PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019246

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019246

Heavy-Duty Autonomous Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

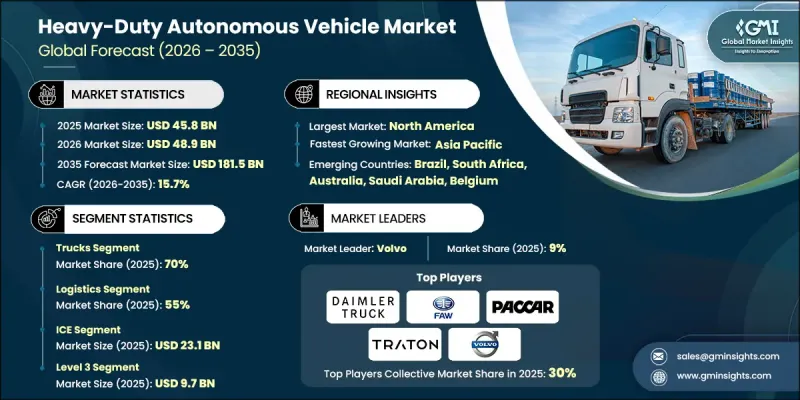

The Global Heavy-Duty Autonomous Vehicle Market was valued at USD 45.8 billion in 2025 and is estimated to grow at a CAGR of 15.7% to reach USD 181.5 billion by 2035.

The heavy-duty autonomous vehicle industry is gaining strong momentum as demand for enhanced safety systems and growing interest in self-driving technologies reshape the transportation landscape. Advanced vehicles are increasingly equipped with sophisticated sensors and intelligent software that can analyze their surroundings in real-time and make rapid driving decisions. These capabilities are expected to significantly reduce accidents, lower the number of injuries and fatalities, and minimize damage to infrastructure and vehicles, ultimately leading to reduced operational costs and improved road safety. Market expansion is further supported by continuous innovation in automation technologies and the integration of smart mobility solutions. As adoption increases, the market is evolving toward more reliable, efficient, and scalable autonomous systems that address both safety and operational challenges across heavy-duty transport applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.8 Billion |

| Forecast Value | $181.5 Billion |

| CAGR | 15.7% |

The heavy-duty autonomous vehicle market is also influenced by the need for strong industry collaboration and partnerships to support rising commercial demand. The COVID-19 pandemic created both challenges and opportunities for the industry. During the early stages of 2020, lockdown measures, supply chain disruptions, and semiconductor shortages slowed development activities and delayed the introduction of advanced autonomous and electric vehicle solutions. In addition, many pilot programs were temporarily halted as logistics providers prioritized maintaining essential operations and managing workforce constraints, rather than investing in new technology initiatives.

The trucks segment held a 70% share in 2025 and is projected to grow at a CAGR of 14.8% from 2026 to 2035. This dominance is driven by the extensive use of trucks across logistics, industrial, and resource-based sectors. Automation in trucking addresses critical challenges such as labor shortages, high operating expenses, and safety concerns. Autonomous trucks offer continuous operation, improved fuel efficiency, and faster delivery cycles, contributing to higher productivity. Advancements in sensor systems and intelligent navigation technologies are also improving driving precision and operational reliability under structured road conditions.

The ICE segment reached USD 23.1 billion in 2025. Internal combustion engine vehicles remain widely used due to their lower initial cost and well-established refueling infrastructure, which supports testing and deployment across multiple environments. Their extended driving range also makes them suitable for long-distance operations and diverse testing scenarios, supporting ongoing development in the autonomous vehicle space.

U.S. Heavy-Duty Autonomous Vehicle Market generated USD 12.7 billion in 2025. Growth is supported by increasing regulatory focus on autonomous vehicle testing and deployment, with government frameworks aimed at enabling safe and efficient adoption. Rising consumer expectations for safety and convenience, along with the need for more efficient transportation systems, are contributing to market expansion. Additionally, these vehicles are being recognized as a potential solution for reducing road congestion and improving overall traffic safety.

