PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019198

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019198

OEM Electric Drive Unit (EDU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

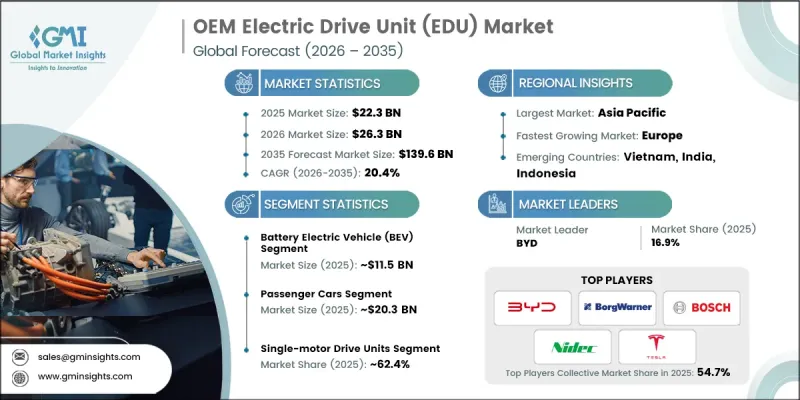

The Global OEM Electric Drive Unit Market was valued at USD 22.3 billion in 2025 and is estimated to grow at a CAGR of 20.4% to reach USD 139.6 billion by 2035.

The growth is driven by the global shift toward vehicle electrification, accelerated investments by leading automakers, and continuous innovations in battery technology. Governments worldwide are implementing stringent emission standards, while many countries are planning to phase out internal combustion engine vehicles in favor of electric vehicles, creating strong demand for electric drive units. Improvements in lithium-ion and solid-state battery efficiency, longer life cycles, and reduced costs have made electric vehicles more appealing to consumers, further increasing the adoption of EDUs. Incentive programs, subsidies, and supportive policies from governments continue to boost market growth. OEM investments in EDUs are also influenced by increasing consumer awareness, environmental concerns, and the need for zero-emission mobility solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.3 Billion |

| Forecast Value | $139.6 Billion |

| CAGR | 20.4% |

The battery electric vehicles (BEVs) segment held a 51.3% share, generating USD 11.5 billion in 2025. The BEV segment's dominance is driven by strict emission regulations, OEM commitments, and consumer adoption supported by government incentives. Zero-emission vehicle mandates and growing environmental consciousness are encouraging manufacturers to prioritize BEV production, driving demand for high-performance EDUs over hybrid and fuel cell variants.

The passenger car segment accounted for 91% share in 2025, valued at USD 20.3 billion, reflecting the faster adoption of electric passenger vehicles compared with commercial vehicles. Factors such as wider model availability, robust production scales, expanding charging infrastructure, and consistent policy frameworks support this segment's continued leadership in the market.

U.S. OEM Electric Drive Unit Market reached USD 2.4 billion in 2025 and is projected to grow at a CAGR of 16.5% from 2026 to 2035. Federal and state EV policies, consumer adoption trends, and OEM strategies drive demand. Programs like the National Electric Vehicle Infrastructure (NEVI) Formula Program are supporting the rollout of EV charging networks, indirectly facilitating EDU adoption by alleviating range anxiety. Policy adjustments, including changes to US-content requirements for federally funded charging stations, are shaping the market ecosystem.

Leading companies in the Global OEM Electric Drive Unit Market include Schaeffler, Valeo, BYD, Bosch, Tesla, BorgWarner, Vitesco Technologies, Aisin, Nidec, and ZF Friedrichshafen. Key strategies employed by companies in the OEM electric drive unit market include investing in R&D to develop high-efficiency, lightweight, and compact EDUs, collaborating with battery and EV manufacturers for integrated solutions, and expanding production capacities to meet growing global demand. Firms are establishing regional manufacturing hubs to reduce supply chain risks, forming strategic partnerships with automotive OEMs, and adopting advanced digital manufacturing technologies to enhance product quality and reliability. Companies are also focusing on cost reduction, modular platform development, and technology licensing to strengthen market presence. Marketing and after-sales support, along with participation in sustainability initiatives, help build brand credibility and customer trust, further reinforcing their foothold in the competitive market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Drive Unit Configuration

- 2.2.4 Cooling Technology

- 2.2.5 Vehicle

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission regulations & zero-emission vehicle mandates

