PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019141

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019141

Dairy Packaging Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

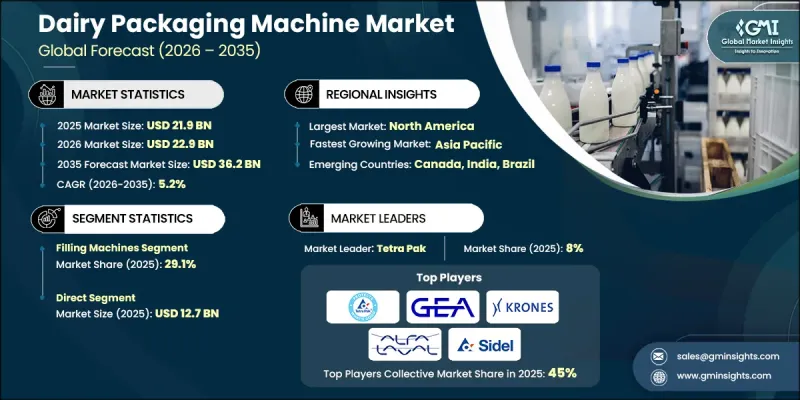

The Global Dairy Packaging Machine Market was valued at USD 21.9 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 36.2 billion by 2035.

The rapid adoption of dairy packaging machines is being driven by ongoing innovations in automation, smart manufacturing systems, and food safety technologies. Manufacturers are increasingly shifting from manual to fully automated and digitally integrated packaging solutions, reflecting the industry's focus on efficiency, precision, and traceability. Consolidation between hardware and software providers has further reinforced the adoption of turnkey solutions that integrate processing, quality inspection, and production monitoring. Modern dairy packaging machines are designed for high flexibility, allowing seamless format changes, multi-product handling, and reduced downtime. Cutting-edge technologies, including AI-enabled quality control, predictive maintenance, machine vision systems, and IoT-driven asset management, are enhancing operational performance while ensuring compliance with stringent safety and hygiene standards. The adoption of digital twin technologies is enabling real-time monitoring, operational simulation, and process optimization, further supporting sustained market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.9 Billion |

| Forecast Value | $36.2 Billion |

| CAGR | 5.2% |

In 2025, the filling machines segment held 29.1% share, valued at USD 6.4 billion. Filling machines are critical in primary packaging due to their high-speed performance, volumetric and gravimetric accuracy, and compatibility with a variety of dairy products, including milk, yogurt, and cream. Automation of filling and sealing operations allows for centralized quality oversight, enabling operators to monitor multiple production lines through digital dashboards and make real-time adjustments. This reduces product waste, shortens changeover times, and ensures consistent output quality, which is a key driver of growth. The integration of AI and vision systems enhances precision, enabling defect detection and adherence to regulatory standards, which strengthens operational efficiency and minimizes production losses.

The direct sales segment is projected to grow at a CAGR of 5.3% through 2035. This segment remains the preferred choice for large-scale industrial processors and multinational dairy corporations. Growth is supported by the rising demand for comprehensive turnkey solutions, direct technical consultations with OEMs, dedicated after-sales support, and operator training programs. Direct engagement allows manufacturers to offer tailored installation services, long-term maintenance agreements, and ongoing system upgrades, which ensure operational reliability and reduce downtime. Companies providing on-site support and customized technical solutions continue to gain the trust of industrial and commercial dairy producers seeking maximum efficiency and system flexibility.

United States Dairy Packaging Machine Market held a 75.3% share in 2025. Market dominance is fueled by a high concentration of large dairy cooperatives, stringent food safety and hygiene regulations, and increasing demand for extended shelf-life packaging solutions. The region is witnessing accelerated adoption of automated, traceability-enabled production lines and advanced packaging systems for milk, cheese, yogurt, and other dairy products. Growing emphasis on sustainability and waste reduction, combined with investments in smart manufacturing technologies, further drives market growth. Advanced packaging solutions, including aseptic filling systems, multi-format line flexibility, and AI-driven monitoring, are increasingly deployed to meet evolving consumer expectations for freshness, quality, and safety.

Major companies operating in the Global Dairy Packaging Machine Market include Alfa Laval AB, Barry-Wehmiller, Carpigiani Group, Elopak, GEA Group, Greatview Aseptic Packaging, IMA Group, Krones AG, Scherjon Dairy Equipment, Scholle IPN (SIG), Sidel, SIG Combibloc, SPX Flow (ITT), Syntegon, Technogel S.p.A., and Tetra Pak. These players are driving innovation, expanding their product portfolios, and enhancing global reach to cater to increasing demand for automated, flexible, and smart dairy packaging solutions. Key strategies adopted by companies in the Dairy Packaging Machine Market include continuous investment in research and development to improve automation, digitalization, and AI-driven inspection technologies. Firms are forming strategic alliances with software and IoT providers to deliver integrated turnkey solutions and smart factory capabilities. Expanding after-sales service networks, including on-site maintenance, operator training, and predictive support, strengthens customer trust and operational reliability. Companies are also focusing on multi-format packaging capabilities, energy-efficient designs, and sustainable material usage to appeal to environmentally conscious dairy producers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Packaging Type

- 2.2.4 Operation

- 2.2.5 Application

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aseptic & extended shelf life

- 3.2.1.2 Labor shortages & reshoring

- 3.2.1.3 Smart Packaging & Iot Integration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial capex

- 3.2.2.2 Increasing sustainability compliance

- 3.2.3 Opportunities

- 3.2.3.1 Increasing growth of modular "micro-dairy" units

- 3.2.3.2 Growth in smart "self-cleaning" systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Print Management & Predictive Maintenance

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Infrastructure & Deployment Landscape (Driven by Primary Research)

- 3.12.1 Deployment Penetration by Region & Buyer Segment (Driven by Primary Research)

- 3.12.2 Scalability Constraints & Infrastructure Investment Trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Filling Machines

- 5.3 Form-Fill-Seal (FFS) Machines

- 5.4 Palletizing Machines

- 5.5 Wrapping Machines

- 5.6 Cartoning Machines

- 5.7 Labeling Machines

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Packaging Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Flexible

- 6.3 Rigid

Chapter 7 Market Estimates & Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Automatic

- 7.3 Semi-automatic

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Milk

- 8.3 Fresh Dairy Products

- 8.4 Butter & Buttermilk

- 8.5 Milk Powder

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Barry-Wehmiller

- 11.2 Carpigiani Group

- 11.3 Elopak

- 11.4 GEA Group

- 11.5 Greatview Aseptic Packaging

- 11.6 IMA Group

- 11.7 Krones AG

- 11.8 Scherjon Dairy Equipment

- 11.9 Scholle IPN (SIG)

- 11.10 Sidel

- 11.11 SIG Combibloc

- 11.12 SPX Flow (ITT)

- 11.13 Syntegon

- 11.14 Technogel S.p.A.

- 11.15 Tetra Pak