PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019252

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019252

Swine Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

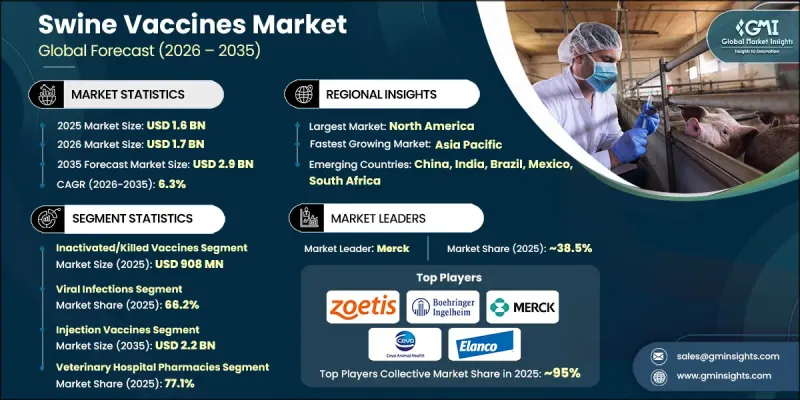

The Global Swine Vaccines Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 2.9 billion by 2035.

Market growth is driven by the increasing demand for pork and related products across global markets, which is placing greater emphasis on maintaining herd health and improving productivity. Swine vaccines play a critical role in protecting pigs by activating their immune systems to defend against a range of infectious agents, including viruses, bacteria, and other pathogens. The ongoing expansion of the livestock sector, fueled by population growth, urbanization, and evolving dietary habits, continues to accelerate demand for effective animal healthcare solutions. As production systems become more intensive to enhance output and efficiency, producers are placing stronger focus on preventive healthcare practices. Vaccination is emerging as a key strategy to reduce disease risks, improve survival rates, and protect economic returns. In addition, concerns related to food security are encouraging the adoption of advanced disease prevention measures, further supporting the growth of the swine vaccines market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 6.3% |

The inactivated or killed vaccines segment generated USD 908 million in 2025, reflecting its strong position in the market. These vaccines are widely preferred due to their established safety profile and stability. Their extended shelf life and relatively straightforward storage requirements make them suitable for large-scale immunization programs. As a result, they continue to be a reliable option for managing commonly occurring diseases in swine populations.

The viral infections segment accounted for 66.2% share in 2025 and is expected to grow at a CAGR of 6.4% during 2026-2035. This segment's growth is driven by the widespread presence and economic impact of viral diseases affecting swine populations. Such infections are highly transmissible and can significantly affect animal health, productivity, and overall farm profitability. Their rapid spread in high-density farming environments reinforces the importance of vaccination as a primary preventive approach, supporting the segment's dominant position.

North America Swine Vaccines Market captured USD 682.6 million in 2025 and is projected to reach USD 1.2 billion by 2035, growing at a CAGR of 5.8% between 2026 and 2035. The region's leadership is supported by advanced livestock management systems, well-developed veterinary healthcare infrastructure, and strong demand for high-quality pork production. The United States remains a major contributor due to its large-scale swine production capacity and significant role in both domestic consumption and exports. Continued focus on disease prevention and the presence of leading animal health companies further reinforce the region's strong market position.

Key players operating in the Global Swine Vaccines Market include Zoetis, Merck, Boehringer Ingelheim, Elanco Animal Health Incorporated, Ceva Sante Animale, HIPRA S.A., Biogenesis Bago, Vaxxinova (EW Group), Indian Immunologicals, Bioveta, Vibac, Colorado Serum Company, and Addison Biological Laboratory. Companies in the swine vaccines market are strengthening their market position through continuous research and development, strategic partnerships, and expansion into emerging regions. They are focusing on developing advanced vaccines with improved efficacy, broader protection, and enhanced safety profiles. Collaborations with veterinary service providers and livestock producers are helping companies expand their reach and improve product adoption. In addition, manufacturers are investing in production capacity expansion and supply chain optimization to ensure consistent availability. Companies are also emphasizing regulatory compliance and quality standards while exploring innovative vaccine technologies to address evolving disease challenges and maintain a competitive edge in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of zoonotic diseases

- 3.2.1.2 Expanding livestock industry and food security concerns

- 3.2.1.3 Advancements in vaccine technology

- 3.2.1.4 Increasing outbreaks of animal diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High R&D costs & long development timelines

- 3.2.2.2 Cold chain infrastructure limitations

- 3.2.2.3 Regulatory complexity & approval delays

- 3.2.3 Market opportunities

- 3.2.3.1 mRNA & next-generation platform adoption

- 3.2.3.2 Thermostable vaccine development

- 3.2.3.3 Combination vaccine innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Vaccine technology evolution and innovation

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Clinical trial/pipeline analysis (Driven by Primary Research)

- 3.9 Future market trends

- 3.10 Impact of AI & generative AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Live attenuated vaccines

- 5.3 Inactivated/killed vaccines

- 5.4 Viral vector vaccines

- 5.5 mRNA vaccines

- 5.6 Other vaccines

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Bacterial infections

- 6.3 Viral infections

- 6.4 Parasitic infections

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 203($ Mn)

- 7.1 Key trends

- 7.2 Injection vaccines

- 7.3 Oral vaccines

- 7.4 Immersion/spray vaccines

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 UAE

Chapter 10 Company Profiles

- 10.1 Addison Biological Laboratory

- 10.2 Bioveta

- 10.3 Boehringer Ingelheim

- 10.4 Ceva Sante Animale

- 10.5 Colorado Serum Company

- 10.6 Elanco Animal Health Incorporated

- 10.7 HIPRA S.A.

- 10.8 Indian Immunologicals

- 10.9 Merck

- 10.10 Biogenesis Bago

- 10.11 Vaxxinova (EW Group)

- 10.12 Vibac

- 10.13 Zoetis