PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019098

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019098

Passenger Car Seat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

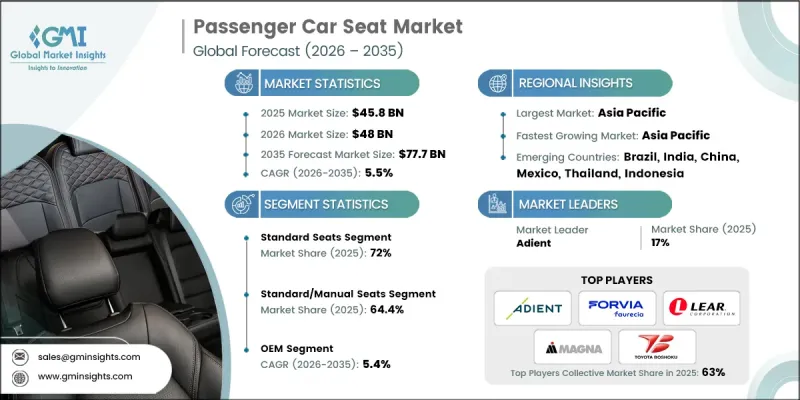

The Global Passenger Car Seat Market was valued at USD 45.8 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 77.7 billion by 2035.

The global passenger car seat market is evolving alongside advancements in vehicle design, where seating systems play a critical role in enhancing passenger experience and structural safety. Modern seating solutions are engineered with lightweight materials, improved cushioning, and integrated electronic functionalities to deliver better ergonomics and durability. Increasing focus on vehicle interior quality and occupant well-being is encouraging the development of advanced seating technologies. At the same time, manufacturers are integrating safety systems within seat structures to support overall vehicle protection standards. Rising production of passenger vehicles, combined with growing consumer preference for enhanced comfort and premium features, is driving steady demand. The expansion of advanced vehicle segments and continuous innovation in materials and design are further strengthening the growth trajectory of the passenger car seat market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.8 Billion |

| Forecast Value | $77.7 Billion |

| CAGR | 5.5% |

The passenger car seat market includes a wide range of configurations, covering front and rear seating systems along with advanced seating technologies designed to enhance user experience. Manufacturers are focusing on delivering complete seat assemblies and components that combine lightweight construction with smart features to improve efficiency and reduce overall vehicle weight. Increasing consumer expectations for enhanced comfort and functionality are encouraging the integration of advanced technologies into seating systems. In addition, rising vehicle ownership and improving economic conditions in emerging regions are contributing to market expansion, particularly as demand for improved interior features continues to grow.

In 2025, the standard seats segment held a 72% share and is expected to grow at a CAGR of 5.7% from 2026 to 2035. This segment's leadership is largely driven by high production volumes of widely adopted passenger vehicles, where cost-effective and durable seating solutions are essential. Standard seating systems are designed to provide a balance between functionality, comfort, and affordability, making them suitable for large-scale automotive manufacturing. Their simple design and reliable performance continue to support widespread adoption across multiple markets.

The OEM segment accounted for 87% share in 2025 and is projected to grow at a CAGR of 5.4% through 2035. This segment represents seating systems supplied directly to vehicle manufacturers through long-term partnerships and integrated production processes. OEM suppliers collaborate closely with automakers during the design and development phases, ensuring seamless integration with vehicle architecture. These partnerships involve coordinated production planning, strict quality standards, and ongoing engineering support, enabling efficient delivery and consistent product performance across vehicle programs.

China Passenger Car Seat Market is expected to grow at a CAGR of 5.5% from 2026 to 2035. The country's strong automotive manufacturing ecosystem and integrated supply chain are driving significant demand for seating systems. High vehicle production volumes are supporting the widespread adoption of both basic and advanced seating technologies. Continuous advancements in manufacturing capabilities and strategic collaborations with automotive manufacturers are strengthening the country's position in the regional market. The growing focus on innovation and efficiency is further supporting the expansion of the passenger car seat market in Asia Pacific.

Key companies operating in the Global Passenger Car Seat Market include Adient, Aisin Seiki, Faurecia, Grammer, Grupo Antolin, Johnson Controls, Lear, Magna International, RECARO Automotive, and Toyota Boshoku. Companies in the passenger car seat market are strengthening their competitive position through innovation, strategic partnerships, and global expansion initiatives. They are investing in advanced materials and smart technologies to enhance seating comfort, safety, and functionality. Close collaboration with automotive manufacturers allows companies to align product development with evolving vehicle architectures and consumer expectations. Market players are also expanding production capabilities and geographic presence to meet rising demand across key regions. Additionally, the integration of lightweight materials and sustainable manufacturing practices is becoming a priority to improve efficiency and reduce environmental impact. Continuous focus on research and development, along with improved supply chain management, is enabling companies to maintain a strong foothold in the competitive landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Seats

