PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019184

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019184

Laser Welding Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

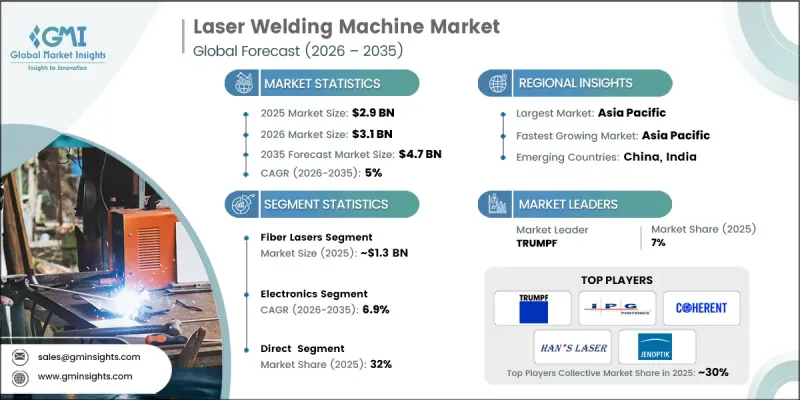

The Global Laser Welding Machine Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 4.7 billion by 2035.

The laser welding machine market is gaining strong traction as industries accelerate their transition toward automation and digitally integrated manufacturing environments. Increasing deployment of robotic welding cells, smart production systems, and Industry 4.0 frameworks is significantly enhancing demand for high-precision welding technologies. These machines offer exceptional accuracy, repeatability, and seamless compatibility with advanced control platforms, making them highly suitable for modern industrial workflows focused on consistency and efficiency. Their non-contact operation minimizes wear and tear, reduces maintenance frequency, and ensures uninterrupted production cycles. Additionally, real-time monitoring and integrated sensing technologies support automated quality assurance, further strengthening their value proposition. As manufacturers continue to prioritize productivity optimization and reduced operational variability, laser welding solutions are becoming an essential component of next-generation production lines. Growing investments in smart factories and advanced manufacturing infrastructure are expected to further accelerate adoption across multiple industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 5% |

The laser welding machine market continues to evolve as automation becomes central to industrial operations, driving widespread implementation of high-performance welding systems. Companies are increasingly adopting technologies that deliver continuous operation with minimal downtime, aligning with the need for efficient and scalable production. Enhanced system capabilities, including precision control and intelligent monitoring, are enabling manufacturers to achieve superior output quality while maintaining operational flexibility. These advancements are reinforcing the role of laser welding equipment in modern manufacturing ecosystems and supporting long-term market expansion.

The fiber lasers segment generated USD 1.3 billion in 2025 and is projected to grow at a CAGR of 4.2% from 2026 to 2035. This segment maintains a strong position due to its high energy efficiency, superior beam quality, and lower maintenance requirements compared to conventional laser technologies. Fiber laser systems enable precise and clean welding with minimal thermal distortion, making them highly effective for applications that demand accuracy and consistency. Their growing adoption is gradually replacing traditional laser systems across both automated and manual welding operations, further strengthening their dominance in the market.

The direct distribution segment accounted for 32% share in 2025, highlighting its importance in delivering complex industrial solutions. Direct sales channels allow manufacturers to establish strong customer relationships while offering customized system configurations, installation support, and technical training. This approach is particularly valuable for high-investment equipment, where end users require ongoing service, maintenance, and expert guidance. The preference for direct engagement continues to grow as businesses seek reliable partnerships and tailored solutions to meet specific operational requirements.

United States Laser Welding Machine Market reached USD 600 million in 2025 and is expected to grow at a CAGR of 5.1% through 2035, maintaining its leadership in the North America region. This growth is supported by advanced manufacturing capabilities, increasing automation levels, and a strong industrial presence across key sectors. Rising demand for precision manufacturing processes, along with continuous investment in next-generation production technologies, is strengthening market expansion. The country's focus on innovation and efficiency improvements continues to drive the adoption of advanced laser welding systems across various industrial applications.

Key participants in the Global Laser Welding Machine Market include Amada Weld Tech, CHIRON Group, Coherent, Emerson Electric, Han's Laser Technology Industry Group, Huagong Laser Engineering, IPG Photonics, Jenoptik, KEYENCE, Laser Technologies, Laserline, Laser Star Technologies, Penta Laser, Precitec, and TRUMPF. Companies in the Laser Welding Machine Market are reinforcing their market position through continuous technological innovation, strategic collaborations, and customer-centric approaches. They are investing in advanced laser technologies, automation integration, and smart manufacturing solutions to enhance product performance and efficiency. Partnerships with industrial clients and system integrators enable tailored solutions and long-term contracts. Businesses are also expanding their global footprint through distribution networks and localized service support. Emphasis on research and development is driving improvements in precision, energy efficiency, and system reliability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Output

- 2.2.4 End use industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of automation in manufacturing

- 3.2.1.2 Rising demand for high-precision welding

- 3.2.1.3 Technological advancements in laser sources

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Skilled workforce shortage

- 3.2.3 Opportunities

- 3.2.3.1 Increasing use in electric vehicle (EV) manufacturing

- 3.2.3.2 Expansion in medical device fabrication

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.1.1 US: Consumer Product Safety Commission (CPSC) 16 Code of Federal Regulations (CFR) part 1512

- 3.7.1.2 Canada: International Organization for Standardization (ISO) 4210

- 3.7.2 Europe

- 3.7.2.1 Germany: Deutsches Institut fur Normung (DIN) European Norm (EN) ISO 4210

- 3.7.2.2 UK: European Norm (EN) ISO 4210 / United Kingdom Conformity Assessed (UKCA)

- 3.7.2.3 France: European Norm (EN) ISO 4210

- 3.7.3 Asia Pacific

- 3.7.3.1 China: Guobiao (GB) 3565

- 3.7.3.2 India: Indian Standard (IS) 10613

- 3.7.3.3 Japan: Japanese Industrial Standard (JIS) D 9110

- 3.7.4 Latin America

- 3.7.4.1 Brazil: Associacao Brasileira de Normas Tecnicas (ABNT) Norma Brasileira (NBR) ISO 4210

- 3.7.4.2 Mexico: International Organization for Standardization (ISO) 4210

- 3.7.5 Middle East & Africa

- 3.7.5.1 South Africa: South African National Standard (SANS) 311

- 3.7.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization (SASO) Gulf Standardization Organization (GSO) ISO 4210

- 3.7.1 North America

- 3.8 Trade data analysis (HS Code - 851580)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of ai & generative ai on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 Genai use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Fiber lasers

- 5.3 Co2 lasers

- 5.4 Diode lasers

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Output, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Below 3 kW

- 6.3 3 kW - 6 kW

- 6.4 Above 6 kW

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Medical

- 7.4 Electronics

- 7.5 Aerospace & defense

- 7.6 Jewelry

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Amada Weld Tech

- 10.2 CHIRON Group

- 10.3 Coherent

- 10.4 Emerson Electric

- 10.5 Han's Laser Technology Industry Group

- 10.6 Huagong Laser Engineering

- 10.7 IPG Photonics

- 10.8 Jenoptik

- 10.9 KEYENCE

- 10.10 Laser Technologies

- 10.11 Laser line

- 10.12 Laser Star Technologies

- 10.13 Penta Laser

- 10.14 Precitec

- 10.15 TRUMPF