Key players operating in the Global Heavy-Duty Autonomous Vehicle Market include PACCAR, Volvo, Daimler Truck, TRATON, FAW, SAIC, JAC, Baidu, Waymo, and ZF Friedrichshafen. Companies in the Heavy-Duty Autonomous Vehicle Market are strengthening their market position through continuous technological advancement and strategic collaboration. They are investing in research and development to enhance autonomous driving capabilities, sensor accuracy, and system reliability. Partnerships with technology providers and logistics companies are enabling faster innovation and real-world deployment. Businesses are also focusing on scalable vehicle platforms and software integration to improve operational efficiency and reduce costs. Expanding testing programs and improving regulatory alignment are key priorities to accelerate commercialization. In addition, companies are enhancing production capabilities and optimizing supply chains to meet growing demand, while aligning product offerings with evolving industry requirements to maintain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Level of Autonomy

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Sensor & Perception Suppliers

- 3.1.1.2 Autonomous Driving Software & AI Stack

- 3.1.1.3 Connectivity & Telematics Providers

- 3.1.1.4 Retrofit & Integration Suppliers

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of 5G and high-speed connectivity

- 3.2.1.2 Growing demand for vehicle safety and telematics

- 3.2.1.3 Government mandates for vehicle connectivity

- 3.2.1.4 Rising adoption of smart mobility and digital services

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Cybersecurity and data privacy concerns

- 3.2.2.2 High cost of connectivity hardware and integration

- 3.2.3 Market opportunities

- 3.2.3.1 Over-the-air (OTA) software updates expansion

- 3.2.3.2 Integration of V2X communication technologies

- 3.2.3.3 Growth of data-driven mobility platforms

- 3.2.3.4 Integration of AI and cloud platforms in vehicles

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 MEA

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.1.1 Predictive Maintenance & Operations Optimization

- 3.13.1.2 Automated design optimization

- 3.13.1.3 Supply chain AI for demand forecasting

- 3.13.1.4 GenAI use cases & adoption roadmap by segment

- 3.13.1.4.1 Tread pattern design generation

- 3.13.1.4.2 Customer service chatbots & technical support

- 3.13.1.4.3 Marketing content creation

- 3.13.1.4.4 Risks, limitations & regulatory considerations

- 3.13.1.4.4.1 Data privacy in IoT-enabled smart products

- 3.13.1.4.4.2 AI algorithm transparency requirements

- 3.13.1.4.4.3 Liability in AI-driven product failures

- 3.13.1 AI-driven disruption of existing business models

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Trucks

- 5.2.1 Class 7

- 5.2.2 Class 8

- 5.3 Buses

Chapter 6 Market Estimates & Forecast, By Level of Autonomy, 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Level 1

- 6.3 Level 2

- 6.4 Level 3

- 6.5 Level 4

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicle

- 7.4 Hybrid vehicle

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Logistics

- 8.3 Construction & Mining

- 8.4 Transportation

- 8.5 Others

Chapter 9 Market Estimates & Forecast By End use, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Nordic

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East & Africa

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Baidu

- 11.1.2 Scania

- 11.1.3 Daimler Truck

- 11.1.4 Einride

- 11.1.5 PACCAR

- 11.1.6 TRATON

- 11.1.7 Volvo

- 11.1.8 ZF Friedrichshafen

- 11.1.9 Waymo

- 11.2 Regional players

- 11.2.1 2getthere

- 11.2.2 Navya ARMA

- 11.2.3 New Flyer

- 11.2.4 FAW

- 11.2.5 Aurora

- 11.2.6 Embark Trucks

- 11.3 Emerging players

- 11.3.1 Kodiak Robotics

- 11.3.2 Oxa Autonomy

- 11.3.3 Torc Robotics

- 11.3.4 TuSimple

- 11.3.5 Zoox