PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019151

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019151

Advanced Public Transportation System (APTS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

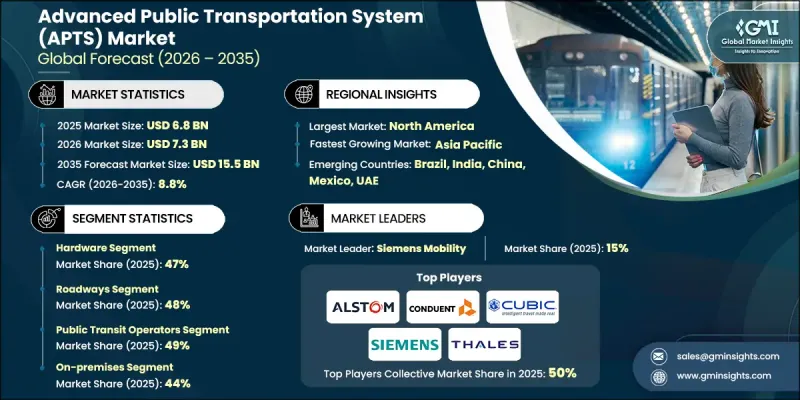

The Global Advanced Public Transportation System (APTS) Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 15.5 billion by 2035.

Market expansion is fueled by the increasing integration of intelligent technologies, including real-time passenger information, automated fare collection, and fleet management solutions, which collectively transform transit networks into data-driven ecosystems. These systems combine hardware, software, and services to enhance service reliability, operational efficiency, and overall passenger experience across buses, rail, and other public transit modes. Urbanization, regulatory mandates, and investments in digital infrastructure are accelerating adoption, as transit agencies aim to unify diverse assets under centralized control. Cloud-native, API-first platforms are gaining traction for their scalability and ability to support multimodal networks without costly infrastructure overhauls. North America leads the market, driven by early adoption of mobility-as-a-service solutions, federal funding support, and a mature ecosystem of vendors and integrators investing in AI-enabled transit operations, open payment standards, and intelligent transit analytics.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $15.5 Billion |

| CAGR | 8.8% |

The hardware segment held a 47% share in 2025 and is expected to grow at a CAGR of 8% through 2035. This segment includes ticketing validation devices, on-board units, sensors, communication systems, and passenger displays. Hardware demand is rising due to fleet modernization initiatives, infrastructure digitization, and connected transit adoption, with IoT-enabled sensors and communication devices enhancing operational intelligence and predictive maintenance. Advanced display technologies, including high-brightness LEDs and solar-powered units, are expanding information access for passengers.

The public transit operators segment accounted for 49% share in 2025 and is projected to grow at a CAGR of 8.7% between 2026 and 2035. Growth is driven by the rapid digital transformation of urban transport networks and increasing investments in intelligent mobility solutions. Transit agencies are deploying real-time passenger information systems, cloud-based management platforms, and fleet tracking solutions to optimize service efficiency and passenger satisfaction. Expansion of smart mobility programs and modernization of public transport infrastructure continue to boost market adoption.

U.S. Advanced Public Transportation System (APTS) Market reached USD 2.4 billion in 2025 and is expected to grow at a CAGR of 8% from 2026 to 2035. The country leads due to strong federal funding, regulatory oversight from agencies, and investments in connected vehicle pilot corridors. U.S. transit operators focus on automation of bus rapid transit, adaptive signal integration, and multimodal interchange optimization, leveraging simulations and digital modeling to manage complex traffic and suburban mobility patterns.

Key players operating in the Global Advanced Public Transportation System (APTS) Market include Siemens Mobility, Cubic Transportation, Trapeze, Moovit (Intel), Alstom, INIT SE, Conduent Transportation, Hitachi Rail, Optibus, and Thales. Companies in the Global Advanced Public Transportation System (APTS) Market strengthen their foothold by investing heavily in R&D to enhance system interoperability, cloud integration, and predictive analytics capabilities. They focus on developing scalable solutions capable of managing multimodal transit networks and upgrading existing infrastructure without replacement. Strategic partnerships with transit agencies, technology integrators, and municipalities help expand market reach and streamline deployment. Vendors leverage AI, IoT, and open payment systems to differentiate offerings while ensuring regulatory compliance. Additionally, firms enhance their presence through geographic expansion, pilot projects, and offering comprehensive maintenance and support services.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Mode of Transportation

- 2.2.6 Deployment Mode

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing urbanization and traffic congestion mitigation

- 3.2.1.2 Government initiatives for smart city development

- 3.2.1.3 Rising demand for enhanced passenger experience

- 3.2.1.4 Fleet electrification and sustainability mandates

- 3.2.1.5 Growth of mobility-as-a-service (MaaS) platforms

- 3.2.1.6 Workforce shortage driving automation adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment for APTS deployment

- 3.2.2.2 Infrastructure limitations in developing regions

- 3.2.2.3 Data privacy and cybersecurity concerns

- 3.2.2.4 Legacy system integration complexities

- 3.2.3 Market opportunities

- 3.2.3.1 Public-private partnership (PPP) funding models

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 Autonomous transit vehicle integration

