PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019193

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019193

Optical Communication and Networking Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

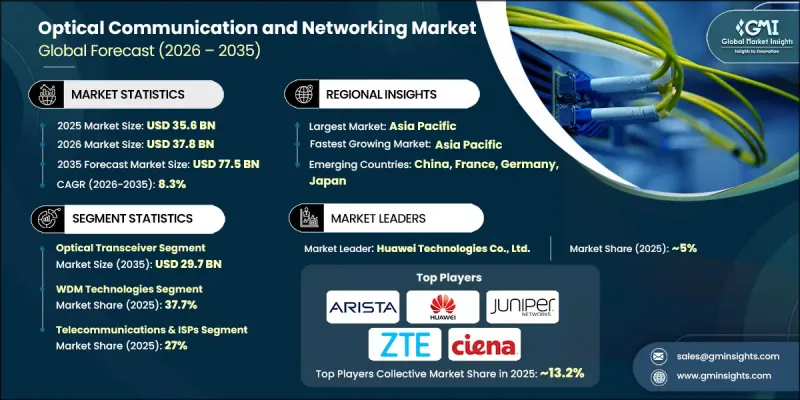

The Global Optical Communication and Networking Market was valued at USD 35.6 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 77.5 billion by 2035.

The market is expanding rapidly as digitalization accelerates globally and 5G technology becomes widely deployed. Telecommunications providers are increasingly building out high-capacity fiber optic networks for both backhaul and fronthaul, integrating Dense Wavelength Division Multiplexing (DWDM) and Coherent Optical technologies. These developments are critical for supporting reliable connectivity in smart cities, industrial automation, and IoT ecosystems, positioning optical networks as a cornerstone of modern digital infrastructure. The growth of hyperscale data centers and the rising demand for cloud services are also major drivers. Advanced optical transport solutions and high-speed transceivers enable fast, large-volume data transfer, supporting AI, cloud computing, and enterprise applications. Ongoing innovations in optical coherent technologies, including 800G solutions, reduce power consumption while increasing capacity, encouraging continued investment in routed optical networks to enhance performance and scalability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $35.6 Billion |

| Forecast Value | $77.5 Billion |

| CAGR | 8.3% |

The optical amplifiers segment generated USD 5.5 billion in 2025 and is expected to grow at a CAGR of 8.1% during 2026-2035. The expansion is fueled by increasing global data traffic and the need for signal boosting across long-haul, metro, and data center networks. Innovations such as multi-core amplifiers significantly reduce energy usage while expanding throughput, and emerging low-power, chip-scale amplifiers offer efficient integration in next-generation photonic networks, enhancing network performance and energy efficiency.

The optical transport network (OTN) segment is projected to grow at a CAGR of 9.5% between 2026 and 2035. OTN provides standardized, robust transport solutions capable of managing diverse client traffic over optical backbones. Its ability to support multiplexing, routing, and traffic management makes it essential for 5G backhaul, cloud interconnects, and secure enterprise communication, reinforcing the reliability and scalability of global high-capacity networks.

U.S. Optical Communication and Networking Market accounted for USD 8.4 billion in 2025 and continues to expand as operators scale fiber networks and optical backhaul to meet growing 5G, cloud, and AI-driven data demands. Telecommunications companies are investing in backbone upgrades, network expansion, and strategic acquisitions to enhance broadband capacity and integrate high-speed services. Leading suppliers are securing multi-billion-dollar contracts for fiber deployment and data center infrastructure, reflecting sustained investment in telecommunications and enterprise ecosystems.

Key players in the Global Optical Communication and Networking Market include Adtran, Arista Networks, Inc., Ciena Corporation, Cisco Systems, Inc., FiberHome, FUJITSU, General Atomics, Huawei Technologies Co., Ltd., Juniper Networks, Inc., Mitsubishi Electric Corporation, NEC Corporation, Nokia, Space Photonics Inc., Telefonaktiebolaget LM Ericsson, and ZTE Corporation. Companies in the Optical Communication and Networking Market are implementing several strategies to strengthen their presence and market foothold. They are investing heavily in research and development to create high-speed, energy-efficient, and scalable optical solutions. Strategic partnerships with telecommunications operators, hyperscale data center providers, and enterprise clients expand deployment opportunities. Firms are also pursuing mergers and acquisitions to enhance network coverage, secure intellectual property, and increase market share. Additionally, companies are focusing on developing software-defined networking (SDN) and automated optical solutions to provide flexible, cost-effective services. Participation in global standardization initiatives, customer-centric innovation, and regional expansion into emerging markets further solidifies their competitive position, ensuring long-term growth and industry leadership.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Deployment model trends

- 2.2.3 End-user industry trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion and rollout of 5G and future mobile networks

- 3.2.1.2 Rapid growth of hyperscale data centers

- 3.2.1.3 Rising global internet usage and data traffic volumes

- 3.2.1.4 Rising adoption of cloud based services and virtualization

- 3.2.1.5 Growth of IoT and digital transformation across sectors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital expenditure on deployment and upgrades

- 3.2.2.2 Complexity in integrating optical technology with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in edge computing and hybrid networks

- 3.2.3.2 Adoption of advanced optical technologies in enterprise/data center networks

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors’ landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Optical Fiber

- 5.3 Optical Transceiver

- 5.4 Optical Switch

- 5.5 Optical Amplifiers

- 5.6 Optical Circulators

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 WDM Technologies

- 6.3 SONET/SDH

- 6.4 Fibre Channel

- 6.5 Optical Packet Transport (OTN)

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Data Rate, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 ≤ 10 Gbps

- 7.3 10-40 Gbps

- 7.4 40-100 Gbps

- 7.5 above 100 Gbps

Chapter 8 Market Estimates and Forecast, By Vertical, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Telecommunications & ISPs

- 8.3 Data Centers & Cloud Providers

- 8.4 Government & Public Sector

- 8.5 Defense & Aerospace

- 8.6 Energy & Utilities

- 8.7 Industrial & Manufacturing

- 8.8 BFSI (Banking, Financial Services & Insurance)

- 8.9 Healthcare & Life Sciences

- 8.10 Media, Broadcasting & Entertainment

- 8.11 Retail & Commercial Enterprises

- 8.12 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Adtran

- 10.2 Arista Networks, Inc.

- 10.3 Ciena Corporation.

- 10.4 Cisco Systems, Inc.

- 10.5 FiberHome

- 10.6 FUJITSU

- 10.7 General Atomics

- 10.8 Huawei Technologies Co., Ltd.

- 10.9 Juniper Networks, Inc.

- 10.10 Mitsubishi Electric Corporation

- 10.11 NEC Corporation

- 10.12 Nokia

- 10.13 Space Photonics Inc.

- 10.14 Telefonaktiebolaget LM Ericsson

- 10.15 ZTE Corporation