PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019091

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019091

Unit Load Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

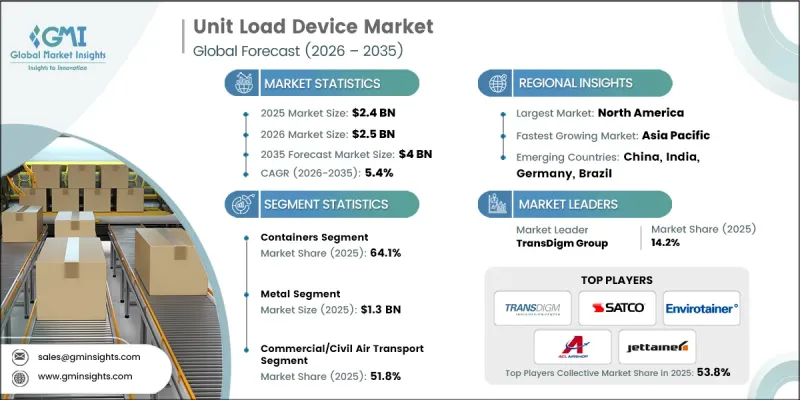

The Global Unit Load Device Market was estimated at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 4 billion by 2035.

Market expansion is fueled by the rapid acceleration of air freight activity and the continuous rise in e-commerce logistics, both of which demand faster and more efficient cargo movement systems. Increasing deliveries of wide-body aircraft and dedicated freighters are further strengthening demand, as each aircraft requires compatible cargo handling solutions. The industry is also experiencing a shift toward advanced materials, with lightweight composite and hybrid ULDs gaining traction due to their operational and fuel-saving benefits. Additionally, airlines are increasingly turning toward outsourcing and pooling services to streamline operations and reduce costs. The integration of temperature-sensitive logistics and improved cargo protection systems is also shaping demand patterns, while digital tracking technologies continue to enhance efficiency, visibility, and asset utilization across global aviation logistics networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $4 Billion |

| CAGR | 5.4% |

The expansion of air cargo operations and cross-border e-commerce activity continues to significantly influence demand for unit load devices, as growing shipment volumes require streamlined cargo handling and quicker aircraft turnaround times. Increasing reliance on both dedicated cargo aircraft and passenger aircraft belly capacity is driving the need for standardized containers and pallets. At the same time, the rise in global aircraft fleet size is creating sustained demand for both factory-installed and replacement ULD solutions, supporting long-term market growth across airline and cargo operator segments.

The transition toward composite and hybrid ULD materials is transforming the competitive landscape, as airlines prioritize weight reduction and fuel efficiency. Compared to traditional aluminum structures, composite designs offer improved durability, reduced maintenance requirements, and better adaptability for temperature-controlled cargo transport. These innovations are particularly valuable for handling sensitive and high-value goods, contributing to their growing adoption across global aviation logistics systems.

The containers segment accounted for 64.1% share in 2025, supported by its flexibility, durability, and compatibility across various aircraft types. These containers facilitate efficient loading and unloading processes while offering enhanced cargo protection and supporting specialized transport needs such as temperature-sensitive shipments. Their standardized formats contribute to improved operational efficiency and better utilization of airline fleets, making them a preferred choice for both passenger and cargo operations.

The composite materials segment is anticipated to grow at a CAGR of 7.2% during 2026-2035, driven by the aviation sector's increasing focus on lightweight and fuel-efficient solutions. These materials contribute to reduced aircraft weight, higher payload capacity, and improved design flexibility, enabling modular and temperature-controlled configurations. As airlines and logistics providers seek cost efficiency and sustainability, composite ULDs are becoming an essential component of modern cargo operations.

North America Unit Load Device Market accounted for 36.9% share in 2025, supported by strong air cargo infrastructure and high passenger traffic across the region. Continued fleet expansion and increasing shipment volumes from e-commerce are driving demand for standardized cargo solutions. Advanced logistics systems and infrastructure enhance ULD handling efficiency, while growing investments in digital tracking and IoT-enabled systems improve operational visibility and asset management. The region is also witnessing increased adoption of lightweight ULD solutions to reduce operational costs and improve fuel efficiency. Additionally, the rising preference for outsourced ULD pooling and maintenance services is enabling airlines to focus on core operations while ensuring optimized resource utilization.

Key players operating in the Global Unit Load Device Market include TransDigm Group, Safran Group, Unilode Aviation Solutions, Envirotainer AB, CSafe Global, Jettainer GmbH, ACL Airshop, Satco, Inc., Brambles Limited (CHEP Aerospace Solutions), DoKaSch GmbH, Nordisk Aviation Products AS, PalNet GmbH, Cargo Composites, VRR Aviation, Taiwan Fylin Industrial Co., Ltd., Wuxi Aviation Products Co., Ltd., Shanghai Avifit Co., Ltd., and AAR Corp. Companies in the Unit Load Device Market are focusing on strategic initiatives to strengthen their competitive position and expand global reach. They are investing in advanced materials such as composites to improve product performance and reduce lifecycle costs. Partnerships and long-term contracts with airlines and logistics providers are being prioritized to secure recurring revenue streams. Firms are also expanding ULD pooling and leasing services to enhance customer flexibility and operational efficiency. Digital transformation, including IoT-based tracking and fleet management systems, is becoming a key focus area to improve asset visibility and utilization.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product Type trends

- 2.2.2 Material trends

- 2.2.3 Container Type trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of air cargo and e-commerce operations

- 3.2.1.2 Growth in wide-body and freighter aircraft deliveries

- 3.2.1.3 Rising adoption of lightweight composite and temperature-controlled ULDs

- 3.2.1.4 Digitalization and IoT-enabled smart ULDs

- 3.2.1.5 Increasing airline outsourcing and pooling services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced composite and smart ULDs

- 3.2.2.2 Regulatory and certification compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growing ULD retrofit and replacement cycle

- 3.2.3.2 Expansion of air cargo in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Containers

- 5.2.1 LD containers

- 5.2.2 Main deck containers

- 5.3 Pallets

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Composite

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Container Type, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Standard container

- 7.3 Temperature-controlled container

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Commercial/civil air transport

- 8.3 Cargo/freight air transport

- 8.4 Military & special mission aircraft

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 TransDigm Group

- 10.1.2 Safran Group

- 10.1.3 Unilode Aviation Solutions

- 10.1.4 Envirotainer AB

- 10.1.5 CSafe Global

- 10.1.6 Jettainer GmbH

- 10.1.7 ACL Airshop

- 10.2 Regional Players

- 10.2.1 Satco, Inc.

- 10.2.2 Brambles Limited (CHEP Aerospace Solutions)

- 10.2.3 DoKaSch GmbH

- 10.2.4 Nordisk Aviation Products AS

- 10.2.5 PalNet GmbH

- 10.3 Niche Players

- 10.3.1 Cargo Composites

- 10.3.2 VRR Aviation

- 10.3.3 Taiwan Fylin Industrial Co., Ltd.

- 10.3.4 Wuxi Aviation Products Co., Ltd.

- 10.3.5 Shanghai Avifit Co., Ltd.

- 10.3.6 AAR Corp