PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019124

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019124

Tacrolimus Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

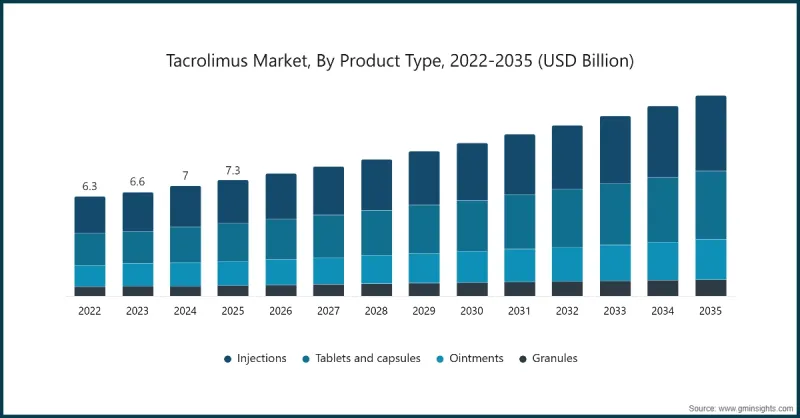

The Global Tacrolimus Market was valued at USD 7.3 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 12.7 billion by 2035.

The tacrolimus market is expanding due to the rising number of organ transplant procedures and the growing burden of autoimmune disorders worldwide. Increasing cases of end-stage organ failure, along with improved awareness of organ donation and advancements in surgical techniques, are contributing to higher transplant volumes, thereby driving demand for immunosuppressive therapies. In addition, the growing prevalence of chronic inflammatory and autoimmune conditions is increasing the need for long-term treatment options. Tacrolimus plays a crucial role in suppressing immune responses by inhibiting calcineurin activity, preventing damage to healthy tissues. Advancements in immunosuppressive drug development and the increasing use of topical formulations for dermatological conditions are further supporting market growth. Continuous investment in research and development, along with improved access to healthcare services, is also strengthening the adoption of tacrolimus-based therapies across global healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.3 Billion |

| Forecast Value | $12.7 Billion |

| CAGR | 5.6% |

The injections segment accounted for 37.5% share in 2025, supported by its critical role in post-transplant care. Injectable tacrolimus is widely utilized during the immediate postoperative period when rapid and controlled immunosuppression is required. This form is particularly important for patients who are unable to take oral medications, ensuring consistent therapeutic delivery. The ability to precisely manage dosage levels in acute care environments further supports the segment's growth, especially as investments in transplant medicine continue to rise.

The hospitals segment held a 54.4% share in 2025, driven by their capacity to manage complex medical conditions and provide specialized care. Hospitals are central to transplant procedures and the management of complications, including acute rejection episodes. Access to skilled healthcare professionals, advanced treatment infrastructure, and supportive care services ensures effective administration and monitoring of tacrolimus therapy. Additionally, hospitals play a significant role in clinical research and trials, further increasing the use of tacrolimus in controlled treatment settings.

North America Tacrolimus Market accounted for 40.4% share in 2025. The region benefits from advanced healthcare infrastructure, including specialized transplant centers and well-equipped hospitals. High levels of healthcare spending and widespread insurance coverage improve patient access to immunosuppressive therapies. These factors, combined with ongoing research and strong clinical adoption, are supporting sustained demand for tacrolimus across the region.

Key companies operating in the Global Tacrolimus Market include Astellas Pharma Inc., Novartis, Pfizer Inc., Abbott Laboratories, Takeda Pharmaceutical Company Limited, F. Hoffmann-La Roche Ltd, GlaxoSmithKline plc, Viatris Inc., Lupin Pharmaceuticals Ltd, Glenmark Pharmaceuticals Ltd., and Biocon Ltd. Companies in the Global Tacrolimus Market are focusing on strategic initiatives to strengthen their market position and expand their global footprint. Investments in research and development are enabling the introduction of improved formulations, including extended-release and topical variants, to enhance patient compliance and therapeutic outcomes. Companies are also expanding their presence in emerging markets to tap into growing healthcare demand. Strategic collaborations with healthcare providers and research institutions support innovation and clinical advancements. Additionally, firms are optimizing manufacturing processes and supply chains to ensure consistent product availability. Emphasis on regulatory approvals, competitive pricing strategies, and patient awareness programs further helps companies maintain market share and drive long-term growth.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of organ transplant procedures

- 3.2.1.2 Rising prevalence of autoimmune diseases

- 3.2.1.3 Surge in immunosuppressive research and development activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of tacrolimus therapy

- 3.2.2.2 Side effects and the availability of the alternative treatments

- 3.2.3 Opportunities

- 3.2.3.1 Development of extended-release formulations

- 3.2.3.2 Growing demand for dermatology applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Patent landscape (Driven by Primary Research)

- 3.8 Impact of AI & generative AI on the market (Driven by Primary Research)

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 GenAI use cases & adoption roadmap by segment

- 3.9 Treatment infrastructure & clinical adoption landscape (Driven by Primary Research)

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Injections

- 5.3 Tablets and capsules

- 5.4 Ointments

- 5.5 Granules

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dermatitis

- 6.3 Immunosuppression

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Astellas Pharma Inc.

- 9.3 Biocon Ltd.

- 9.4 F. Hoffmann-La Roche Ltd

- 9.5 Glenmark Pharmaceuticals Ltd.

- 9.6 GlaxoSmithKline plc

- 9.7 Lupin Pharmaceuticals Ltd

- 9.8 Novartis

- 9.9 Pfizer Inc.

- 9.10 Takeda Pharmaceutical Company Limited

- 9.11 Viatris Inc.