PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027443

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027443

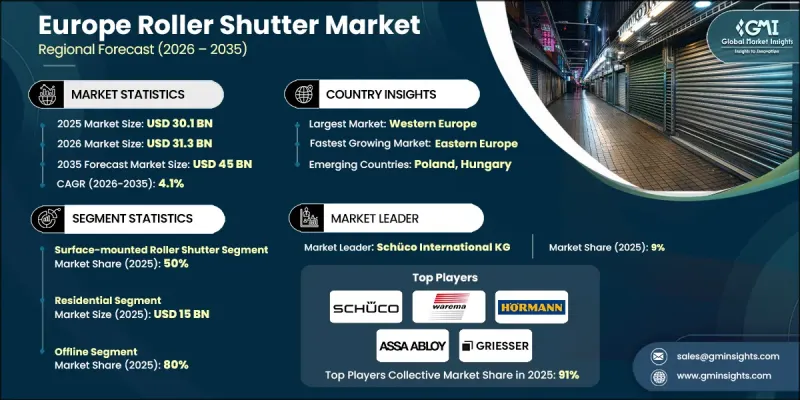

Europe Roller Shutter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Europe Roller Shutter Market was valued at USD 30.1 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 45 billion by 2035.

The growth reflects increasing demand for solutions that combine functionality, security, and modern design appeal. Buyers are placing greater emphasis on products that not only enhance safety but also complement contemporary architectural styles. As a result, manufacturers are focusing on improving product aesthetics, minimizing operational noise, and simplifying everyday usability. Growing awareness of the benefits associated with roller shutters, including improved privacy, protection against environmental conditions, and enhanced indoor comfort, is supporting widespread adoption across both residential and commercial sectors. Additionally, the market is benefiting from a shift toward integrated building solutions, where roller shutters are considered an essential component of overall design rather than a secondary addition, reinforcing their importance in new construction and renovation projects.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $30.1 Billion |

| Forecast Value | $45 Billion |

| CAGR | 4.1% |

Technological advancements are playing a key role in shaping the Europe roller shutter market, with increasing focus on user convenience and operational efficiency. Modern systems are being designed to offer seamless functionality through automated controls and smart integration, enabling users to manage operations with ease. Manufacturers are prioritizing intuitive designs that enhance the overall user experience while maintaining reliability. At the same time, architects and developers are incorporating roller shutter systems more strategically into building designs, recognizing their value in improving both performance and visual appeal across a wide range of applications.

The surface-mounted roller shutter segment accounted for 50% share in 2025, maintaining its position as the leading product category. Its strong market presence is supported by advantages such as straightforward installation, compatibility with existing structures, cost efficiency, and flexible design integration. These systems are widely adopted due to their ability to streamline installation processes, reduce labor requirements, and minimize disruption during upgrades. Their practical benefits and adaptability continue to make them a preferred option across various applications, contributing significantly to overall market growth.

The residential segment held a 57% share in 2025, generating USD 15 billion. Growth in this segment is driven by homeowner preferences that prioritize safety, energy efficiency, aesthetic value, and long-term cost benefits. Purchasing decisions in this category are typically influenced by a combination of functional and lifestyle considerations, with consumers viewing high-quality installations as long-term investments. Extended ownership periods allow costs to be distributed over time, making premium solutions more accessible while delivering ongoing advantages such as enhanced comfort, improved security, and reduced energy consumption.

Western Europe Roller Shutter Market held a 56% share, generating USD 16.9 billion in 2025. The region's leadership is supported by a mature construction landscape, strong economic conditions, and a well-established culture of property investment and security awareness. An aging building stock is driving consistent demand for replacement solutions, while evolving regulatory requirements are encouraging the adoption of modern, compliant systems. These structural factors are contributing to stable and predictable demand patterns, supporting sustained market growth across the region.

