PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019121

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019121

Defibrillators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

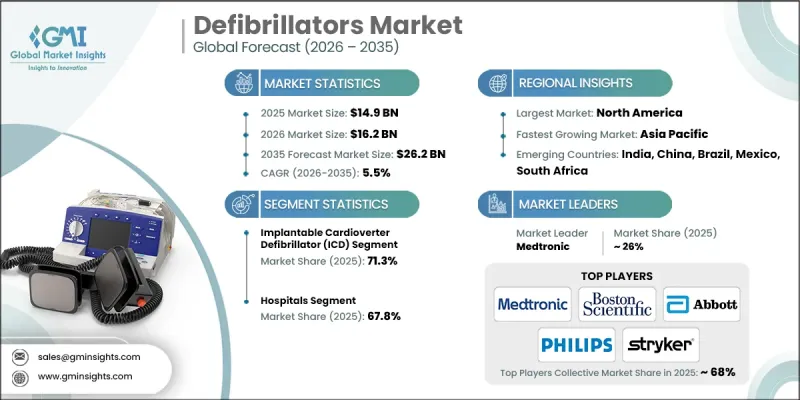

The Global Defibrillators Market was valued at USD 14.9 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 26.2 billion by 2035.

The market growth is driven by the rising prevalence of cardiovascular diseases, increasing incidents of sudden cardiac arrest, an expanding geriatric population, and continuous advancements in defibrillator technology. Defibrillators deliver controlled electrical shocks to restore normal heart rhythm in life-threatening arrhythmias and are deployed in hospitals, emergency care, public locations, and implantable devices. Manufacturers are innovating with wireless-enabled devices, real-time patient monitoring, automated shock delivery, and integration with emergency response systems. Portable, user-friendly automated external defibrillators (AEDs) allow even untrained bystanders to provide timely assistance. Wearable defibrillators are gaining traction by offering continuous monitoring and immediate intervention for high-risk patients, improving mobility and safety while bridging the gap before implantable solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.9 Billion |

| Forecast Value | $26.2 Billion |

| CAGR | 5.5% |

The implantable cardioverter defibrillator (ICD) segment held a 71.3% share in 2025, driven by widespread clinical adoption for managing life-threatening arrhythmias, high physician preference, and rising ventricular tachycardia and fibrillation cases. ICDs automatically detect abnormal heart rhythms and deliver corrective shocks, making them essential for long-term cardiac management.

The hospitals segment accounted for 67.8% share in 2025 and is expected to reach USD 18 billion, supported by advanced defibrillator availability, skilled staff, complex cardiac patient care, and digital health technologies enabling remote monitoring and timely alerts.

North America Defibrillators Market held a 37.3% share in 2025 owing to a high incidence of cardiovascular diseases, sedentary lifestyles, obesity, and related comorbidities. The prevalence of out-of-hospital cardiac events has fueled demand for AEDs and ICDs. The region hosts leading defibrillator manufacturers that heavily invest in research, product development, and commercialization. Strategic collaborations with healthcare providers, ongoing product launches, and continuous technological upgrades enhance accessibility and adoption across the region.

Prominent players in the Global Defibrillators Market include Abbott, Amiitalia, Asahi KASEI, BIOTRONIK, Boston Scientific, BPL Medical Technologies, CU MEDICAL, MEDITECH, Medtronic, MicroPort, Mindray, NIHON KOHDEN, Philips, SCHILLER, and Stryker. Companies in the Global Defibrillators Market strengthen their position by investing in R&D for advanced, reliable, and connected devices, expanding product portfolios to include portable, wearable, and implantable solutions. They form partnerships with hospitals, emergency services, and distribution networks to improve reach and adoption. Focused marketing campaigns, clinical validation studies, and training programs for healthcare professionals reinforce product credibility. Regional expansion strategies target high-risk patient populations while maintaining compliance with local regulatory standards. Continuous innovation, cost optimization, and integration of AI-enabled monitoring and telehealth platforms enhance customer satisfaction, brand loyalty, and market foothold.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases and sudden cardiac arrest

- 3.2.1.2 Technological advancements in implantable and automated defibrillators

- 3.2.1.3 Increasing awareness and training programs for CPR and AED usage

- 3.2.1.4 Growing adoption of portable and user-friendly AED devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of defibrillator devices and maintenance

- 3.2.2.2 Product recalls and safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of defibrillator deployment in emerging markets

- 3.2.3.2 Development of wearable cardioverter-defibrillators

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Customer insights (Driven by primary research)

- 3.11 Start-up scenarios (Driven by primary research)

- 3.12 Investment landscape (Driven by primary research)

- 3.13 Pipeline products (Driven by primary research)

- 3.14 Indication landscape

- 3.14.1 Implantable cardioverter defibrillators (ICDs)

- 3.14.2 Wearable external cardioverter defibrillators (WCDs)

- 3.15 Value chain analysis

- 3.16 Pricing analysis, 2025 (Driven by primary research)

- 3.17 Impact of AI and its future assessment

- 3.18 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Implantable cardioverter defibrillator (ICD)

- 5.2.1 Transvenous implantable cardioverter defibrillator

- 5.2.1.1 Dual-chamber ICDs

- 5.2.1.2 Single-chamber ICDs

- 5.2.2 Subcutaneous implantable cardioverter defibrillator

- 5.2.1 Transvenous implantable cardioverter defibrillator

- 5.3 External cardioverter defibrillator

- 5.3.1 Manual ED

- 5.3.2 Automated ED

- 5.3.2.1 Semi-automated external defibrillator

- 5.3.2.2 Fully automated external defibrillator

- 5.3.3 Wearable cardioverter defibrillator

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Amiitalia

- 8.3 Asahi KASEI

- 8.4 BIOTRONIK

- 8.5 Boston Scientific

- 8.6 BPL Medical Technologies

- 8.7 CU MEDICAL

- 8.8 MEDITECH

- 8.9 Medtronic

- 8.10 MicroPort

- 8.11 Mindray

- 8.12 NIHON KOHDEN

- 8.13 Philips

- 8.14 SCHILLER

- 8.15 Stryker