PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027468

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027468

North America STEM Toys Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

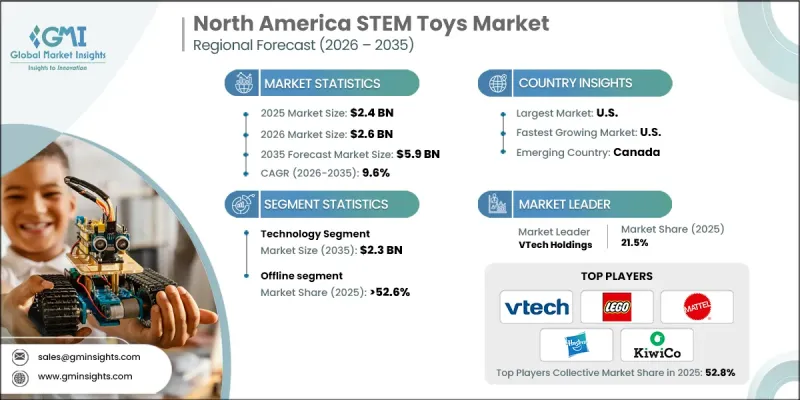

North America STEM Toys Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 5.9 billion by 2035.

The growth reflects a broader cultural transition in which educational toys are increasingly viewed as essential tools for long-term skill development and career readiness. Parents across the region are prioritizing products that support cognitive growth and practical learning from an early age, aligning playtime with future academic and professional outcomes. Institutional backing is also reinforcing this trend, with educational frameworks emphasizing the importance of STEM-based learning at early stages. This support is influencing consumer behavior, as classroom-driven learning tools are increasingly adopted in home environments. Additionally, strong purchasing power and a heightened focus on addressing future workforce skill requirements are contributing to sustained demand. As a result, the market continues to evolve as a stable and high-growth segment within the broader toy industry, supported by a clear emphasis on measurable educational value.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 9.6% |

Institutional support is creating a ripple effect across the North America STEM toys market, as educational tools originally designed for structured learning environments gain traction among households. Consumer purchasing behavior is also being shaped by a growing preference for products that deliver long-term developmental benefits. Many buyers are placing importance on toys that provide sustained engagement and contribute to intellectual growth over time. This shift, combined with stable disposable income levels, is creating consistent demand for high-quality educational products that align with evolving learning expectations and skill development priorities.

The offline distribution channel accounted for 52.6% share in 2025, maintaining its leading position despite the rise of digital retail platforms. Physical stores continue to play a crucial role due to the interactive nature of educational toy purchases, where consumers prefer to evaluate product quality and features in person. Immediate product availability and reduced concerns related to handling sensitive components also contribute to the strength of this channel. Retailers are enhancing in-store experiences to support informed purchasing decisions, reinforcing the importance of brick-and-mortar outlets in the market.

The technology segment generated USD 894.9 million in 2025 and is expected to reach USD 2.3 billion by 2035. Growth in this segment is being driven by increasing demand for interactive and immersive learning experiences that combine physical and digital elements. These products are designed to engage users over extended periods by offering progressive levels of complexity, allowing them to develop new skills over time. Integration with connected devices is further enhancing user engagement, making these products a consistent part of daily routines. The ability to deliver both introductory and advanced learning experiences is strengthening the value proposition of technology-driven STEM toys.

United States STEM Toys Market held an 84.6% share in 2025. Market leadership is supported by strong consumer emphasis on early education and skill development, with STEM toys widely recognized as valuable learning tools. Educational institutions and supplementary learning programs continue to incorporate hands-on approaches, reinforcing steady demand. High consumer spending capacity and a well-developed retail ecosystem are further supporting market expansion. Increased awareness of future career pathways related to STEM fields is encouraging early adoption of educational products. Additionally, ongoing support from both public and private initiatives is strengthening acceptance of learning-oriented toys, while the presence of major industry players contributes to continuous innovation and broad market reach.

Key companies operating in the North America STEM Toys Market include The LEGO Group, Hasbro, Mattel, VTech Holdings, LeapFrog, Spin Master, Ravensburger/ThinkFun, KiwiCo, Sphero, Educational Insights, Learning Resources, Melissa & Doug, MAGNA-TILES, Fat Brain Toys, and K'NEX (Basic Fun!). Companies in the North America STEM Toys Market are strengthening their market position through innovation, strategic partnerships, and targeted expansion initiatives. Significant investments in research and development are enabling the creation of interactive, technology-driven products that enhance learning outcomes and user engagement. Firms are also collaborating with educational institutions and content developers to align products with evolving curriculum standards. Expanding omnichannel distribution strategies is helping companies reach a wider audience while maintaining strong retail partnerships. In addition, businesses are focusing on product differentiation through advanced features and long-term usability. Emphasis on brand building, digital marketing, and customer engagement is further supporting growth, while continuous portfolio expansion ensures relevance in a competitive and rapidly evolving market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.3.1 Source consistency protocol

- 1.4 Research Trail & Confidence Scoring

- 1.4.1 Research Trail Components

- 1.4.2 Scoring Components

- 1.5 Data Collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.7 Paid sources

- 1.7.1 Sources, by region

- 1.8 Base estimates and calculations

- 1.8.1 Base year calculation for any one approach

- 1.9 Forecast model

- 1.9.1 Quantified market impact analysis

- 1.9.1.1 Mathematical impact of growth parameters on forecast

- 1.9.1 Quantified market impact analysis

- 1.10 Research transparency addendum

- 1.10.1 Source attribution framework

- 1.10.2 Quality assurance metrics

- 1.10.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Price

- 2.2.5 Age group

- 2.2.6 End user

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing parental emphasis on early education

- 3.2.1.2 Integration of advanced technology (AI/ML/AR)

- 3.2.1.3 Government initiatives and curriculum alignment

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of advanced robotics and coding kits

- 3.2.2.2 Competition from screen-based digital entertainment

- 3.2.3 Opportunities

- 3.2.3.1 Untapped markets in emerging economies

- 3.2.3.2 Convergence of physical and digital play (STEAM)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.7 Trade data analysis

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 Gen AI use cases & adoption roadmap by segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Country price variations

- 3.9.4 Impact of raw material costs on pricing

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Raw material analysis

- 3.13 Consumer behaviour analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behaviour

- 3.13.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Science

- 5.3 Technology

- 5.4 Engineering

- 5.5 Mathematics

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Wood

- 6.4 Metal

- 6.5 Others (Eco-friendly, recycled materials)

Chapter 7 Market Estimates and Forecast, By Age Group, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 0-3 years

- 7.3 3-8 years

- 7.4 8-12 years

- 7.5 12+ years

Chapter 8 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Individual Consumers

- 9.3 Schools & Educational Institutions

- 9.4 Activity Centres

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-Commerce

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Supermarkets/Hypermarkets

- 10.3.2 Specialty Stores

- 10.3.3 Others (Individual stores, Departmental stores, etc.)

Chapter 11 Market Estimates & Forecast, By Country, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 U.S.

- 11.3 Canada

Chapter 12 Company Profiles

- 12.1 Educational Insights

- 12.2 Fat Brain Toys

- 12.3 Hasbro

- 12.4 K'NEX (Basic Fun!)

- 12.5 KiwiCo

- 12.6 LeapFrog

- 12.7 Learning Resources

- 12.8 MAGNA-TILES

- 12.9 Mattel

- 12.10 Melissa & Doug

- 12.11 Ravensburger/ThinkFun

- 12.12 Sphero

- 12.13 Spin Master

- 12.14 The LEGO Group

- 12.15 VTech Holdings