Key companies operating in the Europe Roller Shutter Market include ASSA ABLOY, Hormann Group, Schuco International KG, Aluprof SA, Bubendorff, Griesser AG, Roma KG, WAREMA Renkhoff SE, Internorm International GmbH, Alulux GmbH, heroal, Alumil, Novoferm GmbH, Teckentrup, and Schenker Storen AG. Companies in the Europe Roller Shutter Market are strengthening their competitive position through innovation, strategic expansion, and customer-focused solutions. Significant investments in product development are enabling the introduction of advanced systems with improved automation, energy efficiency, and design flexibility. Businesses are increasingly adopting smart technologies to enhance user convenience and differentiate their offerings. Strategic partnerships and collaborations are helping companies broaden their market reach and improve distribution capabilities. In addition, firms are focusing on customization options to meet diverse consumer preferences while maintaining high-quality standards. Expansion into new geographic markets and reinforcement of service networks are further supporting growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Slat material

- 2.2.4 Operation system

- 2.2.5 Installation

- 2.2.6 Fixation type

- 2.2.7 End use

- 2.2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 EU energy performance of buildings directive (epbd) compliance mandates

- 3.2.1.2 Energy cost escalation and climate adaptation imperatives

- 3.2.1.3 Smart home ecosystem expansion and iot integration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Construction market cyclicality and western european residential decline

- 3.2.2.2 Raw material price volatility and european aluminum production structural decline

- 3.2.3 Opportunities

- 3.2.3.1 Eastern European market expansion and manufacturing footprint development

- 3.2.3.2 Service-based business model transformation and recurring revenue development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Trade data analysis

- 3.5.1 Import/export volume & value trends

- 3.5.2 Key trade corridors & tariff impact

- 3.6 Impact of ai & generative ai on the market

- 3.6.1 AI-driven disruption of existing business models

- 3.6.2 Gen AI use cases & adoption roadmap by segment

- 3.6.3 Risks, limitations & regulatory considerations

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By product type

- 3.8.2 By region

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirements

- 3.9.2 Regional regulatory frameworks

- 3.9.3 Certification standards

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035(USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Surface-mounted roller shutter

- 5.3 Built-in / integrated roller shutter

- 5.4 Retrofit roller shutter

Chapter 6 Market Estimates and Forecast, By Slat Material, 2022 - 2035(USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Aluminum

- 6.3 Steel & other metals

- 6.4 Wood

- 6.5 PVC / plastic

- 6.6 Composite materials

Chapter 7 Market Estimates and Forecast, By Operation System, 2022 - 2035(USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Motorized

- 7.4 Smart / IoT

Chapter 8 Market Estimates and Forecast, By Installation, 2022 - 2035(USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 New Installation

- 8.3 Replacements

Chapter 9 Market Estimates and Forecast, By Fixation Type, 2022 - 2035(USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Door

- 9.3 Window

Chapter 10 Market Estimates and Forecast, By End Use Industry, 2022 - 2035(USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Commercial

- 10.2.1 HoReCa (hotels, restaurants, cafes)

- 10.2.2 Hospitals

- 10.2.3 Offices

- 10.2.4 Malls

- 10.2.5 Others

- 10.3 Residential

- 10.4 Industrial

- 10.4.1 Warehouses

- 10.4.2 Factories

Chapter 11 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035(USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce

- 11.2.2 Company websites

- 11.3 Offline

- 11.3.1 Distributors

- 11.3.2 Retailers

- 11.3.3 Specialty stores

- 11.3.4 Others

Chapter 12 Market Estimates and Forecast, By Country, 2022 - 2035(USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Northern Europe

- 12.2.1 Sweden

- 12.2.2 Denmark

- 12.2.3 Finland

- 12.2.4 Rest of Northern Europe

- 12.3 Eastern Europe

- 12.3.1 Poland

- 12.3.2 Czech Republic

- 12.3.3 Hungary

- 12.3.4 Rest of Eastern Europe

- 12.4 Southern Europe

- 12.4.1 Italy

- 12.4.2 Spain

- 12.4.3 Greece

- 12.4.4 Rest of Southern Europe

- 12.5 Western Europe

- 12.5.1 France

- 12.5.2 Germany

- 12.5.3 UK

- 12.5.4 Netherlands

- 12.5.5 Rest of Western Europe

Chapter 13 Company Profiles

- 13.1 Alulux GmbH

- 13.2 Alumil

- 13.3 Aluprof SA

- 13.4 ASSA ABLOY

- 13.5 Bubendorff

- 13.6 Griesser AG

- 13.7 heroal

- 13.8 Hormann Group

- 13.9 Internorm International GmbH

- 13.10 Novoferm GmbH

- 13.11 Roma KG

- 13.12 Schenker Storen AG

- 13.13 Schuco International KG

- 13.14 Teckentrup

- 13.15 WAREMA Renkhoff SE