PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027479

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027479

Canned Vegetable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

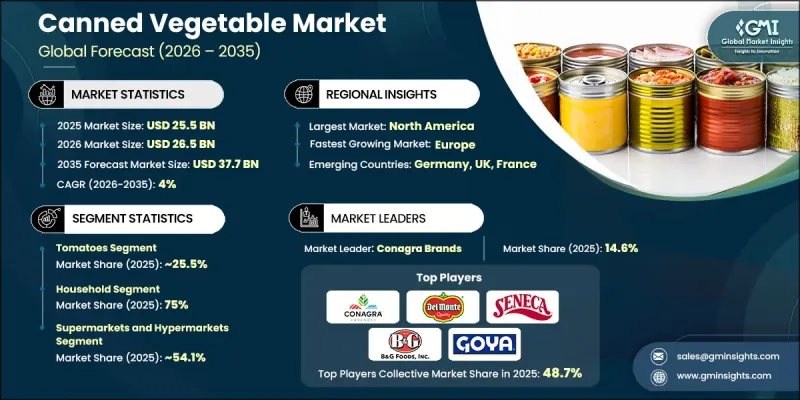

The Global Canned Vegetable Market was valued at USD 25.5 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 37.7 billion by 2035.

The canned vegetables industry continues to expand steadily as consumers increasingly prioritize convenience, longer shelf life, and nutritional value in their food choices. Demand is being shaped by shifting lifestyles that favor easy-to-prepare meal solutions without compromising quality. At the same time, advancements in processing technologies are enabling manufacturers to enhance product consistency, safety, and overall quality standards. The adoption of automated systems is improving operational efficiency while supporting better hygiene and controlled production environments. Regulatory frameworks remain a key influence, guiding manufacturers to maintain strict compliance with food safety and labeling requirements. These standards are encouraging transparency and product reliability, strengthening consumer trust. Market growth is further supported by rising interest in healthier product options, prompting companies to explore organic and clean-label offerings. Additionally, sustainability trends are influencing packaging innovations, with increased focus on environmentally responsible materials. Continuous product development and evolving consumer preferences are expected to sustain long-term growth across the global canned vegetable market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $25.5 Billion |

| Forecast Value | $37.7 Billion |

| CAGR | 4% |

In 2025, the household segment accounted for 75% share and is expected to grow at a CAGR of 4.4% during 2026-2035. This segment leads the market as consumers increasingly seek convenient food options that combine long shelf life with nutritional benefits. Changing lifestyles and time constraints are encouraging households to incorporate canned vegetables into daily meal preparation. At the same time, the foodservice segment is expanding steadily as demand rises for efficient, consistent ingredient solutions that enable quick preparation and cost-effective operations.

The supermarkets and hypermarkets segment held a 54.1% share in 2025 and is projected to grow at a CAGR of 4.3% through 2035. These retail channels continue to dominate the canned vegetable market due to their extensive product availability and strong consumer reach. Their ability to offer a wide selection in a single location supports consistent purchasing behavior. Convenience stores are also gaining traction, particularly in urban areas where accessibility and quick purchasing options are valued. In addition, online retail is emerging as a rapidly growing channel, driven by increasing internet penetration and changing consumer shopping preferences, supported by the ease of home delivery services.

North America Canned Vegetable Market accounted for 37.6% share in 2025, maintaining a strong regional position. Growth in this region is supported by consistent demand for convenient and shelf-stable food products. Increasing awareness of healthier eating habits is encouraging the adoption of improved product varieties. The United States continues to lead the regional market due to strong demand for quick meal solutions aligned with fast-paced lifestyles. Sustainability trends and growing awareness of environmentally responsible packaging are also influencing production practices across the region. Furthermore, the expansion of e-commerce platforms is enhancing product accessibility and supporting sales growth.

Key players operating in the Canned Vegetable Market include Del Monte Foods, Conagra Brands, B&G Foods, Goya Foods, Amy's Kitchen, Seneca Foods Corporation, Faribault Foods, Roland Foods, Mutti S.p.A., Ayam Brand, Farmer's Market Foods, and McCall Farms. Companies in the canned vegetable market are focusing on innovation, operational efficiency, and strategic expansion to strengthen their market position. They are investing in advanced processing technologies to improve product quality and shelf stability while maintaining safety standards. Businesses are also expanding their product portfolios to meet evolving consumer preferences for healthier and sustainable options. Strategic partnerships and distribution network enhancements are helping companies improve market reach and accessibility. In addition, firms are increasing investments in eco-friendly packaging solutions and digital sales channels to align with sustainability goals and changing purchasing behavior, while reinforcing brand visibility and customer engagement.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 End user

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Peas

- 5.3 Corn

- 5.4 Carrots

- 5.5 Beans

- 5.6 Tomatoes

- 5.7 Mushrooms

- 5.8 Mixed vegetables

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Household

- 6.3 Foodservice

- 6.4 Industrial

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Supermarkets and hypermarkets

- 7.3 Convenience stores

- 7.4 Online retailers

- 7.5 Specialty stores

- 7.6 Direct sales

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Amy's Kitchen

- 9.2 Ayam Brand

- 9.3 B&G Foods

- 9.4 Conagra Brands

- 9.5 Del Monte Foods

- 9.6 Faribault Foods

- 9.7 Farmer's Market Foods

- 9.8 Goya Foods

- 9.9 McCall Farms

- 9.10 Mutti S.p.A.

- 9.11 Roland Foods

- 9.12 Seneca Foods Corporation