- 3.2.1.2 Increasing consumer demand for electric & hybrid vehicles

- 3.2.1.3 Government incentives & subsidies for EV adoption

- 3.2.1.4 Growing investment in EV infrastructure & charging networks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost & capital intensity of EDU manufacturing

- 3.2.2.2 Range anxiety & infrastructure gaps in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into off-highway & industrial vehicle segments

- 3.2.3.2 Strategic partnerships between OEMs & Tier-1 suppliers

- 3.2.3.3 Development of modular & scalable EDU platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - Environmental Protection Agency (EPA)

- 3.4.1.2 Canada - Transportation Canada

- 3.4.2 Europe

- 3.4.2.1 Germany - VDA (German Association of the Automotive Industry)

- 3.4.2.2 Italy - Ministry of Infrastructure and Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China - China National Standardization Administration (SAC)

- 3.4.3.2 Japan - Japan Automobile Standards Internationalization Center (JASIC)

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Instituto Nacional de Metrologia (INMETRO)

- 3.4.4.2 Mexico - Mexico’s Secretaria de Comunicaciones y Transportes (SCT)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Saudi Arabia - Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.2 South Africa - South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technologies

- 3.7.1.1 Permanent Magnet Synchronous Motors (PMSM)

- 3.7.1.2 Integrated Electric Drive Units (e-Axles)

- 3.7.1.3 400V Electrical Architecture Systems

- 3.7.1.4 Liquid Cooling Systems for Thermal Management

- 3.7.2 Emerging technologies

- 3.7.2.1 800V High-Voltage Electrical Architectures

- 3.7.2.2 Axial Flux Motors

- 3.7.2.3 Oil-Cooled and Direct Cooling Motor Technologies

- 3.7.1 Current technologies

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Cost breakdown analysis

- 3.9.1 Raw material cost analysis

- 3.9.2 Manufacturing & assembly cost structure

- 3.9.3 Power electronics & semiconductor cost contribution

- 3.9.4 Logistics, supply chain, and overhead costs

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Integration with Advanced Vehicle Architectures

- 3.13.1 Integration with software-defined vehicle architectures

- 3.13.2 Compatibility with advanced driver assistance systems (ADAS)

- 3.13.3 Centralized vs distributed powertrain control systems

- 3.13.4 Integration with 400V vs 800V systems architecture

- 3.14 Electrification Roadmaps of Major Automotive OEMs

- 3.14.1 Transition timelines from ICE to full electrification

- 3.14.2 Investment strategies in EV platforms and technologies

- 3.14.3 Oem-specific approaches to EDU development and integration

- 3.14.4 Partnerships, joint ventures, and technology collaborations

- 3.14.5 Regional variations in electrification strategies

- 3.15 Impact of AI & Generative AI on the Market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Battery Electric Vehicle (BEV)

- 5.3 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.4 Fuel Cell Electric Vehicles (FCEV)

- 5.5 Hybrid Electric Vehicle (HEV)

Chapter 6 Market Estimates & Forecast, By Drive Unit Configuration, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Single-Motor Drive Units

- 6.3 Dual-Motor Drive Units

- 6.4 Multi-Motor Drive Units

Chapter 7 Market Estimates & Forecast, By Cooling Technology, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Water glycol

- 7.3 Oil-based

- 7.4 Air Cooling

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Medium Commercial Vehicles (MCV)

- 8.3.3 High Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Sweden

- 9.3.7 Czech Republic

- 9.3.8 Poland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.4.6 Singapore

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.4.9 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 BorgWarner

- 10.1.2 ZF Friedrichshafen

- 10.1.3 GKN Automotive

- 10.1.4 Dana

- 10.1.5 Continental

- 10.1.6 Linamar

- 10.1.7 Aisin

- 10.1.8 Magna

- 10.1.9 Schaeffler

- 10.1.10 Nidec

- 10.1.11 Valeo

- 10.1.12 Bosch

- 10.2 Regional players

- 10.2.1 BYD

- 10.2.2 Tesla

- 10.2.3 American Axle & Manufacturing (AAM)

- 10.2.4 JATCO

- 10.2.5 Marelli

- 10.3 Emerging players

- 10.3.1 Lucid Motors

- 10.3.2 Rivian Automotive

- 10.3.3 Protean Electric