- 3.2.3.4 Multimodal integration and seamless connectivity

- 3.2.3.5 AI-powered predictive maintenance solutions

- 3.2.3.6 Electric bus charging optimization technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal transit safety & ITS guidance

- 3.4.1.2 Canada - Connected public transport safety framework

- 3.4.2 Europe

- 3.4.2.1 Germany- EU ITS & national smart mobility initiatives

- 3.4.2.2 UK- Post-Brexit APTS adoption flexibility

- 3.4.2.3 France- National ITS strategy & connected transit standards

- 3.4.2.4 Italy- ITS pilots & smart public transport infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- Connected transit mandates & ITS standards

- 3.4.3.2 India- Emerging APTS regulations & pilot programs

- 3.4.3.3 Japan- ITS connect & automated transit policies

- 3.4.3.4 Australia- Technology-neutral ITS & smart city transit policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- Public transport safety & telematics standards

- 3.4.4.2 Brazil- Smart mobility & urban transit modernization

- 3.4.4.3 Argentina-National urban transport regulations & ITS pilots

- 3.4.5 MEA

- 3.4.5.1 South Africa- Road traffic act & ITS adoption guidelines

- 3.4.5.2 Saudi Arabia- Vision 2030 mobility & connected transit regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Software-defined vehicles (SDV) & smart bus platforms

- 3.7.1.2 AI & machine learning in transit operations

- 3.7.1.3 5G & V2X communication technologies

- 3.7.2 Emerging technologies

- 3.7.2.1 Cloud computing & edge analytics

- 3.7.2.2 Internet of Things (IoT) integration

- 3.7.2.3 Blockchain for fare collection & data security

- 3.7.2.4 Augmented reality (AR) for passenger information

- 3.7.1 Current technological trends

- 3.8 Cost breakdown analysis

- 3.9 Patent landscape (driven by primary research)

- 3.9.1 Key patent holders & technology leaders

- 3.9.2 Emerging technology patent trends

- 3.9.3 Geographic distribution of patent activity

- 3.9.4 Patent expiration impact on market competition

- 3.10 Pricing analysis

- 3.10.1 Historical price trend analysis

- 3.10.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.10.3 Total cost of ownership (TCO) analysis

- 3.11 Trade data analysis (driven by paid database)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Infrastructure & deployment landscape (driven by primary research)

- 3.13.1 Deployment penetration by region & buyer segment

- 3.13.2 Scalability constraints & infrastructure investment trends

- 3.14 Use case library & application scenarios

- 3.14.1 Smart city integration use cases

- 3.14.2 Fleet electrification management scenarios

- 3.14.3 Demand-responsive transit implementation models

- 3.14.4 Multimodal hub connectivity solutions

- 3.14.5 COVID-19 recovery & network redesign scenarios

- 3.14.6 Autonomous transit integration roadmaps

- 3.15 Market maturity & technology adoption curve analysis

- 3.15.1 Technology adoption stage by region

- 3.15.2 Early adopter vs laggard agency profiles

- 3.15.3 Chasm analysis for emerging technologies (V2X, autonomous transit, GenAI)

- 3.15.4 Market saturation indicators by solution type

- 3.15.5 Innovation diffusion timeline (2024-2034)

- 3.16 Sustainability and environmental aspects

- 3.16.1 Sustainable practices

- 3.16.2 Waste reduction strategies

- 3.16.3 Energy efficiency in production

- 3.16.4 Eco-friendly Initiatives

- 3.16.5 Carbon footprint considerations

- 3.17 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Display panels

- 5.2.3 Communication devices

- 5.2.4 Onboard computers

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Fleet management platforms

- 5.3.2 Passenger information systems

- 5.3.3 Traffic control & analytics solutions

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Real-time passenger information system

- 6.3 Automated vehicle location (AVL)

- 6.4 Computer-aided dispatch (CAD)

- 6.5 Electronic payment systems (EPS)

- 6.6 Passenger information systems (PIS)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Traffic management

- 7.3 Fleet management

- 7.4 Passenger safety & security

- 7.5 Ticketing solutions

- 7.6 Public information dissemination

Chapter 8 Market Estimates & Forecast, By Mode of Transportation, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Roadways

- 8.3 Railways

- 8.4 Airways

- 8.5 Waterways

Chapter 9 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 On premises

- 9.3 Cloud-based

- 9.4 Hybrid

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Public transit operators

- 10.3 Government bodies

- 10.4 Private fleet operators

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.3.9 Denmark

- 11.3.10 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Israel

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Alstom

- 12.1.2 Conduent Transportation

- 12.1.3 Cubic Transportation Systems

- 12.1.4 Hitachi Rail

- 12.1.5 Siemens Mobility

- 12.1.6 Thales

- 12.1.7 Trapeze

- 12.2 Regional Players

- 12.2.1 Indra Sistemas

- 12.2.2 INIT SE

- 12.2.3 Masabi

- 12.2.4 Moovit

- 12.2.5 Optibus

- 12.2.6 Swiftly

- 12.2.7 Via Transportation

- 12.3 Emerging Players & Technology Enablers

- 12.3.1 Vix Technology

- 12.3.2 Bytemark

- 12.3.3 Clever Devices

- 12.3.4 Genfare

- 12.3.5 Scheidt & Bachmann

- 12.3.6 Spare Labs