services in urban and suburban areas

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research) (2019-2024)

- 3.9.2 Pricing strategy by player type (premium/value/cost-plus) (driven by primary research)

- 3.9.3 Price elasticity of demand analysis

- 3.9.4 Regional price variation & purchasing power parity

- 3.9.5 Online vs offline channel price differential

- 3.10 Trade data analysis (HS code 820551) (driven by primary research)

- 3.10.1 Import/export volume & value trends (driven by primary research) (2019-2024)

- 3.10.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10.3 Top 10 exporting countries analysis

- 3.10.4 Top 10 importing countries analysis

- 3.10.5 Trade balance & net export positions

- 3.10.6 Impact of trade agreements & tariff changes

- 3.11 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.11.1 Channel coverage by region & format (modern vs traditional trade) (driven by primary research)

- 3.11.2 Last-mile infrastructure gaps & emerging channel shifts (driven by primary research)

- 3.11.3 E-commerce platform penetration analysis

- 3.11.4 Specialty retail presence & wine store partnerships

- 3.11.5 Direct-to-consumer channel development

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Core aerators

- 5.3 Spike aerators

- 5.4 Liquid aerators

- 5.5 Rolling aerators

- 5.6 Tow-behind aerators

Chapter 6 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual aerators

- 6.3 Electric aerators

- 6.4 Powered aerators

- 6.5 Gas-powered aerators

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Residential lawns

- 7.3 Golf courses

- 7.4 Sports fields

- 7.5 Commercial landscapes

- 7.6 Agricultural land

- 7.7 Public spaces and parks

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 1st Products

- 10.2 Billy Goat

- 10.3 Blec Global

- 10.4 Classen

- 10.5 Ecolawn

- 10.6 Groundsman

- 10.7 Jacobsen

- 10.8 John Deere

- 10.9 Millcreek

- 10.10 Ryan

- 10.11 Salford

- 10.12 Schiller Grounds Care

- 10.13 Toro

- 10.14 Turfco

- 10.15 Wiedenmann