PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019146

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019146

Aircraft Fuel System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

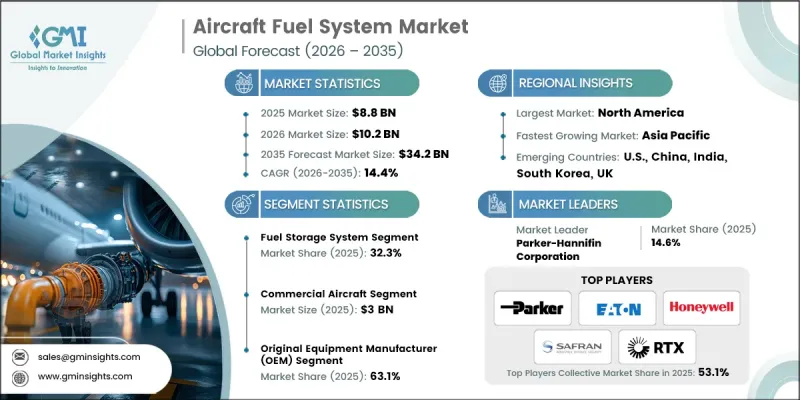

The Global Aircraft Fuel System Market was valued at USD 8.8 billion in 2025 and is estimated to grow at a CAGR of 14.4% to reach USD 34.2 billion by 2035.

The aircraft fuel system market is advancing rapidly as the aviation industry undergoes a large-scale transformation driven by rising air travel demand and increasing aircraft production. Growing passenger traffic is pushing airlines to expand their fleets while simultaneously replacing older aircraft with more efficient models, which is significantly boosting demand for advanced fuel systems. These systems are essential for optimizing fuel storage, transfer, and monitoring functions while improving overall aircraft performance and operational safety. In parallel, defense sector investments in fleet modernization are strengthening the need for highly reliable and technologically advanced fuel management solutions. The integration of lightweight materials and intelligent fuel system technologies is further enhancing fuel efficiency and reducing overall aircraft weight. Continuous innovation in fuel system design, along with the adoption of digital monitoring and control capabilities, is shaping the future of aviation operations. As global aviation activity continues to rise, the aircraft fuel system market is expected to maintain strong growth momentum supported by technological advancements and increasing production volumes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.8 Billion |

| Forecast Value | $34.2 Billion |

| CAGR | 14.4% |

The aircraft fuel system market continues to gain traction due to the steady rise in aircraft manufacturing output and substantial order pipelines across the aviation sector. Airlines are actively expanding operational capacity to accommodate increasing travel demand, which directly influences the need for efficient and reliable fuel system components. Additionally, the ongoing replacement cycle of aging aircraft is encouraging the adoption of next-generation systems that offer improved fuel efficiency and safety performance. Defense investments are also playing a critical role, as governments continue to enhance their aerial capabilities through modernization initiatives. This dual demand from the commercial and military sectors is reinforcing long-term market growth and technological advancement.

The fuel storage system segment accounted for 32.3% share in 2025, maintaining a leading position due to its essential role in ensuring safe and efficient fuel containment. These systems are fundamental in maintaining fuel quality, preventing leakage, and enabling accurate fuel level tracking during operations. Their integration is crucial for meeting strict aviation safety standards and supporting aircraft designed for extended operational ranges. Increasing demand for high-capacity and fuel-efficient aircraft is further strengthening the adoption of advanced storage solutions, contributing to the segment's continued dominance.

The commercial aircraft segment reached USD 3 billion in 2025, driven by the extensive global fleet size and consistent growth in airline operations. Commercial aviation requires highly efficient fuel systems capable of supporting long-duration flights and frequent usage cycles. The steady increase in aircraft deliveries, coupled with rising passenger volumes, continues to generate strong demand for sophisticated fuel management technologies. These systems play a vital role in improving operational efficiency, reducing fuel consumption, and enhancing overall flight performance, making them indispensable for modern commercial aviation.

North America Aircraft Fuel System Market held a 36.3% share in 2025, supported by a well-established aerospace manufacturing ecosystem and strong defense aviation investments. The region benefits from continuous advancements in aircraft technology and a high concentration of production activities, which drive demand for advanced fuel system components. Increasing focus on developing next-generation aircraft and upgrading existing fleets is further supporting market expansion. Additionally, the need for reliable and high-performance fuel systems to meet operational and regulatory requirements is reinforcing steady growth across the region.

Prominent players in the Global Aircraft Fuel System Market include Crane Aerospace & Electronics, Eaton Corporation, GE Aerospace, GKN Aerospace, Honeywell International Inc., Marshall Aerospace and Defence Group, Meggitt PLC, Parker-Hannifin Corporation, Robert Bosch GmbH, RTX Corporation, Safran S.A., Secondo Mona S.p.A., Trelleborg AB, Triumph Group Inc., and Woodward Inc. Companies in the Global Aircraft Fuel System Market are focusing on innovation, strategic partnerships, and global expansion to strengthen their competitive position. Significant investments are being made in research and development to introduce lightweight, energy-efficient, and digitally integrated fuel systems. Collaborations with aircraft manufacturers and defense organizations are enabling companies to align product offerings with evolving industry requirements. Market participants are also expanding their geographic presence through mergers, acquisitions, and partnerships to capture emerging opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Component type trends

- 2.2.3 Aircraft type trends

- 2.2.4 End-use trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising commercial aircraft production and backlog deliveries

- 3.2.1.2 Increasing global air passenger traffic growth

- 3.2.1.3 Military aircraft fleet modernization programs

- 3.2.1.4 Demand for lightweight fuel system components

- 3.2.1.5 Growth in long-range and wide-body aircraft demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High maintenance and system integration costs

- 3.2.2.2 Strict aviation fuel safety certification regulations

- 3.2.3 Market opportunities

- 3.2.3.1 High maintenance and system integration costs

- 3.2.3.2 Strict aviation fuel safety certification regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Fuel storage system

- 5.3 Fuel feed system

- 5.4 Fuel transfer system

- 5.5 Fuel inerting system

- 5.6 Fuel measurement & management system

Chapter 6 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Fuel tanks

- 6.3 Fuel pumps

- 6.4 Fuel valves

- 6.5 Fuel filters & strainers

- 6.6 Fuel sensors & gauges

- 6.7 Fuel control & monitoring units

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Commercial aircraft

- 7.3 Military aircraft

- 7.4 Business & general aviation aircraft

- 7.5 Helicopters

- 7.6 Unmanned aerial vehicles (UAVs)

Chapter 8 Market Estimates and Forecast, By End-Use, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Original equipment manufacturer (OEM)

- 8.3 Aftermarket

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Honeywell International Inc.

- 10.1.2 Safran S.A.

- 10.1.3 RTX Corporation

- 10.1.4 GE Aerospace

- 10.1.5 Parker-Hannifin Corporation

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Crane Aerospace & Electronics

- 10.2.1.2 Triumph Group Inc.

- 10.2.1.3 Woodward Inc.

- 10.2.1.4 Eaton Corporation

- 10.2.2 Asia Pacific

- 10.2.2.1 Robert Bosch GmbH

- 10.2.3 Europe

- 10.2.3.1 GKN Aerospace

- 10.2.3.2 Meggitt PLC

- 10.2.3.3 Trelleborg AB

- 10.2.3.4 Secondo Mona S.p.A.

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Marshall Aerospace and Defence Group