PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019099

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019099

Automotive Thermal System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

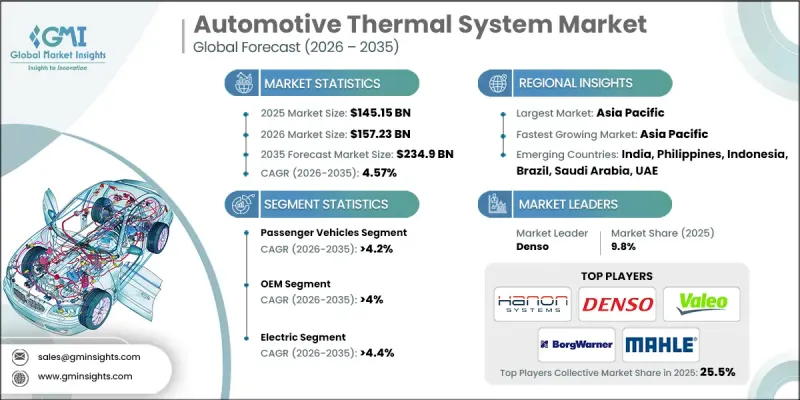

The Global Automotive Thermal System Market was valued at USD 145.15 billion in 2025 and is estimated to grow at a CAGR of 4.57% to reach USD 234.9 billion by 2035.

The automotive thermal system industry is undergoing a significant transformation, such as electrification, stricter emission regulations, and powertrain optimization, which redefine its role within modern vehicles. Thermal systems are no longer limited to conventional engine cooling and cabin climate control, but are now essential for battery efficiency, power electronics protection, passenger comfort, and overall vehicle performance across electric and hybrid platforms. As the global shift toward electrified mobility accelerates, thermal management solutions are becoming a key factor in improving driving range, enabling fast charging, enhancing durability, and reducing the total cost of ownership. Increasing production of electric vehicles, combined with tighter regulatory requirements and efficiency standards, is driving demand for advanced thermal technologies. Automakers are focusing on integrated systems that optimize energy use across the vehicle, incorporating innovations such as multi-circuit cooling, efficient heat exchange mechanisms, and advanced system design approaches that enhance performance while reducing energy losses.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $145.15 Billion |

| Forecast Value | $234.9 Billion |

| CAGR | 4.57% |

The passenger vehicles segment held a 72.4% share in 2025 and is projected to grow at a CAGR of 4.2% through 2035. This leadership position is supported by high global production volumes across vehicle categories and the rapid adoption of electrified passenger vehicles. Increasing demand for enhanced in-cabin comfort, improved energy efficiency, and extended driving range is driving the integration of advanced thermal management solutions. Regulatory pressure related to fuel efficiency and emissions is also encouraging the adoption of lightweight and highly integrated thermal system architectures in passenger vehicles.

The OEM segment held a 72% share in 2025 and is expected to grow at a CAGR of 4% from 2026 to 2035. This dominance is attributed to the complexity of integrating advanced thermal systems within modern vehicle platforms, particularly for electric and hybrid models. Thermal components are increasingly designed and optimized during the vehicle development stage, making original equipment manufacturers central to system implementation. Strong supply partnerships and large-scale vehicle platform development further reinforce the importance of OEM channels, while the aftermarket remains relatively limited due to the technical complexity of these systems.

China Automotive Thermal System Market held a 64.2% share, generating USD 37.3 billion in 2025. Growth in the region is driven by strong electric vehicle production and supportive policy frameworks promoting electrification. The rapid expansion of electric vehicle manufacturing has significantly increased demand for advanced thermal management systems. Government initiatives, sustainability goals, and strict efficiency regulations are accelerating the adoption of next-generation thermal technologies across both passenger and commercial vehicle segments.

Key companies operating in the Global Automotive Thermal System Market include Denso, Valeo, Mahle, Hanon Systems, BorgWarner, ZF, Marelli Holdings, Sanden, Gentherm, and Continental. Companies in the Automotive Thermal System Market are strengthening their competitive position through continuous innovation and strategic expansion. They are investing in advanced thermal technologies to improve energy efficiency, system integration, and overall vehicle performance. Firms are focusing on developing lightweight and compact solutions that align with evolving vehicle architectures. Strategic partnerships with automakers are enabling early-stage integration and long-term supply agreements. Companies are also enhancing research and development capabilities to support next-generation electrified platforms. In addition, they are expanding manufacturing capacity and optimizing global supply chains to meet rising demand, while leveraging digital tools and advanced engineering to improve system reliability and efficiency.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Propulsion

