PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019101

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019101

Impact Resistant Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

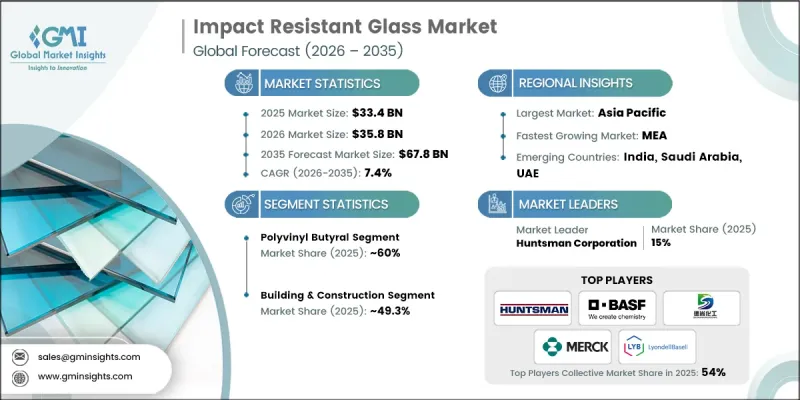

The Global Impact Resistant Glass Market was valued at USD 33.4 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 67.8 billion by 2035.

The market is gaining strong momentum due to accelerating urbanization and increasing construction activity, which are driving demand for high-performance building materials. Growing emphasis on structural safety, durability, and energy efficiency is encouraging the adoption of laminated and advanced safety glass solutions in modern architecture. In parallel, the automotive sector is contributing significantly to market growth, with rising demand for enhanced safety, comfort, and advanced glazing systems. Regulatory frameworks focused on crash safety and building resilience are further reinforcing adoption across key regions. Additionally, climate-related risks and the need for disaster-resistant infrastructure are pushing demand for robust glazing solutions. The integration of smart glass technologies and multifunctional performance features, such as acoustic insulation, solar control, and UV protection, is transforming product capabilities. These evolving requirements are positioning impact resistant glass as a critical component across construction, automotive, and infrastructure applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $33.4 Billion |

| Forecast Value | $67.8 Billion |

| CAGR | 7.4% |

The polyvinyl butyral segment accounted for 60% share in 2025, making it the dominant interlayer material in impact resistant glass. Its widespread use is supported by strong processing capabilities and compatibility with both architectural and automotive applications. At the same time, increasing demand for enhanced structural performance and safety is encouraging the adoption of advanced interlayer materials, particularly in applications requiring higher strength and durability.

The building and construction segment held a 49.3% share in 2025, driven by strict safety regulations and the ongoing modernization of building facades. Laminated glass solutions are increasingly being used across structural applications where safety and resilience are critical. Demand is further supported by growing adoption in transportation applications, where enhanced safety and comfort features are becoming standard requirements.

North America Impact Resistant Glass Market is projected to reach USD 16.4 billion by 2035. Growth in the region is supported by stringent building codes, increasing focus on resilient construction practices, and strong demand from the automotive sector. Retrofit activities and infrastructure upgrades are also contributing to sustained market expansion.

Key players operating in the Global Impact Resistant Glass Market include Saint-Gobain, AGC, Guardian Industries, Nippon Sheet Glass, Pilkington, SCHOTT, Corning, Central Glass Company, Cardinal Glass, CGS Holding, Fuyao Glass Industry Group, Sekurit, Vitro, Xinyi Glass, and Qingdao Kangdeli Industrial. Companies in the Global Impact Resistant Glass Market are focusing on innovation and strategic expansion to strengthen their competitive position. Investments in advanced interlayer technologies and smart glass integration are enabling multifunctional product offerings. Firms are expanding manufacturing capabilities and enhancing supply chain networks to meet growing global demand. Strategic collaborations with construction firms, automotive manufacturers, and technology providers are supporting product development and market penetration. Additionally, companies are prioritizing sustainable production practices and compliance with evolving safety regulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Interlayer

- 2.2.3 End Use Industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Strong building and safety code enforcement

- 3.2.1.2 Growth in EVs and panoramic vehicle glazing

- 3.2.1.3 Climate resilience and disaster-prone construction

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital, processing, and certification costs

- 3.2.2.2 Weak retrofit spending in developing economies

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of smart and multifunctional glazing

- 3.2.3.2 Green building and net-zero construction trends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Interlayer

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code: 700721)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Interlayer, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyvinyl butyral

- 5.3 Ionoplast polymer

- 5.4 Ethylene vinyl acetate

- 5.5 Others

- 5.6 Interlayer

- 5.7 End Use Industry

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Building & Construction

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Public / Institutional

- 6.2.4 Balustrades & Overhead Glazing

- 6.3 Automotive & Transportation

- 6.3.1 Passenger Vehicles

- 6.3.2 Commercial Vehicles

- 6.3.3 Rail & Marine

- 6.4 Security & Defense

- 6.4.1 Banks & Sensitive Facilities

- 6.4.2 High-Security Sites

- 6.5 Industrial & Infrastructure

- 6.5.1 Industrial Plants

- 6.5.2 Critical Infrastructure

- 6.5.3 Transport Infrastructure

- 6.6 Specialty & Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 AGC

- 8.2 Cardinal Glass

- 8.3 Central Glass Company

- 8.4 CGS Holding

- 8.5 Corning

- 8.6 Fuyao Glass Industry Group

- 8.7 Guardian Industries

- 8.8 Nippon Sheet Glass

- 8.9 Pilkington

- 8.10 Qingdao Kangdeli Industrial

- 8.11 Saint-Gobain

- 8.12 SCHOTT

- 8.13 Sekurit

- 8.14 Vitro

- 8.15 Xinyi Glass