PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019058

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019058

Robotic Lawn Mower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

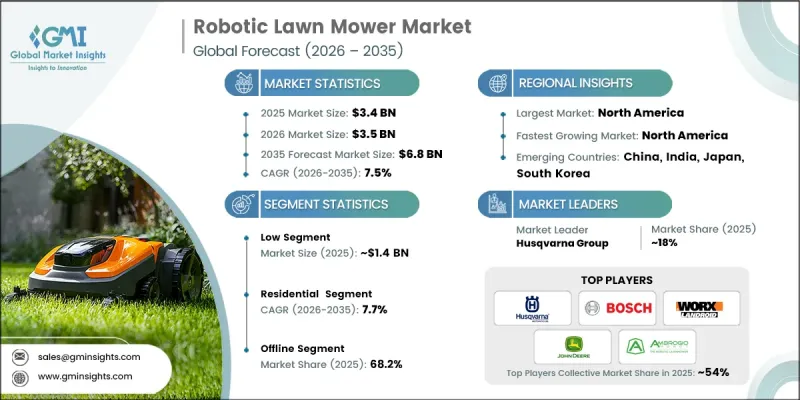

The Global Robotic Lawn Mower Market was valued at USD 3.4 billion in 2025 and is estimated to grow at a CAGR of 7.5% to reach USD 6.8 billion by 2035.

Growth in the robotic lawn mower market is fueled by the increasing adoption of intelligent home solutions that simplify routine outdoor maintenance. Consumers are increasingly embracing automated equipment that reduces manual workload while delivering consistent results. These devices operate through programmable systems supported by sensors, enabling efficient and autonomous lawn care. Integration with digital ecosystems allows users to manage operations through mobile platforms, enhancing convenience and control. Rising preference for low-effort and time-saving solutions is encouraging homeowners to invest in such technologies. Additionally, the shift toward compact living spaces is increasing the demand for efficient and space-conscious equipment. Battery advancements are further improving operational efficiency, runtime, and durability, strengthening product reliability. Environmentally conscious purchasing behavior is also supporting the adoption of electric-powered systems, positioning the robotic lawn mower market for sustained expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.4 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 7.5% |

The robotic lawn mower industry is witnessing strong momentum due to rapid technological advancements and growing consumer awareness regarding automated outdoor solutions. Enhanced navigation capabilities, improved obstacle detection systems, and smarter connectivity features are enabling better performance across varied lawn conditions. The market is also benefiting from the increasing emphasis on energy-efficient devices that align with modern sustainability goals. As automation continues to evolve, manufacturers are focusing on delivering products that combine precision, durability, and ease of use, ensuring broader acceptance across residential and commercial users.

The low cutting height segment generated USD 1.4 billion in 2025 and is projected to grow at a CAGR of 7.6% through 2035. This segment continues to lead due to rising demand for well-maintained and visually appealing turf surfaces. Users prefer shorter grass levels that enhance uniformity and overall landscape aesthetics. Advanced robotic systems are designed to maintain consistent cutting performance at lower heights without affecting operational efficiency. Automated functionality reduces labor requirements while maintaining precise trimming standards. Increasing adoption of smart landscaping solutions further supports the expansion of this segment, reinforcing its strong position within the robotic lawn mower market.

The offline distribution channel accounted for 68.2% share in 2025 and is anticipated to grow at a CAGR of 7.3% through 2035. Physical retail channels continue to dominate as consumers value direct product evaluation before purchase. In-store interactions allow buyers to assess product specifications, build quality, and functional capabilities more effectively. Personalized assistance from sales professionals helps customers select suitable products based on lawn size and terrain conditions. Immediate product access and reliable after-sales services further strengthen the importance of offline channels, maintaining their strong presence in the market landscape.

U.S. Robotic Lawn Mower Market accounted for USD 1.2 billion in 2025 and is expected to grow at a CAGR of 8.1% through 2035, leading the North America region. Market expansion is supported by increasing adoption of automated home maintenance tools and strong consumer spending capacity. Growing interest in connected devices and smart technologies is driving demand for app-enabled and GPS-supported solutions. Product innovation focused on improving navigation accuracy, weather adaptability, and operational efficiency continues to shape the competitive environment. The increasing inclination toward quieter and energy-efficient equipment further contributes to sustained market growth across the region.

Key players in the Global Robotic Lawn Mower Market include Ambrogio, Dreame, Echo Robotics, Ecoflow, Gardena, Honda Motor Company, Husqvarna Group, John Deere, Kress Robotics, Mammotion, Robert Bosch, Robomow, Traqnology, Worx Landroid, and Yarbo. Companies in the Global Robotic Lawn Mower Market are strengthening their competitive position through continuous product innovation, strategic partnerships, and expansion of distribution networks. Manufacturers are investing in advanced technologies such as artificial intelligence, sensor integration, and connectivity features to enhance product efficiency and user experience. They are also focusing on improving battery performance and durability to extend operational capabilities. Expanding retail presence and strengthening dealer networks remain key priorities to improve market accessibility. In addition, companies are emphasizing sustainability by developing energy-efficient and eco-friendly products. Collaborations with technology providers are enabling the development of smarter solutions, while enhanced after-sales services and customer support are helping build long-term brand loyalty and market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By Type

- 2.2.3 By Cutting Height

- 2.2.4 By Lawn Size

- 2.2.5 By Battery Capacity

- 2.2.6 By Price

- 2.2.7 By End Use

- 2.2.8 By Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for smart and autonomous home solutions

- 3.2.1.2 Growth in residential landscaping and outdoor living trends

- 3.2.1.3 Expansion of e-commerce and omnichannel distribution

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High upfront purchase cost relative to traditional mowers

- 3.2.2.2 Complexity of installation and boundary setup

- 3.2.3 Opportunities

- 3.2.3.1 Integration with smart home ecosystems and voice assistants

- 3.2.3.2 Development of advanced terrain-adaptive and all-weather models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Fully autonomous

- 5.3 Semi-autonomous

Chapter 6 Market Estimates & Forecast, By Cutting Height, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low (0.5 inch to 1 inch)

- 6.3 Medium (1 inch to 1.5 inch)

- 6.4 High (1.5 inches to 2 inches)

Chapter 7 Market Estimates & Forecast, By Lawn Size, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Small Lawns (up to 0.25 acres)

- 7.3 Medium Lawns (0.25 - 0.5 acres)

- 7.4 Large Lawns (0.5 acres and above)

Chapter 8 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Up to 20V

- 8.3 20V to 30V

- 8.4 Above 30V

Chapter 9 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 Company websites

- 11.2.2 E-commerce

- 11.3 Offline

- 11.3.1 Specialty stores

- 11.3.2 Supermarket/hypermarket

- 11.3.3 Others

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Ambrogio

- 13.2 Dreame

- 13.3 Echo Robotics

- 13.4 Ecoflow

- 13.5 Gardena

- 13.6 Honda Motor Company

- 13.7 Husqvarna Group

- 13.8 John Deere

- 13.9 Kress Robotics

- 13.10 Mammotion

- 13.11 Robert Bosch

- 13.12 Robomow

- 13.13 Traqnology

- 13.14 Worx Landroid

- 13.15 Yarbo