PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019174

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019174

LNG Marine Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

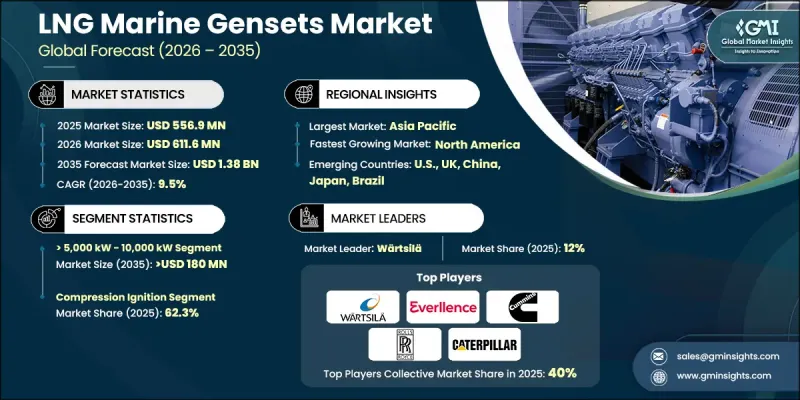

The Global LNG Marine Gensets Market was valued at USD 556.9 million in 2025 and is estimated to grow at a CAGR of 9.5% to reach USD 1.38 billion by 2035.

The growth is fueled by the expansion of seaborne trade and the rising popularity of maritime tourism, as more vessels are equipped with cleaner energy solutions. LNG marine gensets offer a sustainable alternative to conventional marine fuels, aligning with global efforts to reduce greenhouse gas emissions in shipping. Increased import and export activities, especially of commodities like minerals, crude oil, and industrial goods, are further supporting market demand. Rising disposable incomes, improved infrastructure, and government initiatives to promote marine tourism in emerging economies are expanding the industry's reach. Moreover, urbanization and international trade growth are creating new opportunities for shipbuilders and vessel operators seeking efficient and environmentally friendly power generation solutions for their fleets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $556.9 Million |

| Forecast Value | $1.38 Billion |

| CAGR | 9.5% |

LNG marine gensets are electrical power systems that generate electricity on vessels using liquefied natural gas as fuel. LNG is vaporized and combusted in an internal combustion engine, which drives the generator to produce electricity. The surge in maritime tourism, including cruise and ferry services, is encouraging the adoption of LNG-powered gensets. Supportive government policies promoting sustainable marine transport, combined with population growth and infrastructure development in emerging regions, are further contributing to market expansion.

The >5,000 kW to 10,000 kW segment is projected to reach USD 180 million by 2035. Growth is driven by increasing maritime trade in developing regions, expansion of shipbuilding activities, and rising global urbanization. This segment is particularly attractive as larger vessels require high-capacity gensets to maintain operational efficiency.

The compression ignition LNG marine gensets segment held a 62.3% share in 2025. The increasing focus on environmental sustainability and stricter emission regulations are pushing ship operators to adopt cleaner, fuel-efficient gensets. These units produce significantly lower emissions compared to conventional diesel engines, driving demand in countries with stringent environmental standards. The rising need for tugboats, yachts, and specialized marine vessels is also boosting market adoption.

U.S. LNG Marine Gensets Market was valued at USD 54.2 million in 2025. Growth is supported by expanding shipbuilding activities, availability of raw materials, technological innovations, and increasing maritime trade. Additionally, rising recreational marine tourism and cost-efficient labor resources are expected to enhance industry dynamics and strengthen market penetration.

Leading players operating in the Global LNG Marine Gensets Market include Cummins, ABB, Caterpillar, MAN Rollo, Mitsubishi Heavy Industries, Scania, Volvo Penta, Rolls-Royce, Fischer Panda, HD Hyundai Heavy Industries & Engines Machinery, Jinan Diesel Engine Co., Nidec Corporation, Rehlko, Kirloskar, Lindenberg-Anlagen, Guascor Energy, Sandfirden Technics, and Everllence. Companies in the Global LNG Marine Gensets Market are strengthening their positions by investing in advanced, fuel-efficient genset technologies with lower emissions. Strategic partnerships with shipbuilders, port operators, and vessel owners expand market reach. Continuous R&D focuses on increasing reliability, energy efficiency, and system integration with renewable energy sources. Firms also diversifying product portfolios to cater to various vessel capacities and applications. Market leaders emphasize regulatory compliance, particularly regarding international maritime emission standards, to gain trust and expand adoption. Additionally, after-sales service networks, technical support, and digital monitoring solutions enhance customer retention and create long-term competitive advantages in the LNG marine gensets space.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates and forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power rating trends

- 2.1.3 Technology trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/Unit)

- 3.5.1 By region

- 3.5.2 By power rating

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of LNG marine gensets

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 1,000 kW

- 5.3 > 1,000 kW - 5,000 kW

- 5.4 > 5,000 kW - 10,000 kW

- 5.5 > 10,000 kW - 20,000 kW

- 5.6 > 20,000 kW

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Spark ignition

- 6.3 Compression ignition

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Merchant

- 7.3 Offshore

- 7.4 Cruise & ferry

- 7.5 Navy

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 Norway

- 8.3.5 France

- 8.3.6 Russia

- 8.3.7 Denmark

- 8.3.8 Netherlands

- 8.3.9 Belgium

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Vietnam

- 8.4.7 Singapore

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Iran

- 8.5.4 Angola

- 8.5.5 Egypt

- 8.5.6 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Mexico

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Caterpillar

- 9.3 Chevron

- 9.4 Cummins

- 9.5 Everllence

- 9.6 Fischer Panda

- 9.7 Guascor Energy

- 9.8 HD Hyundai Heavy Industries & Engines Machinery

- 9.9 Jinan Diesel Engine Co.

- 9.10 Kirloskar

- 9.11 Lindenberg-Anlagen

- 9.12 MAN Rollo

- 9.13 Mitsubishi Heavy Industries

- 9.14 Nidec Corporation

- 9.15 Rehlko

- 9.16 Rolls-Royce

- 9.17 Sandfirden Technics

- 9.18 Scania

- 9.19 Volvo Penta

- 9.20 Wartsila