PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019162

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019162

Pet Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

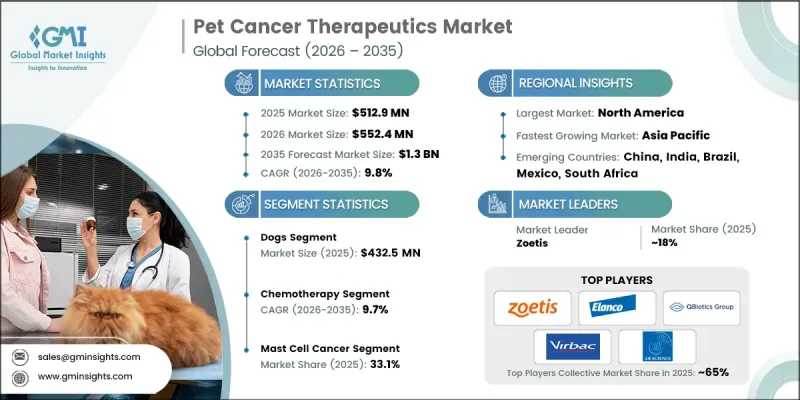

The Global Pet Cancer Therapeutics Market was valued at USD 512.9 million in 2025 and is estimated to grow at a CAGR of 9.8% to reach USD 1.3 billion by 2035.

The market's rapid expansion is driven by the growing trend of pet humanization, with owners increasingly treating pets as family members and investing in advanced healthcare solutions. Improved diagnostic technologies, targeted therapies, and immunotherapies have enhanced access to effective cancer care. Additionally, an aging pet population has led to higher cancer prevalence, further stimulating demand for veterinary oncology solutions. As consumers increasingly prioritize quality care and life-extending treatments, innovations in veterinary medicine, ranging from precision diagnostics to minimally invasive therapies, are playing a central role in shaping market growth. The convergence of advanced therapeutics, increased pet ownership, and rising awareness among pet owners is driving the adoption of sophisticated oncology treatments globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $512.9 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 9.8% |

Pet cancer therapeutics encompass a broad range of treatments aimed at diagnosing, managing, and treating cancers in companion animals. These therapies include chemotherapy, immunotherapies, targeted therapies, and combination regimens designed to reduce tumor size, manage symptoms, and improve overall pet health. Advances in veterinary oncology, such as precision medicine, genomic diagnostics, and immunotherapy, are enabling more effective and less invasive treatments. These innovations are improving survival rates and quality of life for pets diagnosed with cancer, creating substantial demand for advanced therapeutics. Veterinary practitioners are increasingly adopting these therapies due to their targeted effects and improved safety profiles, which drive the market's continuous expansion.

The dogs segment reached USD 432.5 million in 2025. Dogs account for the largest share because cancer incidence is higher in this species compared to other pets. Conditions such as lymphoma, osteosarcoma, and mammary tumors are commonly diagnosed in dogs, driving demand for specialized therapeutics. Increased owner awareness about canine cancer and the availability of effective treatment options further support the dominance of the dog segment in the pet cancer therapeutics market.

The injectable therapies segment is projected to reach USD 835.4 million by 2035. Injectables are favored due to their ability to deliver treatment directly into the bloodstream or tumor site, ensuring rapid absorption and targeted action. Chemotherapy agents, immunotherapies, and other injectable formulations offer precise dosing and enhanced control over side effects, making them highly effective for treating various cancers in pets. Continuous innovations in injectable delivery systems are expected to sustain strong market demand for this segment.

North America Pet Cancer Therapeutics Market held a 78.4% share in 2025. The region's leadership is fueled by high pet ownership, widespread use of advanced therapies, and strong adoption of genomic diagnostics, AI-enabled cytology, and imaging systems that enable early detection and personalized treatment planning. The prevalence of cancer in dogs and cats, high veterinary healthcare spending, and growing emphasis on early-stage interventions and premium therapeutics are driving robust market growth in North America.

Key players in the Global Pet Cancer Therapeutics Market include Zoetis, Elanco Animal Health, Virbac, Dechra Pharmaceuticals, AB Science, NovaVive, Karyopharm Therapeutics, Akston Biosciences, CureLab Oncology, VetDC, Boehringer Ingelheim, Vivesto, ELIAS Animal Health, Qbiotics, and Immuvera. Companies in the Global Pet Cancer Therapeutics Market are pursuing several strategies to strengthen their market position. They are investing heavily in R&D to develop innovative targeted and immunotherapy treatments. Strategic partnerships with veterinary clinics, research institutions, and distribution networks are expanding market access. Product pipelines are being diversified to include injectable, oral, and combination therapies. Geographic expansion into emerging markets and the adoption of digital veterinary tools enhance customer reach. Companies emphasize awareness campaigns, clinical education, and after-sales support programs to build trust with pet owners and veterinarians, solidifying brand loyalty and sustaining long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Species trends

- 2.2.3 Therapy trends

- 2.2.4 Route of administration trends

- 2.2.5 Cancer type trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet humanization

- 3.2.1.2 Rising cancer incidence in pets

- 3.2.1.3 Advancements in veterinary oncology diagnosis and treatment

- 3.2.1.4 Growing awareness and diagnostic capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Side effects and animal tolerance

- 3.2.3 Market opportunities

- 3.2.3.1 Development of personalized cancer vaccines for pets

- 3.2.3.2 Expansion of AI-powered diagnostic and treatment platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by primary research)

- 3.6 Pipeline analysis (Driven by primary research)

- 3.7 Investment and funding landscape in pet care (Driven by primary research)

- 3.8 Pet population, by country

- 3.9 Pet insurance coverage and reimbursement landscape (Driven by primary research)

- 3.10 Impact of AI and generative AI on the market (Driven by primary research)

- 3.11 Future market trends (Driven by primary research)

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Species, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Dogs

- 5.3 Cats

- 5.4 Other species

Chapter 6 Market Estimates and Forecast, By Therapy, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapy

- 6.3 Immunotherapy

- 6.4 Targeted therapy

- 6.5 Combination therapy

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Cancer Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Lymphoma

- 8.3 Mast cell cancer

- 8.4 Melanoma

- 8.5 Mammary and squamous cell cancer

- 8.6 Other cancer types

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AB Science

- 10.2 Akston Biosciences

- 10.3 Boehringer Ingelheim

- 10.4 CureLab Oncology

- 10.5 Dechra Pharmaceuticals

- 10.6 Elanco Animal Health

- 10.7 ELIAS Animal Health

- 10.8 Immuvera

- 10.9 Karyopharm Therapeutic

- 10.10 NovaVive

- 10.11 Qbiotics

- 10.12 VetDC

- 10.13 Vibrac

- 10.14 Vivesto

- 10.15 Zoetis