PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019156

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019156

Eco-friendly Food Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

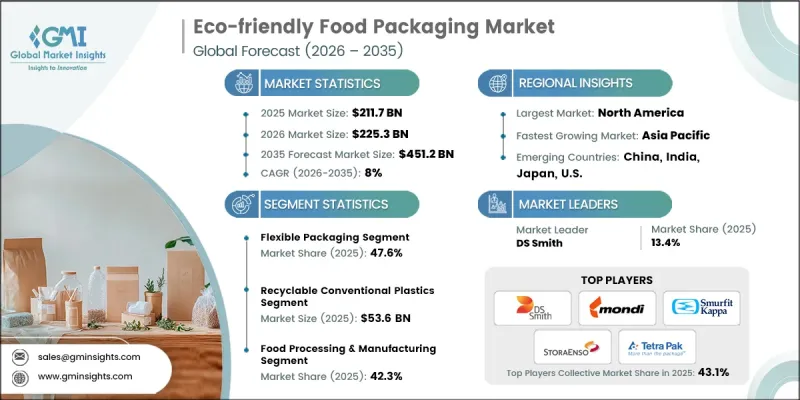

The Global Eco-friendly Food Packaging Market was valued at USD 211.7 billion in 2025 and is estimated to grow at a CAGR of 8% to reach USD 451.2 billion by 2035.

Market growth is driven by stricter regulatory frameworks aimed at reducing plastic waste, along with the rising adoption of sustainable packaging solutions across the food and beverage sector. Increasing demand for environmentally responsible alternatives, combined with rapid expansion in food delivery services, is accelerating the transition toward recyclable and compostable materials. Continuous innovation in bio-based packaging technologies is also enhancing product performance and sustainability credentials. Manufacturers are focusing on reducing environmental impact while maintaining packaging efficiency and durability. The growing emphasis on circular economy practices is encouraging companies to adopt materials that can be reused or recycled efficiently. In addition, the shift toward sustainable consumption patterns is reinforcing demand for eco-conscious packaging formats, making eco-friendly food packaging a key focus area across global supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $211.7 Billion |

| Forecast Value | $451.2 Billion |

| CAGR | 8% |

The eco-friendly food packaging industry is experiencing strong momentum due to tightening regulations targeting single-use plastics across major economies. Regulatory bodies are enforcing stricter compliance standards to minimize environmental impact, prompting companies to transition toward sustainable alternatives. At the same time, food and beverage manufacturers are committing to higher sustainability targets by adopting recyclable and compostable materials. The shift toward fiber-based and paper-based packaging solutions is gaining traction as businesses aim to replace traditional plastic formats. Industry participants are increasingly aligning their packaging strategies with circular economy principles, focusing on material recovery and reuse. This transition is reshaping product development and supply chain strategies, encouraging innovation in sustainable material applications.

The flexible packaging segment accounted for 47.6% share in 2025 owing to its lightweight structure, reduced material usage, and cost efficiency. This packaging format supports improved product preservation and optimized logistics, contributing to its widespread adoption across the food supply chain. Ongoing advancements in recyclable mono-material structures and sustainable laminate solutions are further enhancing its appeal. The ability to balance performance with environmental considerations continues to drive strong demand for flexible packaging solutions.

The recyclable conventional plastics segment generated USD 53.6 billion in 2025. This segment remains prominent as it offers a practical balance between sustainability and functionality. Established recycling infrastructure, cost advantages, and compatibility with existing production systems support its continued use. Materials within this category provide effective product protection, extend shelf life, and comply with regulatory requirements while contributing to circular economy initiatives.

North America Eco-friendly Food Packaging Market held a 46.2% share in 2025, supported by regulatory pressure and increasing corporate focus on sustainability. The region is witnessing the broad adoption of recyclable, compostable, and fiber-based packaging formats across food-related industries. Investments in advanced materials and packaging technologies are strengthening innovation capabilities. Growing demand from food retail, packaged goods, and delivery services is sustaining market expansion, positioning the region as a leader in sustainable packaging adoption through 2035.

Key companies operating in the Global Eco-friendly Food Packaging Market include Amcor, Biomass Packaging, Biopak, DS Smith, Elopak, Genpak, Huhtamaki, International Paper, Karl Knauer, Mondi, Nordic Paper, PacknWood, Smurfit Kappa, Sonoco Products, Stora Enso, Sulapac, Tetra Pak, TIPA, Vegware, and WestRock. Companies in the Global Eco-friendly Food Packaging Market are strengthening their competitive position through innovation, strategic partnerships, and sustainability-driven initiatives. Many firms are investing in research and development to create advanced bio-based and recyclable materials that meet performance and regulatory standards. Businesses are forming collaborations across the value chain to enhance recycling infrastructure and support circular economy models. Expansion of product portfolios with sustainable alternatives is helping companies address evolving consumer preferences. In addition, organizations are leveraging digital technologies to improve supply chain transparency and operational efficiency. Companies are also focusing on sustainable sourcing, eco-friendly manufacturing processes, and compliance with global environmental regulations to reinforce brand positioning and long-term market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Application trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent single-use plastic bans across EU, India, North America

- 3.2.1.2 FMCG brands adopting recyclable and compostable packaging targets

- 3.2.1.3 E-commerce food delivery driving need for biodegradable packaging

- 3.2.1.4 Corporate ESG commitments accelerating packaging material transitions

- 3.2.1.5 Advancements in bio-based polymers improving barrier performance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited industrial composting infrastructure in emerging economies

- 3.2.2.2 Performance limitations in moisture and oxygen barrier properties

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of molded fiber packaging in quick-service restaurants

- 3.2.3.2 Growth in reusable packaging systems for urban food delivery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Paper & paperboard

- 5.3 Recyclable conventional plastics

- 5.4 Recycled plastics

- 5.5 Bio-based & biodegradable plastics

- 5.6 Metal

- 5.7 Glass

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.3 Flexible packaging

- 6.4 Semi-rigid packaging

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fresh food

- 7.3 Dairy products

- 7.4 Frozen food (including frozen desserts)

- 7.5 Processed food

- 7.6 Beverages

- 7.7 Sauces, dressings & condiments

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food processing & manufacturing

- 8.3 Foodservice operators

- 8.4 Retail & private label packaging

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor

- 10.1.2 DS Smith

- 10.1.3 Mondi

- 10.1.4 Smurfit Kappa

- 10.1.5 Stora Enso

- 10.1.6 Tetra Pak

- 10.1.7 Huhtamaki

- 10.1.8 Sonoco Products

- 10.1.9 WestRock

- 10.1.10 International Paper

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Genpak

- 10.2.2 Asia Pacific

- 10.2.2.1 Biopak

- 10.2.3 Europe

- 10.2.3.1 Elopak

- 10.2.3.2 Karl Knauer

- 10.2.3.3 Nordic Paper

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Biomass Packaging

- 10.3.2 PacknWood

- 10.3.3 Sulapac

- 10.3.4 TIPA

- 10.3.5 Vegware