PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027459

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027459

Polydimethylsiloxane (PDMS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

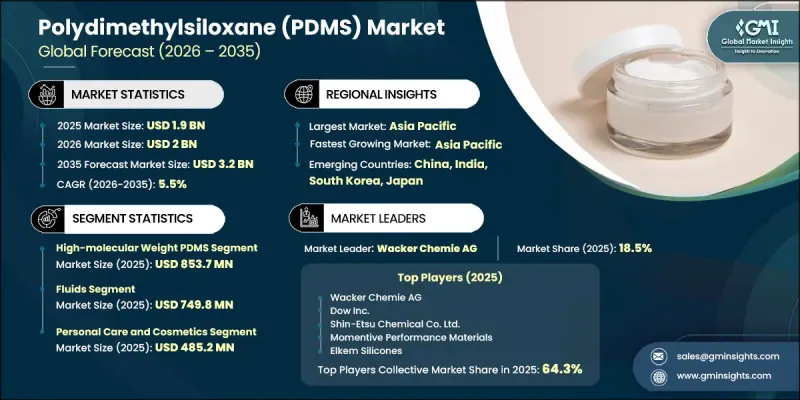

The Global Polydimethylsiloxane (PDMS) Market was valued at USD 1.9 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 3.2 billion by 2035.

The industry is gaining steady traction as PDMS continues to establish itself as a vital material across diverse end-use sectors. This silicon-based organic polymer is defined by a siloxane backbone structure formed by alternating silicon and oxygen atoms bonded with methyl groups, enabling a wide spectrum of performance attributes. Its combination of thermal resilience, chemical stability, low surface energy, permeability, optical clarity, and compatibility with biological systems enhances its industrial relevance. Production methods rely on advanced polymerization processes that precisely regulate molecular weight and chain structure, allowing manufacturers to tailor viscosity and mechanical behavior. Techniques such as controlled hydrolysis, condensation, and polymer chain development are used to generate materials ranging from fluid forms to solid elastomers. PDMS remains a fundamental component within the specialty chemicals landscape, supported by strong manufacturing ecosystems and increasing adoption across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 5.5% |

The high molecular weight PDMS segment accounted for USD 853.7 million in 2025. Materials within the viscosity range of 1,000 to 1,000,000 cSt continue to dominate due to their extensive role in producing elastomers, sealants, adhesives, and coating systems. Their ability to deliver durability and structural integrity supports widespread use in performance-driven industrial applications, where higher-value formulations are required to meet stringent operational standards.

The personal care and cosmetics segment reached USD 485.2 million in 2025, emerging as the fastest-growing application area. PDMS plays a critical role in enhancing formulation quality across beauty and care products by improving texture, stability, and performance. Increasing demand for high-quality formulations with enhanced sensory appeal and long-lasting characteristics continues to drive innovation, enabling manufacturers to differentiate products in a highly competitive global market.

North America Polydimethylsiloxane (PDMS) Market is projected to grow from USD 505.4 million in 2025 to USD 857.3 million by 2035, reflecting strong regional expansion. Growth is supported by advanced industrial capabilities, well-established manufacturing infrastructure, and sustained demand across key sectors. The United States leads regional consumption, driven by high-value production environments and technological advancement, while Canada contributes through its industrial base and integrated supply chain capabilities that support regional market development.

Key companies operating in the Global Polydimethylsiloxane (PDMS) Market include Dow Inc., Wacker Chemie AG, Shin Etsu Chemical Co., Ltd., Momentive Performance Materials, Elkem Silicones, KCC Corporation, Merck KGaA, Thermo Fisher Scientific, Evonik Industries, Dongguan City Betterly New Materials Co., Ltd., Gelest Inc., Clearco Products Co., Inc., NuSil Technology LLC, ACC Silicones Ltd., and Zhejiang Runhe Chemical New Material Co., Ltd. Companies in the Global Polydimethylsiloxane (PDMS) Market are strengthening their competitive position through continuous innovation and strategic expansion initiatives. Significant investments are being directed toward research and development to enhance product performance, improve formulation flexibility, and expand application scope. Strategic collaborations and partnerships enable access to advanced technologies and new customer segments. Manufacturers are also focusing on capacity expansion and regional footprint growth to meet rising global demand efficiently. Customization of products to meet specific industry requirements is becoming a key differentiator. Additionally, companies are optimizing supply chains, enhancing distribution networks, and leveraging pricing strategies to improve market penetration while aligning with evolving regulatory and sustainability expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Form

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Low-Molecular Weight PDMS

- 5.3 High-Molecular Weight PDMS

- 5.4 Ultra-High Molecular Weight PDMS

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Fluids

- 6.3 Elastomers & Gels

- 6.4 Resins & Coatings

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Medical and Healthcare

- 7.3 Personal Care and Cosmetics

- 7.4 Electronics

- 7.5 Automotive

- 7.6 Construction

- 7.7 Industrial Processes

- 7.8 Household Care

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Wacker Chemie AG

- 9.2 Dow Inc.

- 9.3 Shin-Etsu Chemical Co., Ltd.

- 9.4 Momentive Performance Materials

- 9.5 Elkem Silicones

- 9.6 KCC Corporation

- 9.7 Merck KGaA

- 9.8 Thermo Fisher Scientific

- 9.9 Evonik Industries

- 9.10 Dongguan City Betterly New Materials Co., Ltd.

- 9.11 Gelest Inc.

- 9.12 Clearco Products Co., Inc.

- 9.13 NuSil Technology LLC

- 9.14 ACC Silicones Ltd.

- 9.15 Zhejiang Runhe Chemical New Material Co., Ltd.