PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019125

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019125

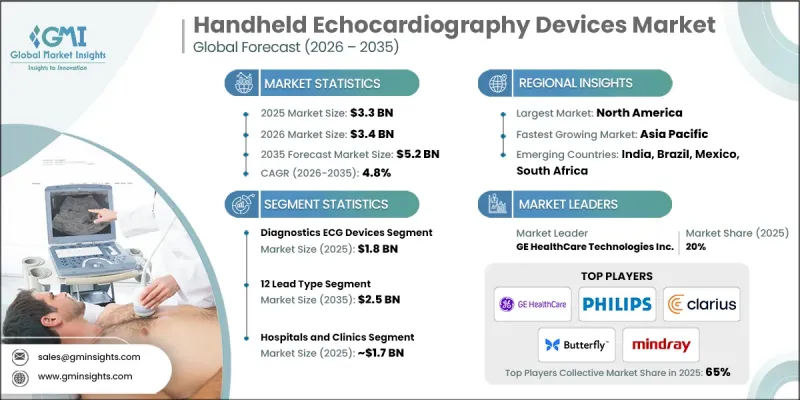

Handheld Echocardiography Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Handheld Echocardiography Devices Market was valued at USD 3.3 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 5.2 billion by 2035.

The growth is driven by the rising demand for remote patient monitoring, advancements in echocardiography technology, an increasing prevalence of cardiovascular diseases, and the expanding aging population, along with growing home healthcare adoption. Handheld echocardiography devices have become essential tools in modern medicine, providing real-time cardiac imaging at the point of care. They enable rapid screening, early disease detection, clinical triage, and treatment monitoring across hospitals, outpatient clinics, primary care centers, emergency departments, and underserved areas. The market is propelled by technological innovations, including enhanced image quality, miniaturized designs, extended battery life, wireless transmission, and integration of artificial intelligence for image interpretation. These advances improve diagnostic confidence, streamline workflows, and enhance user experience, encouraging wider adoption in clinical and home care settings. Portable, lightweight, and battery-operated, these devices allow clinicians to capture cardiac structure, function, and blood flow images efficiently on-site.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.3 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 4.8% |

The diagnostics ECG devices segment accounted for USD 1.8 billion in 2025, leading the market due to its non-invasive, rapid, and accessible cardiac imaging capabilities. These devices reduce dependence on traditional cart-based scanners and speed up clinical decision-making. Technological improvements, including compact transducers, wireless connectivity, and app-based workflows, have enhanced usability and facilitated integration into decentralized healthcare settings, expanding adoption across point-of-care and home monitoring models.

The hospitals and clinics segment generated USD 1.7 billion in 2025. This segment includes public and private hospitals, cardiac care centers, outpatient clinics, and emergency departments where handheld echocardiography devices are used for bedside assessments. These devices enable clinicians to quickly evaluate cardiac structure and function during routine check-ups, emergencies, and follow-up visits without relying on large stationary systems. High patient volumes and the growing need for rapid diagnosis and workflow efficiency contribute to the dominance of this segment.

North America Handheld Echocardiography Devices Market held a 33.6% share in 2025. The region's strong market share is attributed to the high prevalence of cardiovascular diseases and the rising need for rapid, point-of-care cardiac evaluations in hospitals, outpatient clinics, and emergency care settings. A well-established healthcare infrastructure, early adoption of portable imaging technologies, and the presence of major medical device manufacturers accelerate market growth. The North American healthcare ecosystem supports early diagnosis, timely interventions, and widespread adoption of innovative handheld echocardiography solutions.

Key players operating in the Global Handheld Echocardiography Devices Market include AliveCor, Inc., Biotronik SE & Co. KG, Boston Scientific Corporation, Butterfly Network, CHISON, Clarius, EchoNous Inc., Esaote S.p.A., Exo Imaging, Inc., Fukuda Denshi Co., Ltd., GE HealthCare Technologies Inc., Hill-Rom Holdings, Inc., Koninklijke Philips N.V., Medtronic plc, and Shenzhen Mindray Bio-Medical Electronics Co., Ltd. Companies in the Handheld Echocardiography Devices Market are adopting several strategies to strengthen their market position. They are investing in research and development to create compact, AI-integrated, and wireless-enabled devices that enhance diagnostic accuracy and ease of use. Strategic partnerships with hospitals, clinics, and telehealth providers expand product reach and ensure integration into point-of-care workflows. Firms are also entering emerging markets to tap into growing home healthcare and remote monitoring demand. Additionally, companies focus on training programs for healthcare professionals, digital marketing campaigns, and service support infrastructure to improve adoption rates.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Lead type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for remote patient monitoring

- 3.2.1.2 Advancements in echocardiography technology

- 3.2.1.3 Rising cardiovascular disease incidence

- 3.2.1.4 Increasing aging population and home healthcare trends

- 3.2.2 Industry Pitfalls and Challenges:

- 3.2.2.1 Regulatory compliance and standardization

- 3.2.2.2 Limited diagnostic capability compared to traditional ECG systems

- 3.2.3 Market Opportunities

- 3.2.3.1 Rising adoption in emerging markets

- 3.2.3.2 Expansion of point-of-care diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by Primary Research)

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostics ECG devices

- 5.2.1 Resting ECG

- 5.2.2 Stress ECG

- 5.3 Monitoring ECG devices

- 5.3.1 Holter monitors

- 5.3.2 Mobile cardiac telemetry (MCT)

- 5.3.3 Wearable ECG devices

- 5.3.4 Other monitoring ECG devices

Chapter 6 Market Estimates and Forecast, By Lead Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Single lead type

- 6.3 3 lead type

- 6.4 6 lead type

- 6.5 12 lead type

- 6.6 Other lead types

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Diagnostic centers

- 7.4 Ambulatory surgical centers

- 7.5 Home care settings

- 7.6 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AliveCor, Inc.

- 9.2 Biotronik SE & Co. KG

- 9.3 Boston Scientific Corporation

- 9.4 Butterfly Network

- 9.5 CHISON

- 9.6 Clarius

- 9.7 EchoNous Inc.

- 9.8 Esaote S.p.A.

- 9.9 Exo Imaging, Inc.

- 9.10 Fukuda Denshi Co., Ltd.

- 9.11 GE HealthCare Technologies Inc.

- 9.12 Hill-Rom Holdings, Inc.

- 9.13 Koninklijke Philips N.V.

- 9.14 Medtronic plc

- 9.15 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.