- 2.2.4 Vehicle

- 2.2.5 Material

- 2.2.6 Technology

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing global vehicle production and sales

- 3.2.1.2 Rising consumer demand for comfort and premium features

- 3.2.1.3 Increasing safety regulations and integrated safety systems

- 3.2.1.4 Shift toward electric vehicles driving lightweight seat designs

- 3.2.1.5 Technological advancements in smart and connected seating

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High raw material costs and supply chain volatility

- 3.2.2.2 Stringent emission and weight reduction mandates

- 3.2.2.3 Cost pressures from OEM consolidation and price negotiations

- 3.2.2.4 Complexity in multi-material integration and manufacturing

- 3.2.3 Market opportunities

- 3.2.3.1 Autonomous vehicle development creating new seating configurations

- 3.2.3.2 Growth in emerging markets with rising vehicle ownership

- 3.2.3.3 Sustainability trends driving eco-friendly material adoption

- 3.2.3.4 Aftermarket customization and personalization services

- 3.2.3.5 Integration of health and wellness features (massage, posture monitoring)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal Motor Vehicle Safety Standards (FMVSS) & NHTSA seating regulations

- 3.4.1.2 Canada - Transport Canada seat safety standards & crashworthiness regulations

- 3.4.2 Europe

- 3.4.2.1 Germany- ECE R17 seat strength & Euro NCAP crash test compliance

- 3.4.2.2 UK- Post-Brexit vehicle type approval for seating systems

- 3.4.2.3 France- Interior material safety & decarbonization requirements

- 3.4.2.4 Italy- Low-emission zone compliance & occupant protection regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China- GB/T and GB standards for seat safety & crashworthiness

- 3.4.3.2 India- AIS seat safety norms & Bharat NCAP compliance

- 3.4.3.3 Japan- Fuel efficiency-linked interior weight regulations & seat safety standards

- 3.4.3.4 Australia- ADR 4/05, ADR 7/00 standards & seatbelt integration norms

- 3.4.4 LATAM

- 3.4.4.1 Brazil- INMETRO seat safety certification & crash test requirements

- 3.4.4.2 Mexico- NOM-194-SCFI-2019 & USMCA compliance for automotive interiors

- 3.4.4.3 Argentina- Law 24.449 & updated seat safety and material regulations

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (seat safety amendments)

- 3.4.5.2 Saudi Arabia- Traffic law & Vision 2030 automotive interior initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9.3 Total cost of ownership (TCO) analysis

- 3.10 Trade data analysis (Driven by Paid Database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Use cases & success stories

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Raw material sourcing & supply security analysis

- 3.14.1 Critical material dependencies (foam, steel, leather, electronics)

- 3.14.2 Geographic concentration risk & supplier diversification

- 3.14.3 Price volatility trends & hedging strategies

- 3.15 Customer preference & buying behavior analysis

- 3.15.1 Feature prioritization by vehicle segment (economy vs. luxury)

- 3.15.2 Willingness-to-pay analysis for premium features

- 3.15.3 Regional preference variations

- 3.16 Sustainability and environmental aspects

- 3.16.1 Sustainable practices

- 3.16.2 Waste reduction strategies

- 3.16.3 Energy efficiency in production

- 3.16.4 Eco-friendly Initiatives

- 3.16.5 Carbon footprint considerations

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Standard seats

- 5.3 Luxury seats

- 5.4 Sports seats

Chapter 6 Market Estimates & Forecast, By Seat, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Front seats

- 6.3 Rear seats

- 6.4 Bucket seats

Chapter 7 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Fabric

- 7.3 Leather

- 7.4 Synthetic

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Standard/manual seats

- 8.3 Powered/electric seats

- 8.4 Smart/connected seats

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Sedan

- 9.3 SUV (Sport Utility Vehicle)

- 9.4 Hatchback

- 9.5 Luxury

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.3.9 Denmark

- 11.3.10 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Israel

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Adient

- 12.1.2 Aisin Seiki

- 12.1.3 Faurecia

- 12.1.4 Gentherm

- 12.1.5 Grammer

- 12.1.6 Grupo Antolin

- 12.1.7 Johnson Controls

- 12.1.8 Lear

- 12.1.9 Magna International

- 12.1.10 NHK Spring

- 12.1.11 Toyota Boshoku

- 12.2 Regional Players

- 12.2.1 Bharat Seats

- 12.2.2 Futuris

- 12.2.3 Haima

- 12.2.4 Harita Seating Systems

- 12.2.5 Summit Auto Seats

- 12.2.6 TACHI-S

- 12.3 Emerging Players

- 12.3.1 Brose Fahrzeugteile

- 12.3.2 RECARO Automotive Seating

- 12.3.3 Yanfeng Automotive Interiors