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in electric vehicle (EV) adoption and battery thermal management requirements

- 3.2.1.2 Rise in stringent global emission and energy efficiency regulations

- 3.2.1.3 Surge in demand for integrated thermal systems (HVAC + battery + power electronics)

- 3.2.1.4 Growth in electrified commercial and fleet vehicle deployments

- 3.2.1.5 Expansion in aftermarket thermal components and service demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High System Complexity & Cost

- 3.2.2.2 Limited Standardization & Fragmented Architectures

- 3.2.3 Market opportunities

- 3.2.3.1 Surge in demand for thermal solutions for fast-charging and high-voltage platforms

- 3.2.3.2 Increase in adoption of digital and AI-enabled thermal control systems

- 3.2.3.3 Rise in demand for sustainable refrigerants and low-GWP coolants

- 3.2.3.4 Growth in modular aftermarket repair and refurbishment services

- 3.2.3.5 Expansion in thermal solutions for emerging EV segments (two- & three-wheelers, off-road)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory guideline

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA Vehicle Emission & Fuel Efficiency Standards

- 3.4.1.2 Canada: Transport Canada Safety & Thermal Performance Standards

- 3.4.2 Europe

- 3.4.2.1 Germany: End-of-Life Vehicle (ELV) Directive

- 3.4.2.2 UK: Zero Emission Vehicle (ZEV) Mandate

- 3.4.2.3 France: Energy Transition Law

- 3.4.2.4 Italy: National Energy & Climate Plan (PNIEC) Alignment

- 3.4.3 Asia Pacific

- 3.4.3.1 China: NEV Mandate & Dual Credit Policy

- 3.4.3.2 India: FAME II & PLI Scheme for Auto Components

- 3.4.3.3 Japan: Green Growth Strategy & JEVS Standards

- 3.4.3.4 Australia: National Electric Vehicle Strategy

- 3.4.4 Latin America

- 3.4.4.1 Brazil: Rota 2030 Program

- 3.4.4.2 Mexico: USMCA Localization Requirements

- 3.4.4.3 Argentina: National Sustainable Mobility Policies

- 3.4.5 MEA

- 3.4.5.1 UAE: Net Zero 2050 Strategy & EV Infrastructure Expansion

- 3.4.5.2 Saudi Arabia: Vision 2030 & EV Localization Strategy

- 3.4.5.3 South Africa: Green Transport Strategy

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Trade statistics (Driven by Paid Database)

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.14.2.1 Predictive Thermal Modeling & Temperature Profile Optimization

- 3.14.2.2 AI-Enabled Fast Charging Thermal Management

- 3.14.2.3 Real-Time Adaptive Cooling Strategies for Battery Longevity

- 3.14.2.4 Autonomous Vehicle Thermal Load Prediction

- 3.14.3 Risks, Limitations & Regulatory Considerations

- 3.15 Investment & Funding Analysis

- 3.15.1 VC & PE Investments in Thermal Technology Startups

- 3.15.2 OEM R&D Spending on Thermal Management

- 3.15.3 Government Grants & Subsidies for Green Refrigerants

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Compressor

- 5.3 Heat Exchanger

- 5.4 Electric Pump

- 5.5 Electric Fan

- 5.6 Thermoelectric Module

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light-duty

- 6.3.2 Medium-duty

- 6.3.3 Heavy-duty

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Powertrain Cooling

- 9.3 HVAC

- 9.4 Battery Thermal Management

- 9.5 Waste Heat Recovery

- 9.6 Seat Heating & Cooling

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BorgWarner

- 11.1.2 Continental

- 11.1.3 Denso

- 11.1.4 Hanon Systems

- 11.1.5 MAHLE

- 11.1.6 Marelli

- 11.1.7 Sanden

- 11.1.8 Schaeffler

- 11.1.9 Valeo

- 11.1.10 Webasto

- 11.2 Regional Players

- 11.2.1 Dana

- 11.2.2 Eberspacher

- 11.2.3 ESTRA Automotive Systems

- 11.2.4 Grayson Thermal Systems

- 11.2.5 PWR

- 11.2.6 Sanhua Automotive

- 11.2.7 Senior

- 11.2.8 Subros

- 11.2.9 T.RAD

- 11.2.10 Yinlun

- 11.3 Emerging Players

- 11.3.1 Boyd

- 11.3.2 Gentherm

- 11.3.3 Modine Manufacturing

- 11.3.4 XING Mobility

- 11.3.5 ZF